Why this matters: Real estate professionals are observing a trend in the steadily recovering inventory of for-sale property, a new experience for those not part of the market in the Great Recession period of 2008. The cyclical inventory event requires understanding the consequence of a consistently growing for-sale catalog — a forced reduction in pricing of property when a transaction is intended.

A buyer’s market arrives, and agents pivot

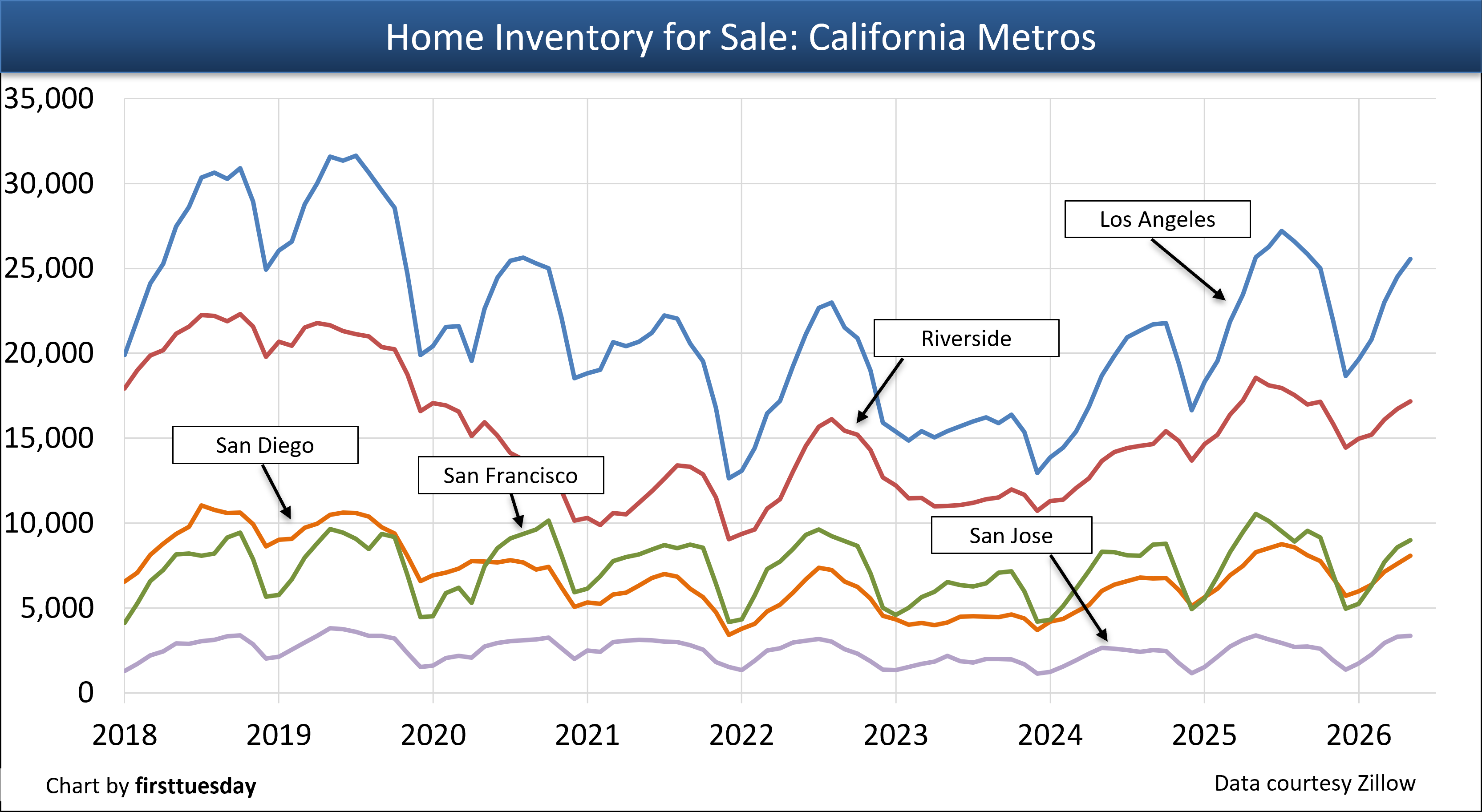

California’s inventory of homes available for sale is expanding following its unparalleled contraction:

- precipitated by the pandemic fueled buying spree of 2021; and

- aggravated by the flow-through of uncertain economic conditions including:

- high and rising mortgage rates;

- employment stagnating;

- abnormally increasing consumer costs; and

- tariff and military disruptions.

For-sale inventory in California’s largest metros averages 4.7% below a year earlier for May 2026, from data released by Zillow. Although the overall pattern shows a recovery from 2022-2023’s post-pandemic inventory low, it has not kept up with strides made last spring.

The number of properties publicly offered as available for sale in the year to date for 2026 averaged -0.1% lower in most counties than the same time period a year earlier as of May.

In 2025, low-tier priced housing had the lowest level of inventory available for sale or rent. No surprise here, as today’s mid- to high-tier pricing is out of range for most of our employed population.

Consider this: wealthy buyers are historically the first to taper acquiring property and cause an earlier buildup of excess high-tier inventory than occurs in lower tiers. Thus, a decline in pricing occurs first in high-tier priced housing followed by mid-tier, then low-tier housing.

The wealthy experience a decline (or increase) in their income before jobholders do. Profits and interest from investments decline before growth slows in jobholder numbers, then peaks and eventually declines as California witnessed in 2025.

However, 2026’s uncertainty around employment, trade taxes, and rising costs — especially in areas like construction — all contrast against buoyed Wall Street investments kept high by a corporate dash to build up AI. The faux build up inverts the cycle, so workers are the first to feel the effects of the looming, but yet to be announced, recession.

Today’s high price point levels asked by sellers and the cyclically higher mortgage rates force buyers reliant on mortgage funding to either:

- wait until sellers reduce their price demands significantly; or

- buy cheaper housing.

Compounding the drag on sales volume, mortgaged homeowners who purchased or refinanced in the past decade are less willing to sell and relocate to an upgrade when mortgage rates and payments greatly exceed those on their present mortgage. Pandemic refinancing is now inhibiting turnover, a significant factor reducing transactions and broker fees. Assumption of pandemic mortgages by buyers without lender interference is one solution but is not yet considered by seller agents to expedite sales volume.

Additional drags on seller willingness to turn over their occupancy and ownership are the readily available reverse mortgages for retired owners of single family properties and ADU permitting on the rise for most homeowners.

Further, the California real estate recession, underway since mid-2022, has worsened with the sudden 2025 destabilization of global immigration and trade arrangements. Recessions are cyclical events, typically ushering in job and property value losses.

These income and wealth losses place highly leveraged property owners in the position of unconventional sellers. As forced sales, for-sale inventory is added without the seller purchasing a replacement property. Once forced to sell, these sellers tend to become long-term tenants to satisfy their housing needs.

The growth of inventory available for sale has consequences: prices of property begin to decline as sellers seek to attract a buyer from a reduced number of potential consumers of housing. Buyers, confronted with swelling choices and declining prices, initially tend to take a wait-and-see approach before they are willing to step up and acquire a property.

No fear of missing out (FOMO) remains today. The buyer retreat presently underway ends when buyers perceive prices have reached their bottom level and several months of sales activity indicates prices are on the rise.

Looking ahead, expect for-sale inventory to increase in 2026 and beyond until the first drove of speculators enter the market as buyers, not likely an influence before 2028 without a crash in stock or commodity markets.

Chart update 6/22/26

| May 2026 | May 2025 | Annual change | |

| Los Angeles for sale inventory | 25,600 | 25,700 | -0.4% |

| Riverside for sale inventory | 17,200 | 18,600 | -7.6% |

| San Diego for sale inventory | 8,100 | 8,300 | -2.6% |

| San Francisco for sale inventory | 9,000 | 10,500 | -14.7% |

| San Jose for sale inventory | 3,400 | 3,400 | -0.6% |

The previous decades long enduring seller’s market fully reversed course in mid-2022 and has evolved to the initial stage of a full-blown buyer’s market. The shift to a buyer’s market in real estate began with the 2013 cyclical end to ever-lower mortgage rates after 1982, introducing our present roughly 30-year half cycle of generally rising mortgage rates.

As for real estate agents in property sales and leasing, a steady income from fees in 2026-2028 will require agents to consider a pivot in their practice to cash-heavy users of property, whether owners or tenants, residential or commercial.

A buyer with the willingness to buy property and ability to use accumulated wealth to acquire a home has a logic for buying now. The justification for the high price paid to purchase a property today, not later, is the offset in present value created by the widened difference between:

- the greater interest rate on a mortgage avoided by using savings;

- the high level of rental income for an SFR property; and

- the lesser interest rate lost on accumulated savings used to purchase the property.

The rental rate today for a property acquired using savings in an all-cash transaction exceeds the amount of interest no longer earned by the savings. With that, the opportunity cost of the amount of interest now lost is far less than rent for the property acquired. This logic is further justification for paying today’s higher price for property as ownership itself is not strapped with high mortgage rates for the price paid.

Buyer interaction with the gatekeeper agents is now enhanced by the 2025 advent of written representation agreements. Buyer confidence in the acquisition of real estate is greatly improved when a written representation agreement is used by an agent who expects to earn – and keep – a fee for assisting a buyer.

Expect property prices to bottom around 2028, but only when government chaos is controlled. As always, a timeline is complicated by disruptions in jobs and attitudes brought on by abnormal shifts in economics due to international turmoil and the vicissitudes of inconsistent government action.

Related article:

The cure for an inventory shortage

California’s decade-long inventory imbalance and related housing crisis of low-tier availability have two reasonable bases for resolution:

- decreased demand, via an increase in the number of occupants per existing dwelling or parcel of real estate, a recession-related phenomenon; and

- construction of residential units, enforced and funded by state programs, such as the state pension fund, for low-tier priced housing necessary to support the local workforce.

The years beyond 2026 will see a bit of both. Residential construction is, complicated by the cost of materials affected by trade taxes.

Homeownership is below normal rates and rental vacancies are greater than normal rates for the present level of household income in California. This occupancy stress is due to local and statewide inability – resistance – to permit new construction of housing units sufficient to house individuals employed in a community. The concept of “live where you work” is yet to catch on with local policy makers.

To that end, several pieces of new legislation since 2017 focus on the construction of more dwellings in California communities. However, only a few inclusive communities willing to deliver long-term housing policy have addressed the permitting issue with a positive reaction. Some officials in coastal communities need judicial enforcement to allow permits for additional low-tier housing to skirt the politically pervasive NIMBY crowd.

Unless a community permits low-tier housing starts, the community will need rent control ordinances to house those families employed locally. It’s one or the other, as coastal communities have discovered.

Related article:

{kind=link}

It’s easy to focus only on home prices, but the balance between supply, buyer demand, and affordability tells a much bigger story. Articles like this help make a complex market easier to understand, especially for first-time buyers and anyone keeping an eye on where the real estate market might be headed.

Very insightful analysis of California’s housing market trends. The explanation about rising inventory and changing buyer behavior is clear and informative. It really helps understand how market conditions are shifting and what buyers and sellers can expect in the coming months.

Analyzing California’s home inventory is vital for real estate professionals. While predicting market trends isn’t as simple as playing Easy Games, staying updated on supply levels helps in making better investment choices. Great data for the 2026 forecast!

Finally seeing some of these luxury listings sit for a bit is long overdue. Curious to see if sellers actually drop their prices or just keep holding out for a miracle.

So you’re saying the inventory growth outpacing owner need to sell is driven by wealthy buyers pulling back, which usually causes high-tier pricing to decline first. Makes sense, given their investments take a hit before lower-income households feel it.

Focuses on Blox Fruit and Defense stats. Ideal for those who enjoy magical, high-range combat.

If the lender finds a lease agreement with a duration that is greater than three years, they have the legal right to call in the mortgage.

Carrie –

With all due respect, the low housing inventory has little to do with interest rates. In past years, interest rates have been as high as 10% without having this kind of impact on sellers reluctance to sell their homes. The real culprit is capital gains tax. The federal government has failed to adjust the exemption amount in over 25 years. People don’t want to pay a huge tax bill just for selling their home. Email me if you would like more info.