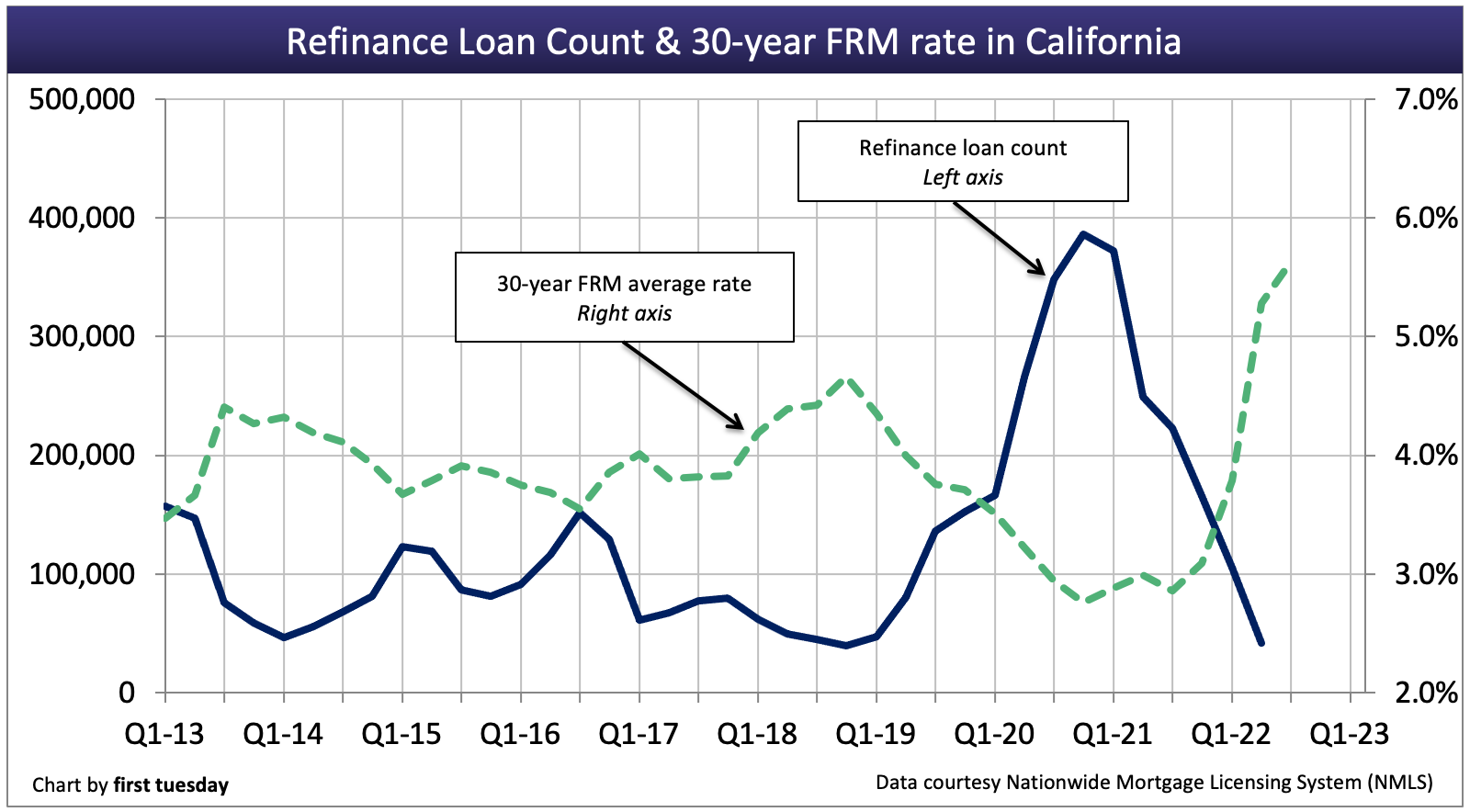

Following the record-smashing refinance volume of 2020-2021, refinancing has quickly collapsed into irrelevance.

When interest rates climb, refinancing simply makes less sense for homeowners. Conversely, when interest rates plunge — as during 2020-2021 — demand for refinances responds by rising rapidly, as expected.

Just 42,000 loans were refinanced in Q2 2022, down sharply from the 249,000 loans refinanced a year earlier. While refinance numbers are not yet available for the second half of 2022, fixed rate mortgage (FRM) interest rates have continued to climb. Therefore, expect reports to show refinance volume in the basement by year’s end.

While interest rates fluctuate on a daily basis, the overall trend for the next two decades will be up. This is reflective of the historical rate cycle, which bottomed most recently in 2012. The plunging rates of 2020-2021 were temporary aspects of the Pandemic Economy, stimulated by government intervention. Now that rates have resumed their upward course, extreme pressure will continue to fall on the refinance segment of the mortgage industry.

Mortgage loan originators and other industry professionals will need to make a quick attitude shift from relying on refinances to boost incomes during 2020-2021 to identifying more creative streams of income. This includes arranging sales of carryback notes, working with investors and real estate owned (REO) property and arranging private money loan originations.

Updated November 16, 2022. Original copy released July 2014.

Chart update 11/16/22

| Q2 2022 | Q1 2022 | Q2 2021 | |

| Refinance loan count | 42,000 | 105,500 | 249,400 |

| Refinance loan amount | $28 billion | $48 billion | $136 billion |

Average 30-year FRM rate | 5.6% | 5.3% | 3.00% |

Refinancing inflated the mortgage industry

Refinances made up just 35% of the 119,000 mortgage originations in California during Q2 2022, with purchases making up nearly all the difference. This relatively low share is down from the record-breaking 80% share achieved in 2021, when plummeting interest rates attracted a higher number of refinances.

The single largest influence on the recent drop in refinances has been the historic jump in mortgage rates, which followed record-low interest rates in 2020-2021.

2012 was the bottom of a 60-year rate cycle: 30 years of descending mortgage rates, followed by another 30 years of rising mortgage rates. Thus, the long-term outlook is one of steadily rising rates. However, the Federal Reserve (the Fed) began to drop rates in 2019 in preparation for the next recession, which officially began in February 2020. The Fed began bumping up their benchmark rate in early 2022, and the bond market reacted in kind by allowing long-term interest rates — like mortgage interest rates — to rise.

MLOs get nervous

The number of California mortgage loan originators (MLOs) have steadily risen each quarter since the first quarter (Q1) of 2012. State-licensed MLOs continue to rise, likely due to the availability of work, while federally registered MLOs have remained level since 2014. However, as rates continue to rise and mortgage originations diminish, MLOs are quickly losing work. Thus, the renewal rate for MLOs is expected to likewise decrease, along with newly licensed MLOs.

Still, more activity is being seen from end user homebuyers (those most likely to take out mortgages, as opposed to speculators who are often armed with cash).

Where’s the profit going to come from?

Lower bank earnings are expected for the next two-three decades, as banks will attempt to keep mortgage rates appealing while still maintaining a profit.

Low earnings will be further complicated by rising mortgage delinquencies. Nationally, the foreclosure moratorium and forbearance programs have kept millions of homeowners in their homes without making mortgage payments. While in forbearance, the mortgage servicer agrees to temporary halt the foreclosure process while the homeowner attempts to bring the mortgage current.

However, the foreclosure moratorium ended in July 2021, and as many exit forbearance 2022, these mortgages are fair game for lenders. A influx of forced sales are expected in 2023-2025, adding to inventory.

Related article:

Rising 90+ day mortgage delinquencies are the foreclosure shadow inventory

Getting used to lower mortgage profits

Our message to MLOs is this: lower earnings will continue over the next two decades or so, with short reprieves when interest rates decline in tandem with recessionary activity. A shift in the housing market has occurred. Reduced buyer purchasing power equals stunted home sales volume and thus prices. The refinance wave of 2020-2021 was a temporary reprieve from the pressures of the long-term rate cycle.

Still, the long-term outlook doesn’t need to be all dreary. Preparing now for reduced profits can help your mortgage business survive in the years to come. As profits per loan originated will again begin to decrease, the difference will need to be made up with a greater volume of loan originations.

Buyers desire better customer service, and many are willing to pay a higher interest rate to get that service, according to a survey by Carlisle and Gallagher Consulting Group. Gaining a word of mouth reputation for superior customer service is one way to ensure you gain the loan volume needed to survive in the coming years.

{kind=link}

Still, the long-term outlook doesn’t need to be all dreary. Preparing now for reduced profits can help your mortgage business survive in the years to come. As profits per loan originated will again begin to decrease, the difference will need to be made up with a greater volume of loan originations.