Bank earnings decreased in the first quarter (Q1) of 2014, down 7.6% from a year earlier. Lost revenue due to decreased mortgage activity was mostly to blame, according to the Federal Deposit Insurance Corporation (FDIC). Total reported net income for FDIC-insured banks and savings institutions was $37.2 billion in Q1 2014.

FDIC chairman Martin J. Gruenberg attributes the loss both to a decline in both purchase and refinance mortgages, as well as shrinking margins due to high interest rates. Indeed, the dollar amount of mortgage originations and refinances for one-to-four family residential homes was a whopping 71% lower than in Q1 2013.

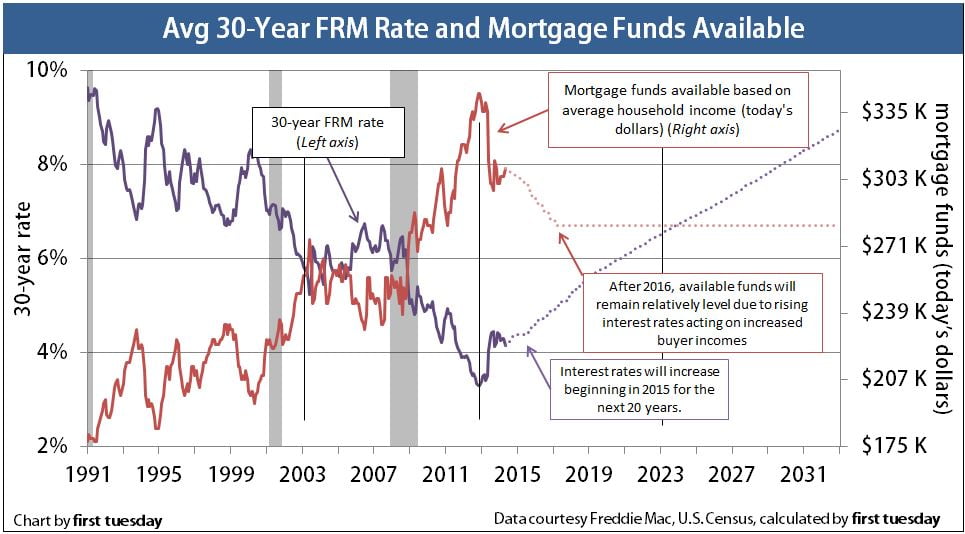

Our message to lenders: get used to it. Lower profit margins are here to stay for the next 20-30 years as banks struggle to keep mortgage rates enticing to homebuyers while maintaining their margins. That’s because we’re entering the upswing of a 60-year rate cycle: roughly 30 years of falling interest rates, followed by 30 years of rising interest rates. We hit the bottom of the cycle at the end of 2012, followed by a premature rate spike in mid-2013, seen in this chart:

Together with outrageous home prices in the aftermath of 2013’s speculator free-for-all, today’s higher mortgage rates equal reduced buyer purchasing power.

The good news is that mortgage rates aren’t expected to increase for several more months. Mortgage rates will rise when members of the bond market push long-term rates higher in anticipation of the Federal Reserve (the Fed) raising rates in the latter half of 2015. The Fed’s hope is the U.S. economy will be fully recovered and picking up steam by the time they act to raise rates in 2015. Thus, more financially able homebuyers will be better equipped to deal with higher rates and bank profits won’t feel the blow too much. However, once mortgage rates begin to increase, they will continue to rise for two-three decades.

Let your buyer clients know: although yesterday’s rates were lower, those low rates are not returning any time soon. If they are able to qualify at today’s rates, they ought to consider buying before those rates increase next year.

{kind=link}