Here is the final post in our new study series — Down payment download — breaking down the purchase costs and ownership expenses a buyer, as guided by their buyer agent, is prepared to expect. This series is designed to educate a buyer agent advising a prospective homebuyer on the costs of owning their residence, emphasizing the extensive financial literacy required to intelligently take out a mortgage.

Every DRE licensed agent asking a potential buyer to trust their judgment finding them the right property must also understand and communicate the financial consequences the transaction they arrange imposes on their buyer’s budget, income and down payment decisions.

Read the previous installment: Down payment download: Mind your mortgage

Why this matters: A real estate broker and their agent retained by a buyer to guide them through the house-hunting, mortgage and closing process to own their residence need to know what is and isn’t obvious to their buyer-clients, especially first-time homebuyers. Competent brokers and agents inform and educate buyer-clients by breaking down the acquisition process into down payment consequences, transaction costs and ownership expenditures.

Mortgage in, rent out, the trade for ownership

Homebuyers learn a lot about compromise during the house hunting process: bigger closets mean smaller bedrooms, the view in exchange for the commute, a backyard or a pool. The priciest trade of them all: turning their hard-earned cash spent on rent into a mortgage — and ownership.

When buyers are setting their homeownership budget, they typically are sheltered from the full scope of fees, costs, and financial tradeoffs associated with the acquisition of mortgage-funded home ownership.

But mortgage insurance and interest rates do negatively affect buyer purchasing power and, in turn, the amenities a buyer can afford compared to renting. And now, current high property prices following the post-pandemic buying spree clash with cyclically rising mortgage rates.

Today’s diametric collision of these two market situations – high price, high mortgage rates – forces buyers to wait until prices fall into line and a 20% down payment is accumulated. Meanwhile, sales volume declines and inventory for sale rises.

Until pricing adjusts, buyers and their agents need to mull over estimates of the costs to acquire and maintain homeownership. Further, cautious buyers who are curious learn about the relationship between monthly mortgage payments and the cost of owning a home versus renting. The analysis starts with a discussion about choices for the size of the down payment.

Related article:

Multiple sticker shocks

Consider a home priced at $500,000 and a buyer who is prepared to make a 20% down payment, plus closing and moving costs as well as holding a six-month cash reserve. Given recent mortgage rates and a buyer with good credit, we’ll estimate a 6% fixed rate mortgage (FRM) and a monthly principal and interest (PI) payment of $2,400 – 31% of the household income of the buyer.

With their down payment of 20% in hand – $100,000 – the buyer is positioned to make a series of decisions that greatly affect their financial health as a homeowner.

The buyer needs to consider transactional costs to simply acquire a home, in addition to the down payment, for:

- mortgage points, including any discount points;

- necessary 3rd party property reports;

- mortgage insurance (MIP or PMI) for down payments less than 20%; and

- any costs associated with selling or leasing out their current home.

These costs and financial penalties become repressive for every mortgage funded purchase of a home when the down payment is less than 20% of the price. However, we’ll continue the prior example of a $500,000 home with a 20% down payment as a stand in for the costs of buying and owning.

Related article:

A hypothetical home

For buyers lacking a 20% down payment, mortgage insurance premiums, discussed at length in earlier parts of the Down payment download series, add a monthly cost payable to the mortgage holder at an annual rate of around 0.7%. Also, the higher rate of interest is incurred on the larger mortgage amount borrowed – which a 20% down payment eliminates.

No matter the amount of down payment, to avoid paying the current par rate of interest for a mortgage, buyers can proactively lower the interest rate by paying mortgage points at time of closing, Lenders accept mortgage points, each equal to 1% of the total amount borrowed, in exchange for a decrease the annual mortgage rate by 0.25% for every “point” paid.

In our $500,000 example home with a $400,000 mortgage, a buyer can spend $4,000 at closing to “buy down” the annual interest rate from 6% to 5.75%. Over the life of a 30-year $400,000 mortgage, the homeowner saves over $18,300 for their $4,000 investment today. The purpose of a buy down is to qualify to borrow a greater sum of money with the same monthly payment.

Buyers may need to invest in 3rd party reports before closing on a sale, such as a home inspection report (HIR) when the seller has failed to provide one. This due diligence by the buyer enables them to demand and force the seller to correct or eliminate any defects undisclosed before the seller accepts the buyer’s purchase agreement offer. An HIR reduces the risk of coping with knowable defects first discovered after taking ownership of a property.

A first-time homeowner need not be hit with a shock due to undisclosed, and thus unexpected, costs that normally arise from ownership. Investing in a home is rewarding as a tool to build up wealth, but ownership requires management. And management requires knowledge of what costs to expect before thoughtful decisions can take place.

Related article:

Homeowners spend how much on what?

Going back to the $500,000 example, a perspective homebuyer can estimate property ownership expenses based on the home’s:

- age,

- maintenance,

- upgrades,

- value, and

- specific location.

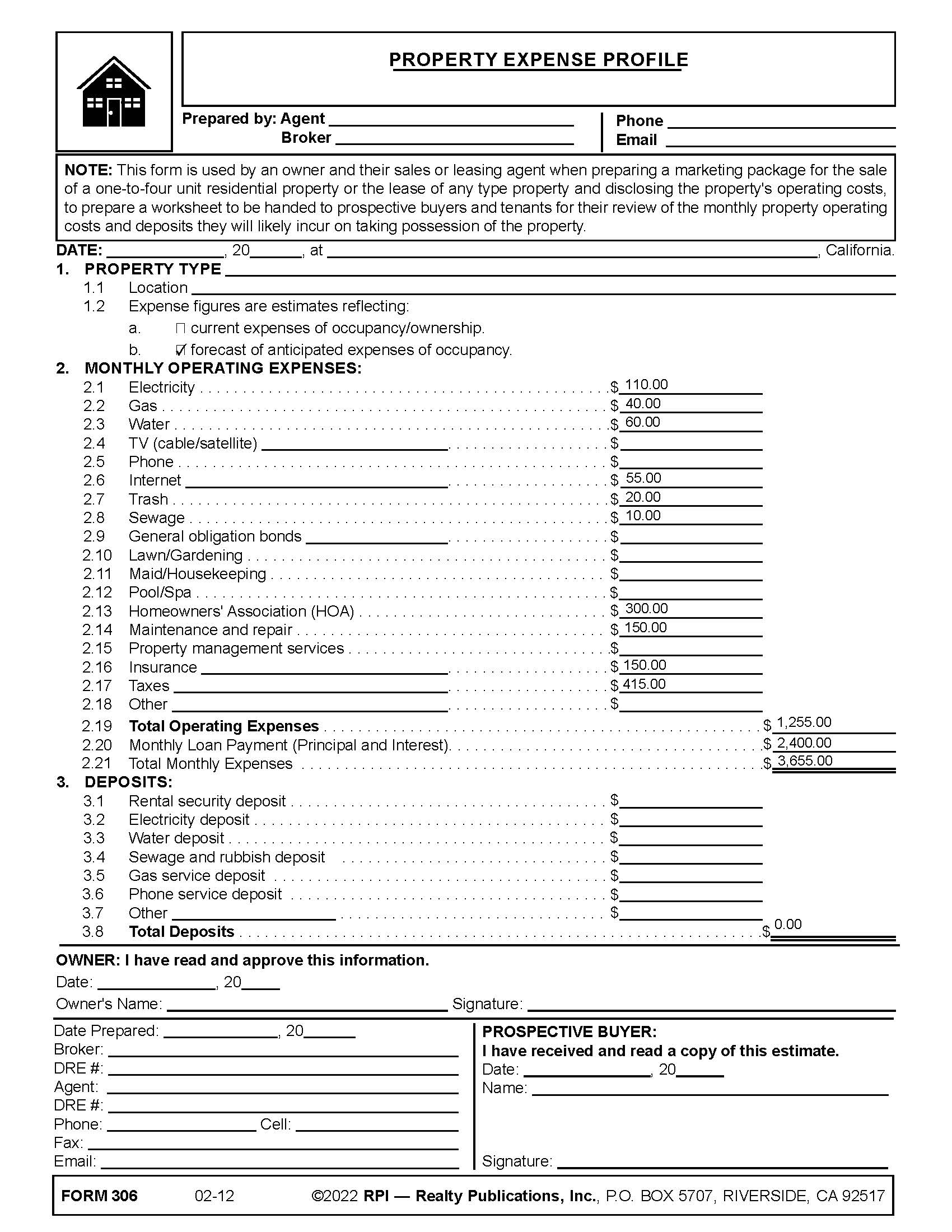

Property taxes are about 1% of the buyer’s purchase price. They are not the amount of property taxes the seller pays. The taxes for owning a property rise 2% annually. Thus, they do not increase more than the Cost-of-Living Adjustment (COLA) wage increases in the future.

Because a 20% down payment homeowner pays property taxes annually, not monthly, taxes must be budgeted and set aside monthly in a reserve account. They are disbursed annually in one or two installments. For the example home, an owner pays $5,000 or a bit more in property taxes – $425 monthly – the first year of ownership.

For homeowner insurance coverage required by the mortgage holder, as well as being a necessity for the largest financial investment in most people’s lives, the premiums are volatile — that is they rise, often alarmingly. The annual premiums rise primarily due to the rising costs of replacement materials, rising risks of wildfires and the effects of climate change in the area. Our example — barring any high-risk complications — is expected to budget around $150 a month, set aside as reserves for paying the annual premium.

A more familiar expense — utilities and government service fees — are costs renters understand since they have likely dealt with them before. But there are other charges to be considered, leaving bills closer to $150 to $250. These include public services such as:

- garbage collection;

- street lighting; and

- water bills.

Owners also bear responsibilities that renters do not, primarily covering all maintenance and repairs required for the ground area and improvements. Owners also are responsible for internal upkeep, to keep the property neat and something to be proud of. A homeowner in our example budgets and sets aside $150 a month for routine and surprise maintenance.

When a homeowner belongs to an HOA they do not directly incur these ownership obligations. With an HOA involved, the owner pays monthly HOA fees which include the costs of care and maintenance of grounds and improvements.

Those in an HOA are informed by mandated HOA disclosures provided by the seller broker before making a purchase agreement offer. For our example, the current monthly HOA fee is around $300.

All totaled together, the range of ongoing homeownership costs exists between $870 to $1,270 a month for a $500,000 home. Like all budgets, there are opportunities to trim and save, but these costs will be there and are in addition to the mortgage payment.

Practice best practices

All of the information above is communicated by the seller and their agent using a Property Expense Profile. These are facts known to the seller and disclosed to potential buyers since they affect decisions regarding ownership of the property. [See RPI Form 306]

Editor’s note — RPI Form 306 is used by a seller broker when marketing a one-to-four unit residential property for sale. This form is used in collaboration with other disclosures discussed here.

Delivering information buyers need to make decisions is referred to as the disclosure of material facts. What the seller knows about the operating conditions and costs gets bundled into the marketing package the seller broker delivers to prospective buyers and their agents.

When a seller agent fails to perform their due diligence work to provide a comprehensive property operating cost sheet, the default requires the buyer agent to prepare and submit estimates for the seller’s correction and approval. Skipping this informational step deceives the buyer about the reality of the property.

The seller and their agent have no escape route to avoid disclosing what they know about a property since the information might affect a buyer’s decision about buying or the price to be paid.

Related article:

A virtuous cycle

As agents and brokers reach out to potential clientele, encouraging renters to make that first step into homeownership, they are rewarded by then working with an informed and prepared client. No surprises and no illusions.

Not only do agents advise buyers to locate and select a home, they are also the experts first-time buyers look to for advice on all things real estate. Financially prepared homeowners have the tools to turn their new house into an asset that builds future wealth instead of draining it.

Client relationships are critical over time for real estate agents. Trusted agents get referrals, and referrals are the heart of a sustainable livelihood from real estate fees.

Related article:

{kind=link}