Why are homebuyers buying in 2023?

- To relocate due to a job or income change (47%, 7 Votes)

- To improve their quality of living (33%, 5 Votes)

- For investment purposes (20%, 3 Votes)

Total Voters: 15

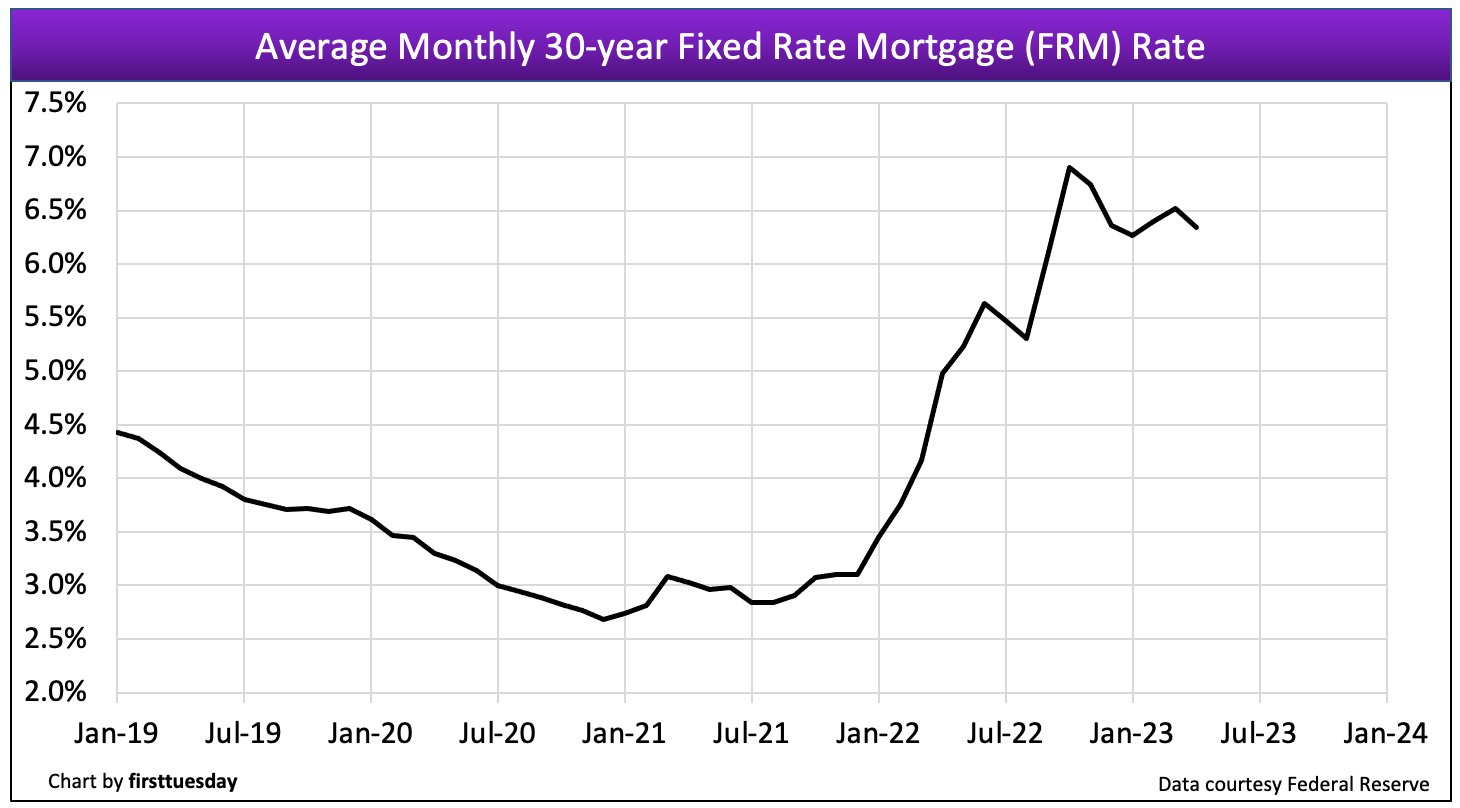

Mortgage interest rates have skyrocketed since early 2022, leaving reminiscent homebuyers — and seller illusional pricing — unwilling to participate. The result has been plunging home sales volume, softening home prices, and a dilapidated for-sale inventory.

71% of surveyed homebuyers say they will not move on a purchase until they are able to borrow at a mortgage rate below 5.5%, according to John Burns Research and Consulting.

But waiting for a 5.5% FRM is mental joy riding. As of May 2023, the monthly average 30-year fixed rate mortgage (FRM) rate is just over 6.3% — rising to 6.7% in mid-June — down slightly from the peak of nearly 7% reached in October 2022. According to this survey, this rate is simply perceived as too high a bar to induce most homebuyers to jump in.

Video updated July 2023

It’s unclear where the 5.5% figure is coming from, since it has zero correlation with actual home sales. The last time FRM rates were below this 5.5% “magic number” was in August 2022, when homebuyer purchases were surely booming? (They were not).

Still, since rates were still at historic lows just two years ago — sub 3% — to understand how today’s homebuyers feel that rates are too high is complicated by issues of money illusion. Seller’s want yesterday’s prices in today’s interest rate market (delusional). Buyers want low rates in today’s falling price market (delusional). That train left the station long ago.

All the while, maximum mortgage funding is fully available to anyone with a job, which is more people today than at any time in the past 15 years. Mortgage lenders are more flexible, but buyers may not have noticed.

When the pandemic set in, the average 30-year FRM rate had risen to almost 4.0% which over seven years had gradually slowed price increases by reducing the amounts all buyers with a job were able to borrow. Today’s post-pandemic rise in the FRM to 6.7% inflicts a further reduction in buyer purchasing power — which axiomatically controls property pricing, for which sellers, or their agents refuse to do the math.

What buyers don’t comprehend is the 2020-2021 period of the Pandemic Economy saw FRM rates artificially reduced to their lowest rates ever, solely to stimulate the devastated economy — but FRMs will not see a return to those lows in the 2023 recession, or at any point in time for this homebuying generation.

Since rates won’t return to the low levels seen during the pandemic anytime soon, buyers who are employed and need purchase-assist mortgage funding to buy a home are today limited in their options to either:

- consider a home in a lower price tier (unlikely); or

- simply wait out the inevitable drop in seller asking prices, expected to reach bottom after a period of 24-to-30 months forward in 2025 into 2026

Related article:

Press Release: Q1 2023 Buyer Purchasing Power Index down 23% from a year earlier

To sell or not to sell — an owner’s pricing question

When it comes to whether or not a home sells, the ball is truly in the seller’s court. Seller alone stage their property for sale through pricing. Today’s higher interest rates and lower buyer purchasing power, both of which the bond market controls, means the only player in a real estate transaction with any wiggle room to move property is the seller.

Thus, the seller who wishes to counteract the unavoidable damage from higher interest rates needs to blow off their pricing expectations and drop their prices to meet buyers where they are.

All willing buyers when employed do quality to borrow. More relevantly, they are no differently qualified than in any other past year. However, unlike in past years, sellers are not willing to accept that mortgage funding controls the amount most buyers pay for a home.

In some cases, sellers are offering concessions to attract buyers, including:

- permanently buying down the mortgage rate by purchasing mortgage points;

- temporarily buying down the mortgage rate;

- paying for inspections and origination fees;

- paying property taxes; and

- covering the costs of repairs and improvements.

These types of mortgage buydowns are especially common for builders hoping to attract homebuyers to purchase new homes. Falling building material costs in 2023 have given builders more room to negotiate by buying down rates to attain the “magic 5.5%” and offering buyers other concessions, according to the John Burns survey.

But in the end, it is more efficient for the seller to simply list at a more attractive price immediately, avoiding the sour taste of a lingering listing. “Market worn” listings tell buyers something about the seller’s lack of motivation to sell; maybe the property also.

Sellers with a large equity, or free and clear of mortgage debt, can also avoid additional concessions and attract homebuyers by offering seller financing, also known as owner will carry or carryback financing.

This owner-will-carry (OWC) financing generally offers the buyer:

- a moderate down payment;

- a competitive interest rate;

- less stringent terms for qualification and documentation than imposed by traditional lenders; and

- no origination costs or lender processing hassle.

For the seller, carryback financing makes their property more marketable, enabling a higher sales price. It also allows them to defer any tax bite on their non-exempt profits. And then too, how about offering that “magic 5.5%” that buyers seem to have become enthralled with.

Real estate agents and brokers who are poised to counsel buyers and sellers about carryback transactions will find themselves closing more deals and earning more income in these years of rising interest rates. Read more in RPI e-book: Creating Carryback Financing

Related article:

Offering mortgage points? There are better ways to catch a buyer

{kind=link}