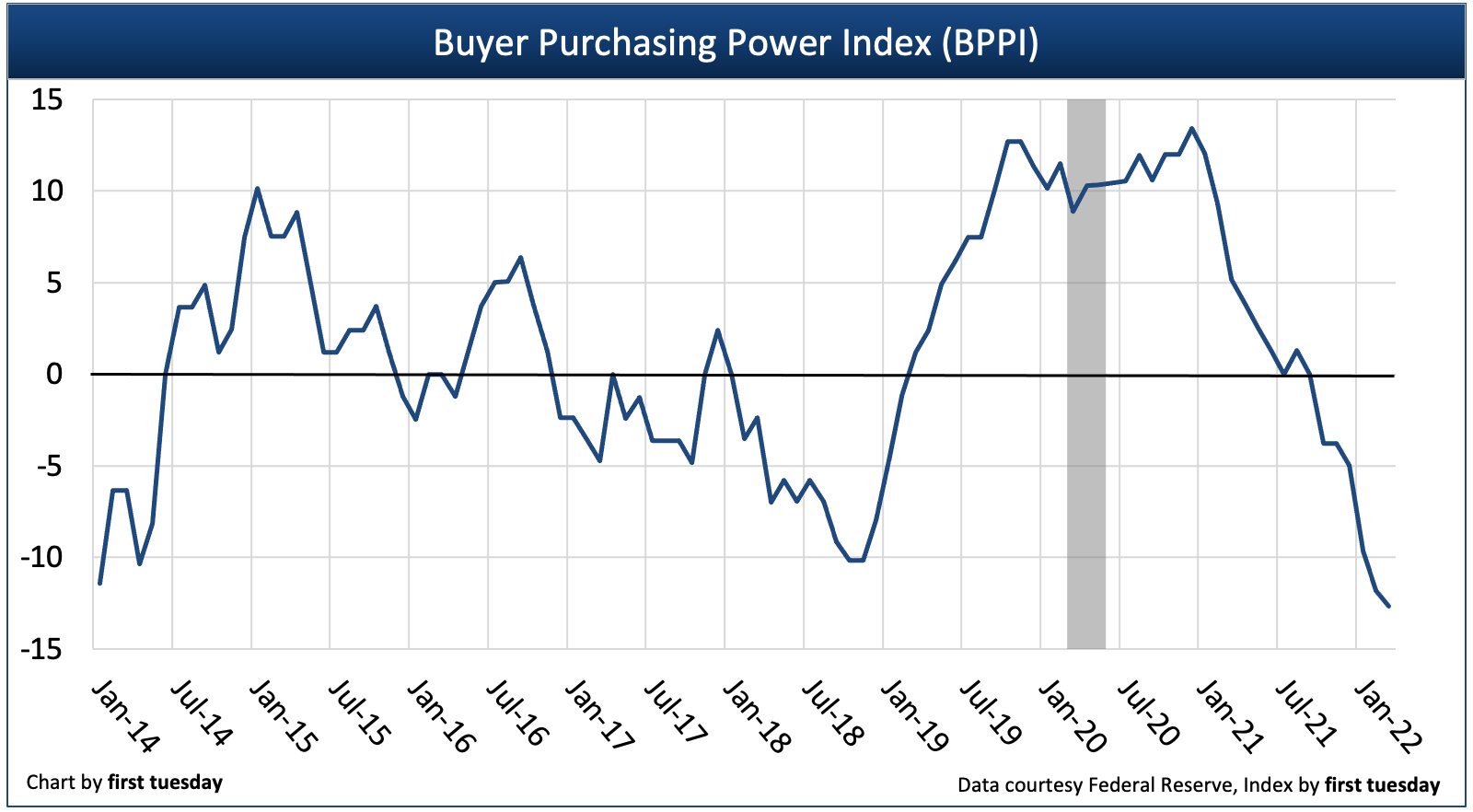

The California Buyer Purchasing Power Index (BPPI) figure declined to -12.7 in March 2022. This figure tells us a homebuyer with the same income is able to borrow 12.7% less mortgage money than a year ago when mortgage interest rates were still near historic lows. Q1 2022’s negative BPPI figure reflects a quickly worsening situation for homebuyers reliant on mortgage financing, as the BPPI had previously been in the positive during 2019-2021 due to consistently lower mortgage interest rates.

Going forward, the BPPI will further decline as interest rates continue to rise, in what has been the swiftest turnaround for interest rates experienced since the 1990s. Already, the BPPI has stumbled even further into negative territory at the time of this reporting in April 2022.

Chart update 04/19/22

| Q1 2022 | Q4 2021 | Q1 2021 | |

| Buyer Purchasing Power Index (BPPI) | -12.7 | -5.0 | +5.2 |

As the BPPI declines, so goes support for home prices. In today’s rising mortgage interest rate environment, both the BPPI and homebuyer participation in the home sales market are adversely affected.

As of January 2022, average California home prices are 19%-to-22% higher than one year earlier. However, 2022’s rapid mortgage rate increases are beginning to interfere with home prices, as market momentum is swiftly cooling. Since homebuyers qualify for a maximum mortgage amount based on their incomes, any rise in mortgage rates instantly cuts the amount they can borrow. Thus, the price they pay for a home is reduced.

Lacking the support of falling interest rates, additional stimulus or income boosts, home prices are expected to fall back in 2022. Home prices will be further checked by the additional inventory anticipated to arrive in 2022 following the 2021 expiration of the foreclosure moratorium.

For some background, interest rates descended to historic lows in 2020 due to efforts to stimulate lending despite job losses and tightening access to credit. Beginning in Q1 2020, the Federal Reserve (the Fed) dropped their benchmark interest rate to zero and began purchasing mortgage-backed bonds (MBBs), fulfilling their role as lender of last resort to ensure mortgage originations continued.

In March 2022, the Fed finally bumped up their benchmark rate and announced it will soon begin selling off its MBB holdings.

Interest rates will continue to rise as the Fed further increases its benchmark rate in 2022-2023 and gradually releases more MBBs into the market. In anticipation of the Fed’s bond taper, investor activity began to push rates slightly higher in Q3 and Q4 2021, with a rate surge arriving in Q1 2022.

firsttuesday expects mortgage interest rates to continue to increase in the months ahead, causing the BPPI figure to remain negative throughout 2022.

The long-term outlook for the BPPI is a decades’ long period of descent as mortgage rates continue to rise with the economic recovery, likely to gain strength around 2024. Thus, sellers can expect downward pressure on home prices. Without the support of a full jobs recovery, home prices will remain tenuous in 2022, likely to fall heading into 2023.

About the BPPI

The Buyer Purchasing Power Index (BPPI) is calculated using the average 30-year fixed rate mortgage (FRM) rate from Freddie Mac (Western region) and the median income in California.

A positive index number means buyers can borrow more money this year than one year earlier.

A negative index figure translates to a reduced amount of mortgage funds available.

An index of zero means there was no year-over-year change in the amount a buyer can borrow with the same income. At a BPPI of zero, homebuyers cannot purchase at higher prices than one year before unless they resort to adjustable rate mortgages (ARMs) to extend their borrowing reach or greater down payment amounts.

As long-term BPPI trend declines, the capacity of buyers to borrow purchase-assist funds is reduced. In turn, buyers needing purchase-assist financing on average can only pay a lesser price for a home. To keep the inventory of homes for sale moving at the same pace, sellers will need to lower prices to accommodate buyer purchasing power or pull their properties off the market.

—

first tuesday journal online is a real estate news source. It provides analyses and forecasts for the California real estate market, and has done so since 1978.

{kind=link}