With the economy several months deep into the 2020 recession, this summer was surprisingly competitive for homebuyers. While job losses and social distancing measures kept some buyers at home, historically low mortgage interest rates increased buyer purchasing power. On top of reduced inventory, high competition was inevitable.

For example, 46% of homes for sale nationwide were listed for less than two weeks before going under contract during July 2020, according to Redfin. This is the largest share of homes to bounce off the market in less than two weeks since Redfin began tracking this data in 2012.

Further, during the month of July, 54% of Redfin offers faced competition nationwide. Here in California, the share of Redfin offers facing bidding wars was:

- 67% in the San Francisco and San Jose area;

- 65% in San Diego;

- 58% in Los Angeles; and

- 47% in Sacramento.

While Redfin offers represent just a slice of the market, these numbers shed some light on how much competition is heating up in California’s housing market.

It’s hot now, but winter is coming

Reading this data may tempt some real estate professionals to believe the worst is behind us and the housing market will be spared from the recession. However, California’s housing market is still in a period of transition in 2020.

Currently, homebuyer demand is high relative to the number of properties available. But inventory is extremely low — in fact, nationwide multiple listing service (MLS) inventory has never been this low in the 20+ years it has been tracked, according to Redfin. When inventory starts to rise again, will demand rise with it?

The answer is tied directly to jobs. Homebuyers need access to savings and high credit scores, but most importantly, quality and reliable sources of income.

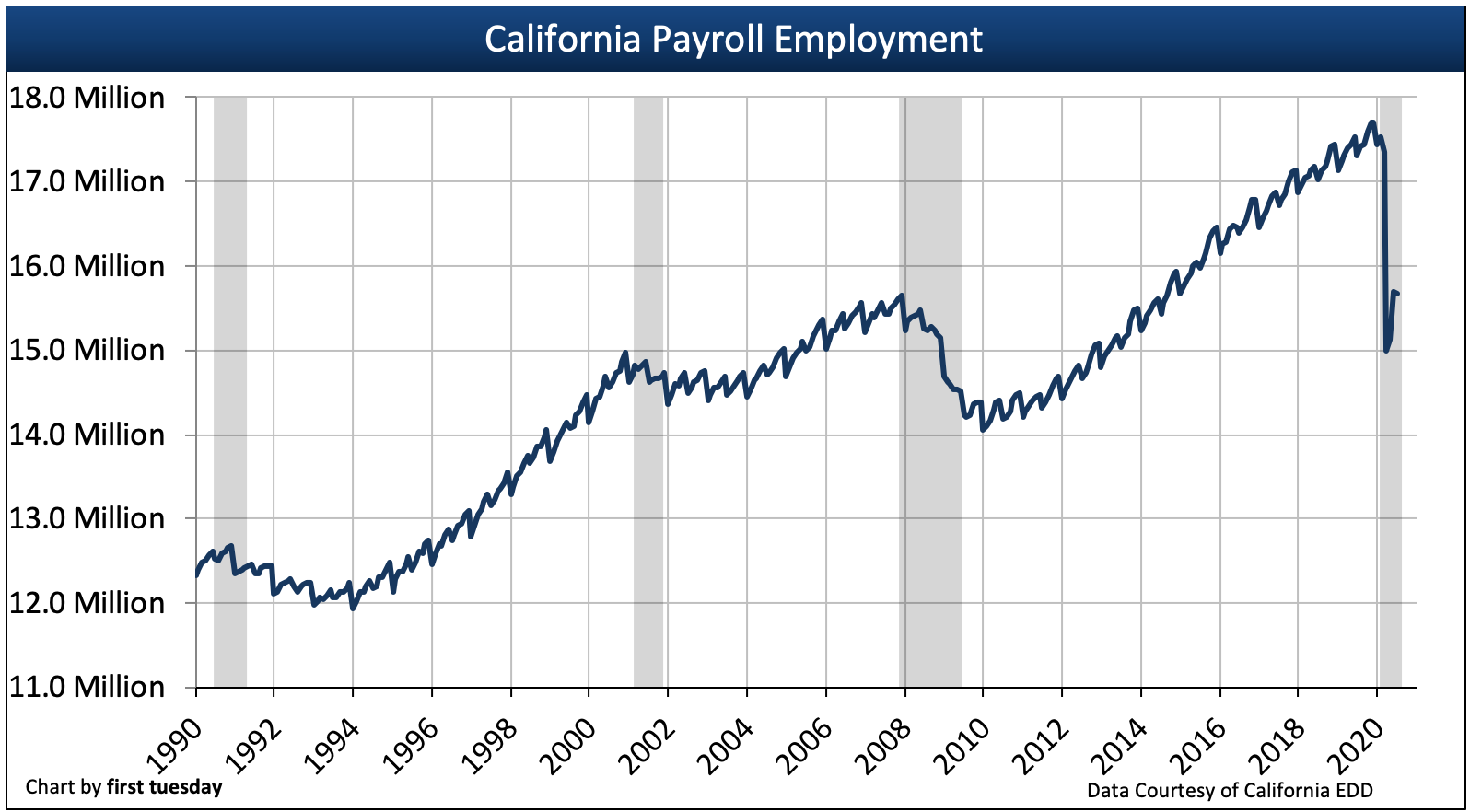

California lost over 2.7 million jobs from the December 2019 peak until bottoming in April 2020. Since then, while the media has happily touted “record job gains,” these have equaled a return of just 680,600 of these lost jobs as of July 2020.

Until jobs are recovered, a stable housing market is simply not possible.

When will a jobs recovery occur in California?

It’s tempting to point to a COVID-19 vaccine and an end to the pandemic as the magical turning point for the jobs market. But that would be to ignore the underlying recession that was developing in the economy long before the pandemic was on anyone’s radar. Yes, the social distancing required by the pandemic response caused a more sudden and severe recession than anticipated. But the conditions for a troubled economy remain.

This recession is likely to mimic a “W”-shape in the remainder of 2020 and 2021, with conditions rising with false momentum, only to fall back in the following quarter in what economists have morbidly termed a dead cat bounce. The employment market won’t begin to make solid climbs until 2022 or even 2023, at which point the housing market will begin to emerge from its own recession.

In the meantime, as the summer of 2020 comes to a close, real estate professionals who wish to continue making a living in the lean months to come need to get creative and plan ahead as soon as possible.

These strategies include becoming familiar with foreclosure and short sale transactions, as well as researching popular investment strategies. Periods of consistently falling home sales volume are axiomatically followed by falling prices, which tend to bring on distressed sales. Preparing for more foreclosures now will put real estate brokers a step ahead of the competition; important, when there are so few sales to go around.

Related article:

{kind=link}