Why this matters: Student debt affects the long-term savings, mortgage debt-to-income ratio and confidence level for much of the next generations of first-time homebuyers. Understanding how to cultivate potential buyer clients from renters typically means guiding graduates shackled with student debt through their housing options.

Give it the old college try

Student debt is generally incompatible with mortgage financing. Debt negatively affects borrowing capacity due to the homebuyer’s debt-to-income ratio (DTI) applied by MLOs.

Since 48% of college graduates are financially burdened with student loans, according to the Federal Reserve, an agent advising a first-time homebuyer must confront the student debt issue. Most of an agent’s college-educated buyer clients must weigh their first home purchase selection with:

- college debt they must pay; and

- savings of less than a 20% down payment.

In 2025, the group in California with the largest number of borrowers was 25 to 34-year-olds. However, the largest amount of student loan debt by dollar amount per borrower was held by 35- to 49-year-olds.

As tuition costs rise faster than earning expectations and interest only student loan payments postpone paying down the principal debt, graduates tend to fall deeper and deeper in debt as they get older. 18% of student borrowers have a student loan balance between $40,000 and $100,000.

Those who leave without a degree are stuck with the loans they took out. In California, the default rate on student loans by non-graduates was twice the number of those who finished their degree. This information suggests these individuals are doubly punished by taking on debt and missing out on higher pay.

Student debt is pervasive among first-time buyers — and it cuts deep into their mortgage borrowing capacity and the amenities in a property they qualify to acquire.

Why do so many people have student debt?

The reasons behind the rising trend in student debt include:

- the cost to attend college continues to increase unrealistically (since colleges can charge more without affecting enrollments);

- the number of individuals aiming to attend college remains high; and

- government insured student loans are available to finance the education of most students.

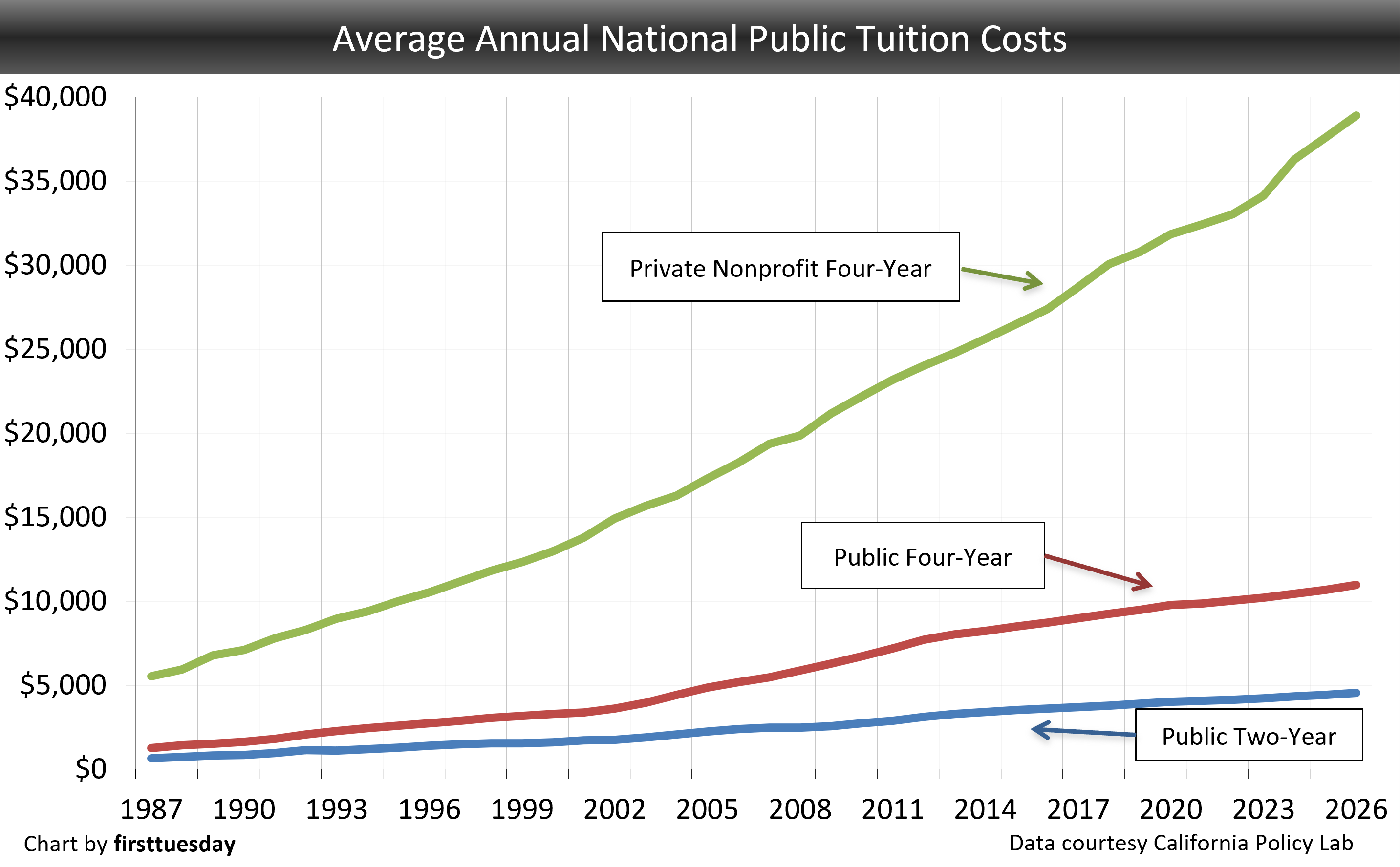

To get specific, the average tuition and fees for a four-year public college or university in California during the 2006-2007 school year was $4,549. Five years later, in 2011-2012, it was twice that at $9,022. By the 2025-2026 school year, the average in state tuition and fees held at $9,310 with out of state students coming to California paying a dramatic annual price tag of $34,814.

The number of individuals attending four-year public colleges or universities in California grew 16% from 2000 to 2010. In 2010, there were 642,000 students enrolled in public four-year institutions in California. However, after college enrollment dropped during the pandemic, the 2024-2025 school year had only 546,500 enrolled students in the four-year public schools within the Cal State and UC school systems.

Editor’s note: The differences between colleges and universities are slight and mainly organizational. Student loan statistics do not vary based on whether the four-year degree-granting institution is labeled a university or college. However, public and private institutions present a stark difference, as tuition and fees are much higher at private institutions.

In decades past, governments paid for the public college education of many young people. The most significant instance is the GI Bill, first passed in 1944. This bill provides for the education of service members, as well as loan guarantees for homes and businesses.

Following World War II, students attending school on the GI Bill made up half of all college students, according to the U.S. Department of Veterans Affairs. When these students graduated, they were able to obtain higher paying jobs and pay for housing amenities they otherwise had no access to. The housing boom of the 1950s ensured a jump in the homeownership rate that lasted until the 1980s.

Fast-forward to today’s government paid education: The latest statistics have students attending college with Post-9/11 GI Bill benefits at roughly 492,000 students nationally, according to the Postsecondary National Policy Institute. With 18.6 million students currently enrolled in degree-granting, postsecondary institutions nationwide, that’s about 2.5% of all students enrolled under the GI Bill. The difference is troublesome for savings rates and future homeownership, particularly for Millennials and Gen Z.

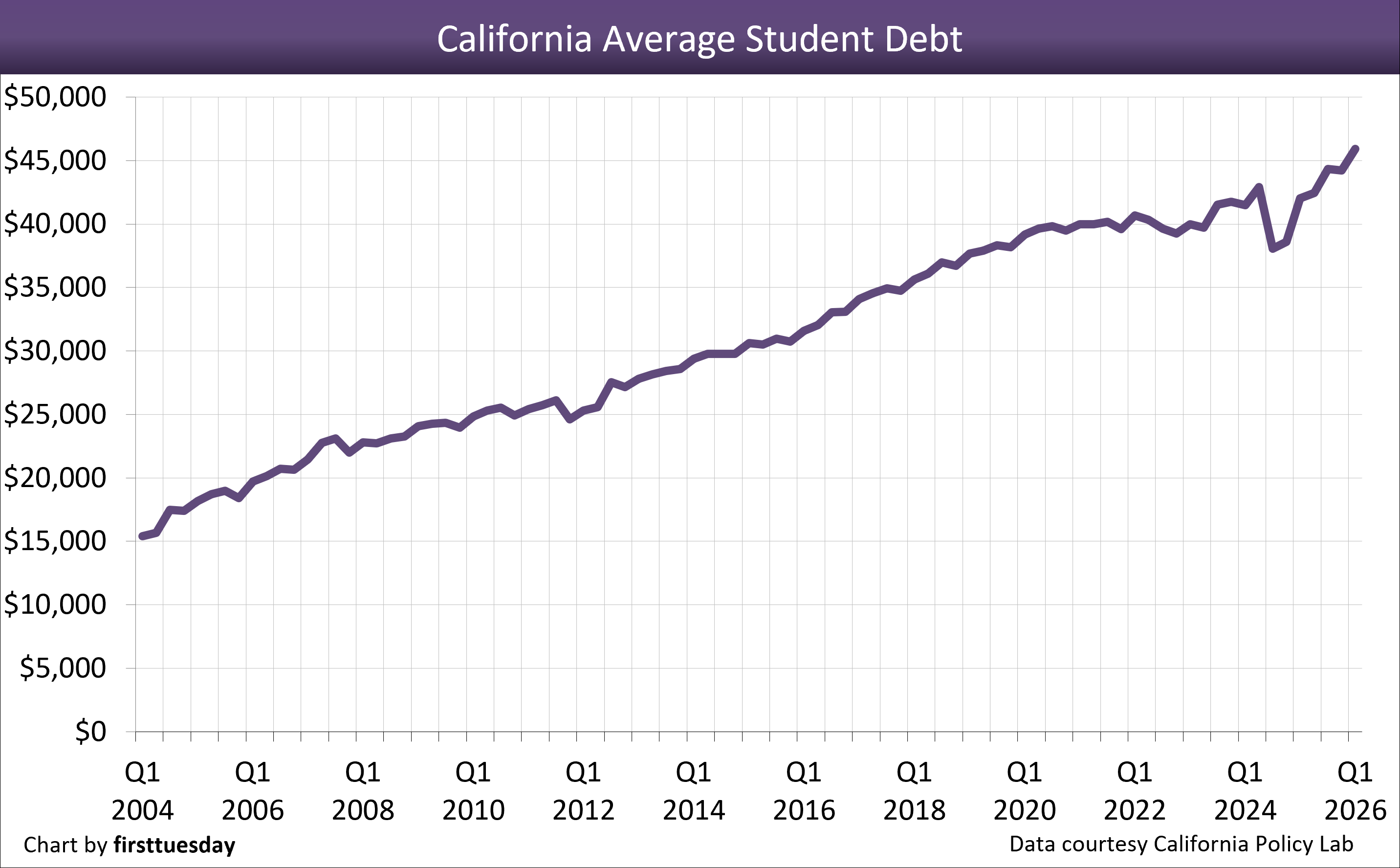

Chart 1 Chart update 7/21/26

Chart update 7/21/26

Q1 2026 | Q1 2025 | Q1 2024 | |

| Average student debt in California | $45,900 | $42,000 | $31,600 |

Chart 2 Chart update 7/21/26

Chart update 7/21/26

| 2025-2026 | 2020-2021 | 2015-2016 | Ten-year change | |

| Private Nonpublic Four-Year | $38,900 | $32,400 | $27,400 | +42% |

| Public Four-Year | $11,000 | $9,900 | $8,700 | +26% |

| Public Two-Year | $4,600 | $4,100 | $3,600 | +26% |

The problem for housing sales and leasing

While alarming in a general sense, the rising tide of student debt presents a tricky obstacle for California’s housing market and the agents whose practice is home sales or leasing.

On the one hand, higher education is essential to obtaining a high-paying job. For instance, the median wage for four-year college graduates is 68% more than the median wage of those with only a high school diploma, according to the Federal Reserve Bank of New York. For local economies, jobs held by graduates are a great boon to the local housing markets. For property owners, communities with high-skilled jobs requiring college degrees foster greater investment and higher home prices and rents with more stable demand from end users – these higher paid graduates.

In contrast, today when obtaining a college degree means accruing tens of thousands of dollars of student debt even before starting a career. An initial home purchase — particularly in high-priced areas where the best jobs are located — is increasingly beyond reach. The result these days is fewer new homes are built than are needed to house household formations as took place when education was mostly free of cost.

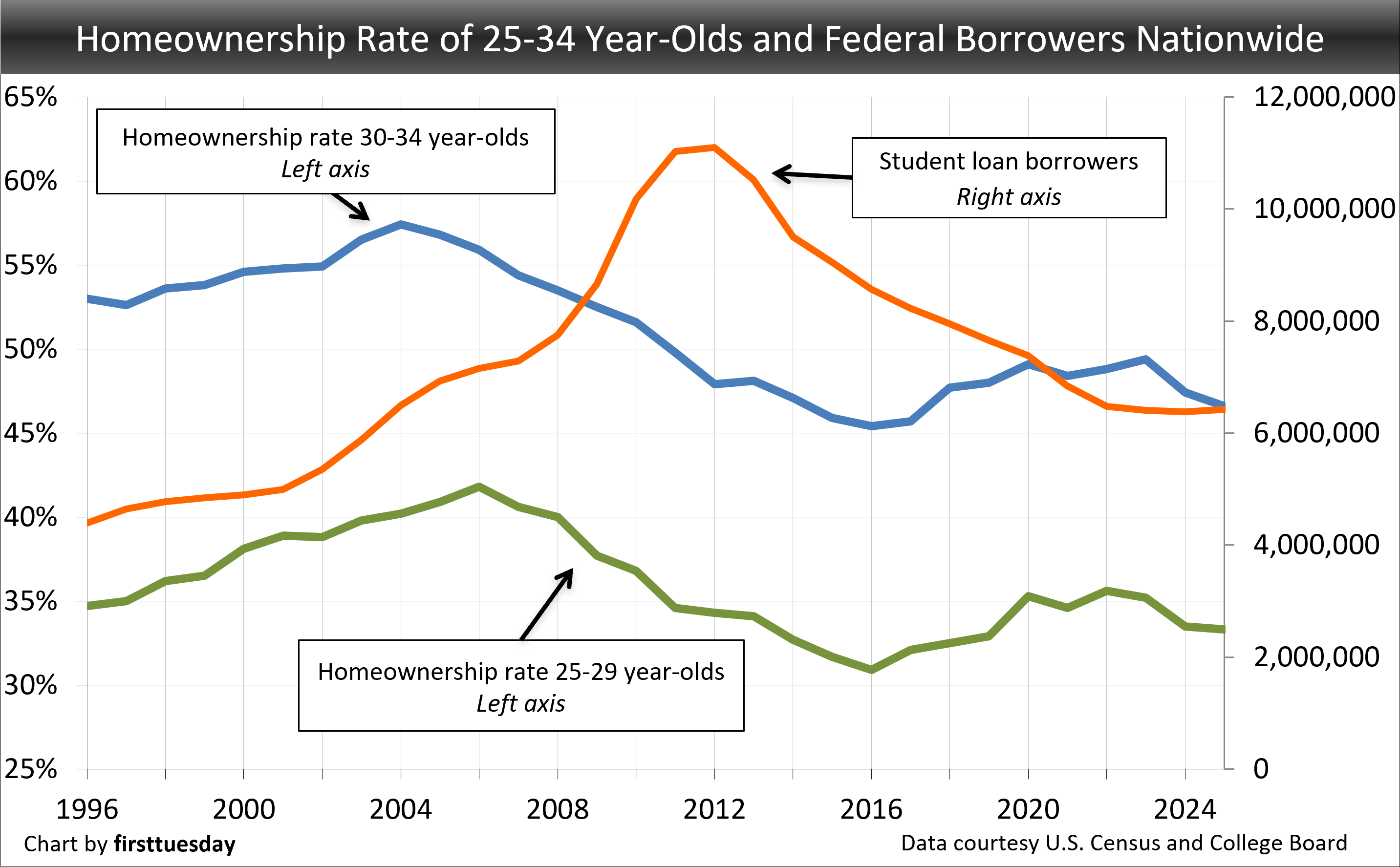

As evidence, the decrease in the first-time homebuyer demographic (those aged 25-34) corresponds with the recent decades’ swift rise in federal student loans.

Chart 3 Chart update 7/15/26

Chart update 7/15/26

To be fair, the decline in homeownership amongst the traditional first-time homebuyer demographic can also be attributed to a number of factors. These include:

- persistently high rates of unemployment in the wake of the 2008 recession and 2020 pandemic lockdown as well as the population’s declining participation in the labor force;

- for those who are employed, underemployment exists in jobs for employees who don’t need a college degree; and

- of course, the reduced savings and decreased capacity for manageable mortgage debt due to the ever-increasing weight of student debt.

The good news: homeownership rates were on the rise for young people after reaching a low in 2016. Today, homeownership remains a milestone and financial goal across generations, a fact not missed by agents in sales.

A buyer’s student debt continues to dissuade

However, even as first-time homebuyers return in greater force at the end of this decade, their shot at ownership prior generations achieved is stunted by the drag of student debt.

For example, consider a potential first-time homebuyer who is a recent college graduate. Their gross monthly income equals $4,000. Their monthly student debt payment is $450. This payment amount is based on the average U.S. student debt interest rate of 6.39%, paid off over the default repayment plan of ten years.

However, on top of their student debt payments, this borrower is also making a car payment of $300 monthly and has a monthly payment on credit card debt of $100 a month.

This individual’s monthly debt totals $850. Thus, their current DTI is 21%. However, it leaves insufficient funds for monthly housing costs and a savings plan.

A homebuyer’s maximum DTI, including housing costs and all other debts (the back-end ratio for mortgage borrowing) is 43% of their monthly income. Thus, in this scenario they qualify for a maximum monthly mortgage payment of 22% of their monthly income (the front-end ratio) – $880.

With this monthly payment, they qualify to take out a home mortgage of roughly $170,000 – but only if they come with a 20% down payment. In this case, coming up with a 20% down payment ($34,000) is unlikely, particularly when over 20% of their monthly income is already going toward paying down pre-established debt and any rent paid for housing. Further, home prices in most of California are well above the maximum mortgage funding this homebuyer qualifies to borrow.

The options for homebuyers with student debt

In most cases, student loan borrowers are set up for ten-year repayment plans. This means a set amount of their monthly income goes towards paying down their debt for a full decade. However, this doesn’t necessarily preclude them from buying a home until their student debt is wiped out.

One less than ideal way is to wait until their income rises. In a couple of years, our borrower, now earning $4,000 a month, may be earning $5,000 a month. This brings their pre-established debt from 21% down to 17%, bringing their acceptable front-end ratio from 22% to 26%. Now with a 25% increase in personal income, they qualify for a maximum monthly mortgage payment of 26% of their $5,000 monthly income (the front-end ratio) – $1,300 — a 50% jump in mortgage funding for purchasing a home.

Further, the couple of years waiting to buy gives them more time to build up savings for that 20% down payment.

However, this is complicated by how long they expect to be paying off their student debt. Again, the payment plan is 10 years, but on average it now takes graduates twenty years.

So, is there no way around the student-debt burden for a homebuyer? Is a real estate agent’s best counsel really to “wait it out?” Consider advice on restructuring the student debt payments.

Chart 4 Consider changing the repayment plan

Consider changing the repayment plan

Consider changing the repayment plan

Consider changing the repayment planHomebuyers with student debt payments have options to reduce those payments. With lower monthly payments, the percent of their income expended on student loan payments and in turn the percentage of mortgage DTI consumed by student debt is reduced.

The result is an increase in available mortgage funds to purchase a better-quality home now rather than waiting for personal income to rise.

Even though student loan debt is specific to the individual borrower, the agent may begin the conversation around loan modification by introducing these three federal plans:

- Pay As You Earn – caps payments at 10% of monthly income and extends the repayment schedule);

- Income-Based Repayment – caps monthly payments up to 15% of their income while offering full forgiveness at the end of a set extended repayment schedule; and

- Public Service Loan Forgiveness Program — for government employees or tax-exempt not-for-profit organizations.

Qualifying for these programs or similar loan consolidation or modification depends on:

- date of origination;

- when the borrower applies for modification;

- status of the loan; and

- other disqualifying factors.

Programs dependent on federal funding are especially vulnerable to changes with the current administration and may even end earlier than borrowers expect.

While an agent provides assistance, they need to be careful not to speak in guarantees on subjects they are not experts in.

An agent with adequate awareness of student loan debt not only prepares a potential homebuyer for a better financial reality, but also presents themselves as knowledgeable, compassionate and worthy of recommendation to other first-time buyer clients the borrower may know.

The path to payment

The Pay As You Earn student loan repayment plan caps a borrower’s monthly payments at:

- 10% of their monthly income; and

- extends the length of repayment from 10 to 20 years, at which time the remaining loan balance is forgiven.

To qualify, the individual must be a “new borrower,” which is an individual:

- with no Direct Loan or Federal Family Education Loan (FFEL) debt October 1, 2007; and

- who has received disbursement of Direct Loan funds on or after October 1, 2011.

Further, to be eligible for the plan, their new payments must be lower than under the standard repayment plan. Monthly payments are adjusted each year depending on the borrower’s changing income and family size but never exceed 10% of their household’s monthly income.

Enrollments are only open for new pay-as-you-earn applications until July 1, 2027. For more information, see the U.S. Department of Education.

An alternative payment arrangement is the Income-Based Repayment plan. When your buyer client doesn’t qualify for the Pay As You Earn program, they may qualify this income-based plan which ends July 31, 2028. This program:

- limits borrowers’ monthly payments to 15% of their monthly income when they borrowed before July 1, 2014, and 10% for borrowers after; and

- extends the repayment period from 10 to 20 or 25 years, at which time the remaining loan balance is forgiven.

A student loan borrower qualifies for this plan under any Direct Loan or FFEL loan balance. Monthly payments are adjusted each year depending on the borrower’s changing income and family size. The plan has a ceiling of 15% of the household’s monthly income. For more information, see the U.S. Department of Education.

Finally, the Public Service Loan Forgiveness Program is open for buyer clients with Direct student loans – FFEL loans are not eligible – who are:

- government employees working full-time for a federal, state or local government agency; or

- employees of a tax-exempt not-for-profit organization.

This public service employee program works jointly with the Pay As You Earn or Income-Based Repayment plans, by coupling these plans to:

- limit the borrower’s monthly payment to the applicable reduced payment amount; and

- end the repayment period at ten years, at which time the remaining loan balance is forgiven.

To qualify, a borrower has a Direct Loan and made 120 qualifying monthly payments under a repayment plan. The payments must all have been in full and on time. For more information, see the U.S. Department of Education.

An agent’s solution is counseling the first timer

All things considered, no quick fix exists for the massive and mounting burden of student debt. However, a real estate agent has a few steps they can take when confronted with a client who wishes to buy but presents issues qualifying for a mortgage due to their student debt:

- Ask the client to prepare a profit and loss statement detailing their monthly income and debt payments for your reference when discussing their DTI. [See RPI Form 209-2]

- When their DTI exceeds acceptable levels to qualify for a meaningful mortgage amount, advise on different student loan repayment plans which may lower their payments and thus lessen the percentage of DTI.

- Shift your outlook to the long-term. Suggest the prospective first time homebuyer save up for a 20% down payment and build the good credit necessary to qualify for the best available mortgage rates with minimal charges. Consider the prospect as a client who will buy in the future and provide references in the meantime.

- Make a list of current renters who are prospective homeowners but are now unable to buy due to debt. Send FARM materials regularly and check in with them every so often. Keep your name and advice fresh in their minds. When you find your list of renters becoming lengthy, you may even consider adding property management to your list of skills.

Student debt is here to stay — and it will continue to grow until governments reverse course and fund a college education. Stay ahead of the competition by branding yourself as an expert who assists homebuyers with managing student debt as a future homebuyer.

{kind=link}

Refunds on subscription apps usually feel painful, but SmartyMe refund process was actually fine. Their page covers what to do. Did it myself once after a double charge – contacted the support team, no weird hoops.

vfsdffsd

At the end of the repayment time and debt balance forgiveness, I understand the balance forgiven will be taxable . Then how will the former student be able to PAY THE TAXES! Maybe do what was done on short sales for several years and make the balance tax exempt. Most folks do NOT know about the tax implications

Two things could be done to solve this problem as follows;

– Have a 40 year loan program with 10% down.

– Allow the student loan and the home loan to be combined. For example a $100,000 student loan and a $ 500,000 home loan would combine to give a $600,000 combined loan at current 4% rate.