Why this matters: Without turnover of residential and commercial occupancy, whether by tenants or owners, the use of real estate brokerage and construction services languish along with earned fees and profits. Mortgage rates slip during business recessions but have been in an upward trend since 2012 and are expected to continue for around two more decades.

Pricing of real estate rents and sales are way too high to compete with today’s demographics and mortgage market conditions — on average, household size is increasing and businesses are downsizing. Meanwhile, real estate agents and builders are left to cope and advise until the price paid to occupy real estate adjusts.

Unpacking the rate of packing to move

Turnover rate measures the number of tenants and homeowners who aren’t in the same home they were a year ago. This percentage demonstrates a move down the street, across the country, or switching their category of occupancy entirely — tenants becoming homeowners and homeowners relocating or renting.

Home sales since the recent peak in 2021 are stagnant. As anticipated, 2025 is forecast to end with home sales volume slightly below a year prior. However, California’s homeownership rate remains near the historic norm, at 55.3% as of Q2 2025, holding to an unsurprising pattern.

Mortgage rates since 2013 are on a long-term upward trend likely for a couple more decades, temporarily deviating downward for recessions during the rate cycle underway.

However, prices holding flat since 2021 are stubbornly adjusting to offset the adverse effect cyclically rising mortgage rates have on buyer purchasing power, similar to conditions between 1964 and 1980.

While turnover of homeowners and renters generally rise or fall in tandem, renters’ more mobile lifestyle produces a far greater annual turnover rate. Even when a renter makes the jump into homeownership, their move out of a rental unit creates an opening for another household to move in.

The level of turnover directly equals the level of fees for real estate agents and brokers in sales and leasing. Up or down, the direction of turnover reflects the trend in fees generated from sales and leasing transactions. And the same for builders.

Brokers acting as property managers earn fees from clients for locating tenants, collecting rents, coordinating maintenance and accounting. This fee-based management service is often credited as recession-proof. It is a stable and more consistent source of income than the single-event fees collected by leasing, sales or MLO agents.

Related article:

What is the turnover rate now?

Understand that turnover is a lagging indicator of economic conditions in real estate. Turnover only reflects conditions after the moving boxes have been put away and people are settled into their new homes. Turnover rates move based on changes in leading factors, such as:

- mortgage rates and by extension, buyer purchasing power;

- job market conditions;

- costs to occupy a property (owned or rented);

- inventory levels for sale or lease;

- a rise in debt delinquency and bankruptcies; and

- external conditions affecting consumer caution such as:

- international and domestic turmoil; or

- inconsistent government action or conduct.

When these conditions shift, the end result is an altered trend for turnover and fees.

Also, turnover rates are very location specific. Different metro areas across California feel the changing economic and demographic forces affecting their population differently.

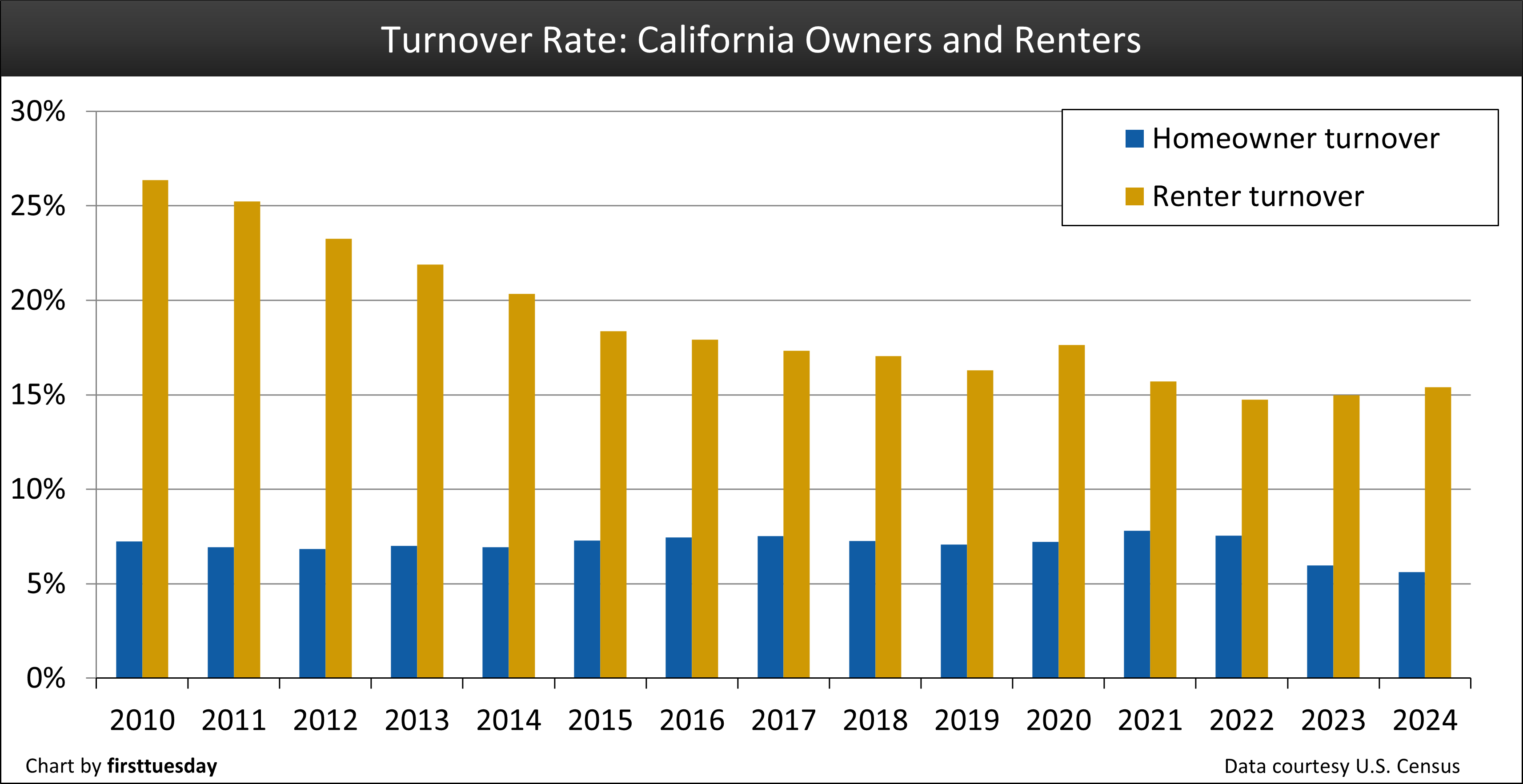

As a state, California’s turnover rate is low, but not yet stalled. 2024 saw 15.4% of renters move and 5.6% of homeowners. This is down significantly from a general statewide peak when the Great Recession wound down by 2010 and over 26% of renters moved annually and 7% of homeowners changed their residence.

Chart updated 10/14/2025

| 2024 | 2023 | 2010 | |

| Homeowner Turnover Rate | 5.61% | 5.98% | 7.24% |

| Renter Turnover Rate | 15.39% | 14.97% | 26.36% |

Data courtesy of the U.S. Census

Annual data detailing the turnover rate experienced by California generally and for specific metro areas as collected by the U.S. Census, is provided by the American Community Survey (ACS) seen in their regional chart.

The taller, yellow bar represents the percentage of California renters in a new residence since a year ago. The trend downward in renter turnover since 2010 was interrupted by 2020, when a variety of factors from the pandemic lockdown pushed renters to seek different housing.

Homeownership turnover, above in blue, has smaller changes year to year, and was consistent after 2010 while recovering from the Great Recession of 2008. The rate of homeowner turnover in 2023 and 2024 marked a departure with a sharp decline now anticipated to continue into 2027 as caution entrenches itself.

Related article:

Neighboring economic factors

For property managers and landlords, long-term tenants offer stability in occupancy rates and income. Conversely, a decline in turnover without new construction stops growth in for-sale inventory and leaves prices to rise when local populations grow.

Also, low turnover suggests residents have become cautious about making logical job changes or improving their standard of living. Of course, these are conditions experienced mostly in recessions rather than during periods of economic upturn.

Lower employment —fewer job holders and no hiring of replacements — increases turnover but without relocating through renting or buying. Rather, households consolidate by living with family, friends, or roommates to ease the burden of California’s especially high rent. With living costs increasing at a faster clip than annual income adjustments, an unstable job situation can quickly devolve into homelessness.

Further, the hiring freeze observed in 2025 encourages caution among the employed to avoid taking on more debt obligations for housing and new purchases.

Although income kept up with higher inflation rates over the past decade, it failed to match the pace of rising rental and mortgage rates. This financial one-two punch traps tenants in increasing rental obligations which are less than the total expense of owning a comparable quality of living. Without large pay raises or a deliberate reduction in a tenant’s standard of living, excessive rents leave no room to build up savings for a down payment. Mortgage rates have risen far faster than annual pay making ownership by standby homebuyers illogical as presently priced.

Today, more than half of Californians are rent burdened — spending far more than the recommended 1/3rd of their gross household income on housing — unable to save the 20% down payment needed financially to prudently invest in homeownership or other opportunities.

This leaves sellers waiting while they watch more housing inventory stand unsold for longer and longer. As real estate recessionary conditions evolve, large vacancy ratios and year-long unsold property weigh on the market to invoke the turnover of the 2008 Great Recession. Those years were an uncomfortable time for brokers, MLOs and builders looking to finance and move property.

Today, renters who save enough to pay the upfront costs to purchase a home expect to pay the same dollar amount on mortgage payments and property ownership costs as they spend renting. To meet this budgetary condition means a quality downgrade from the amenities they currently experience as a tenant for the same monthly costs.

A tenant looking to move to a new rental is obligated to save for moving expenses and two months’ rent (recent legislation capped the upfront deposit) in addition to application fees, time off work to view housing and resetting their usual routines.

Replacing or transporting household belongings is an expensive and sometimes intimidating task. Leaving little room to wonder why turnover in 2025 is at a low moment.

Related article:

The connection between renters and homeowners

Looking across the US today, California possesses the least affordable rents in metro areas in three of the top five offenders: Los Angeles, San Diego, and Riverside.

In a confusing case, the state of California offers significantly more financial support to homeowners compared to renters, as reported for 2025 by the California Housing Partnership. California spent $6.53 billion on homeowners, the majority being tax avoidance by mortgage interest and property tax deductions.

In contrast, tenant assistance spent by the state was a third of homeowner assistance with tenants receiving tax credits, the Affordable Housing Sustainable Communities Program benefits and new construction incentives. But unlike homeownership programs, only 25% of tenant programs were permanent as opposed to 97% aimed at homeowners. Housing policy at the state and federal level was built to keep builders and homebuyers more prosperous, not landlords and their tenants. The issue is unequal treatment in housing by the state.

Tenants today in California trade the longevity of occupancy accompanying ownership for higher quality amenities offered by a rental at the same monthly cost of housing. The downside of future uncertainty in rental housing arrangements is offset by a tenant’s greater flexibility and choice finding a better future job location.

Homeowners during the decade prior to the 2022 buildup in available inventory for sale became used to deciding when to reenter the housing market to sell and relocate. However, mortgage rate increases after 2021 are a reminder that owners aren’t in control of when their home sells or the price they can get during a real estate recession.

Another issue for homeowners faced with the current buildup of for-sale inventory and cyclically higher mortgage rates is the changed conduct of prospective homebuyers since 2021. Buyers today are more likely each year to wait for property prices to bottom before they are willing to house-hunt and make offers to buy.

The present behavior in the real estate market by both tenants and existing homeowners stalls turnover leaving speculators to acquire a rising percentage of homes in 2025 compared to owner-occupants.

Related article:

The family that sticks together grows the household

Recessionary trends consolidate family and friends as money saving housing arrangements are sought out to combat high rents, high prices, and job insecurity or loss. These room-sharing or common-living arrangements are affecting households on both sides of the generational divide. Both are feeling stuck — Boomers as owners of largely unused homes and Millennials and Gen Z members as tenants increasingly unable to hurdle into homeownership for lack of savings and borrowing capacity.

Today’s consolidation of households increases the average number of members in statewide households by reducing two prior households into one.

Average household size in California rose in 2024 compared to a year prior. The rise marked a change in trend since household size peaked for renters in 2014 at 2.94 and, as expected with the following recovery, homeowners in 2017 at 3.03. Household formations will not pick up to reduce the number of people in a household until job numbers increase, likely in the next recovery expected to begin around 2028.

Since 2006, homeownership in the region dropped 28% for people aged 25 to 34. At the same time, homeownership among the Baby Boomer generation held steady. Major contributors to this generational difference in rates of homeowner are:

- student debt, which eats into the debt payment ratios MLOs use to qualify borrowers to originate a mortgage; and

- mortgage rates, which have doubled in the past decade.

A responsible MLO following SFR mortgage guidelines limits:

- mortgage related payments to 31% of gross household income; and

- the total of all household installment payments at 41% of income.

After the Millennium Boom ended in 2007, homeownership rates dropped swiftly, adversely affecting over a million California homeowners and their households before changing direction in 2013. For the Millennial and Gen Z renters, this memory of personal and family financial stress, student and credit card debt obligations, increasing living costs, and the recollection of job losses during the Great Recession and pandemic economy have put a mental if not financial hold on their homeownership plans.

However, consolidation of households does produce turnover. When households form or enlarge due to consolidation by including relatives, friends or cost sharing roommates in one housing unit, their move to save on rent or mortgage is a measure of turnover — a vacant housing unit now available for sale or rent.

Unlike other moves, consolidation arrangements alone produce zero broker and MLO fees, except possibly for the property vacated. No agent is involved when an additional occupant is added to enlarge the household already owning or leasing a housing unit.

When job growth does not exist and is slipping in most parts of the state — as is in the case in 2025 — this turnover is increasing the inventory of unsold or vacant property.

The inventory buildup becomes especially noticeable in different metro areas when California’s bedroom city population has chosen to live far from where they work and commute. Urban cities with high-cost housing also see their workforce leave in favor of working from home with their digitally connected office space in less expensive communities.

Related article:

Why is turnover helpful?

With a responsible agent looking at as many indicators as possible to assist with anticipated changes to their local real estate market, what is the value in knowing the measurement for a trend that has already happened?

For starters, any agent looking to understand a new community examines more detailed information than simply knowing how many people rent or own.

It is the rate people relocate that heralds growing or shrinking numbers of fee-producing transactions — important during a real estate recession when agents and brokers need to reexamine which income-generating services they’ll offer and to whom.

Turnover also reflects the direction of consumer confidence. Watching household moves into or out of a neighborhood affects buyers:

- experiencing fear of missing out (FOMO);

- saving more or less for a down payment; and

- waiting to spot a bottom in pricing during a recession after which hesitant buyers choose to act.

On the other hand, turnover fuels seller’s:

- willingness to drop their sticky asking prices;

- willingness to price right when reviewing comparable sales prices; and

- estimates on their ability to buy property after selling theirs.

Related article:

How agents and brokers can encourage a move

Recent changes to legislation promote renters making the change into homeownership. From restricting the amount of a security deposit a landlord may demand to rewarding positive reporting of timely rental payments to improve a tenant’s credit scores, renters become better qualified buyers.

But a homebuyer needs to save 20% for a down payment to avoid hefty money charges imposed as a financial penalty for down payments less than 20%. All participants in a home purchase transaction are covered for any loss, except the less-than-20% down payment buyer.

In addition to promoting the switch to homeownership, agents offering services as property managers make data driven decisions to encourage moves like offering more pet friendly rentals and watch turnover data to better understand and find local clientele.

Related article:

{kind=link}