This form is used by an agent when preparing a marketing package for an income property they listed for sale or conducting a due diligence investigation of the property for a buyer, to gather rent and expense data for calculating the property’s net operating income (NOI) and estimating its annual reportable income or loss.

Operating data disclosed to buyers

A broker and their agents need to advise a prospective buyer or tenant of any material facts that may affect the value or desirability of the purchased or rented property. A broker marketing property as an income-producing investment also owes a duty to the buyer to research and disclose whether the property produces adequate income to meet the buyer’s investment objectives.

An annual property operating data sheet (APOD) is a worksheet used when gathering income and expenses on the operation of an income producing property, to analyze its suitability for investment. [See RPI Form 352]

Operating data is gathered and entered on the APOD by the seller and the seller’s agent. The APOD provides information about the property’s fundamentals and is handed to prospective buyers or their agents.

An income-producing property’s operating data is the glue attaching the commencement to the conclusion of a transaction. When the data is deficient or defective in its content, the adhesiveness of the data is lost. The transaction will not close without a price adjustment.

By design, the APOD is intended to induce prospective buyers to rely on its content to decide just what price to offer to buy the property. Thus, with the presentation of an APOD to a prospective buyer or their agent, negotiations have begun.

When negotiations produce a match, a prospective buyer enters into a purchase agreement with the seller. The conclusive act by the buyer and the buyer’s agent is the completion of their due diligence investigation to verify the accuracy and future relevance of the income data contained in the APOD.

To verify the data, the buyer’s agent reviews the seller’s records for operating expenses, rent rolls, leases and tenant estoppel certificates. When the estoppel certificates are substantially the same as the data contained in the APOD and the leases, and the expenses are verified by the buyer’s agent, the transaction will most likely close.

Property information which needs to be separately disclosed to a prospective buyer so they may determine the property’s worth includes recent “spikes” in expense items, such as:

- utilities;

- evictions necessitated by delinquencies;

- security re-evaluations needed due to incidents of crime on the premises;

- loss of a local industry which employs a significant percentage of area tenants;

- assumable or locked-in financing;

- rent control adjustments; and

- mortgage commitments.

The APOD contents

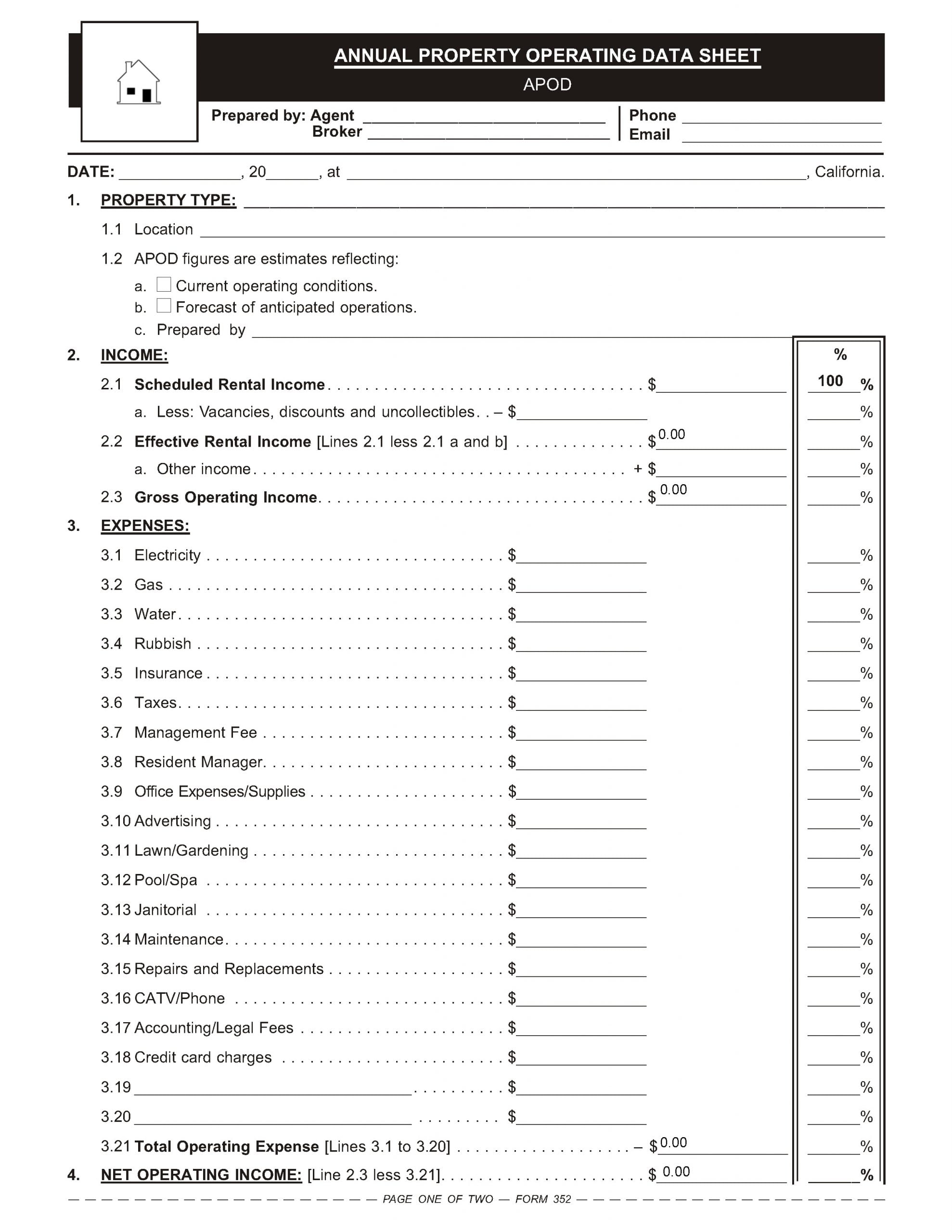

A buyer’s agent or broker uses the Annual Property Operating Data Sheet (APOD) published by RPI when gathering income and expenses on the operation of an income-producing property. It allows the buyer to analyze the property’s suitability for investment purposes. [See RPI Form 352]

An APOD, prepared by a seller’s agent and handed to a prospective buyer, provides operating information on the property, including:

- the estimated net operating income (NOI), which is the net revenue generated by an income producing property as the return on capital, calculated as the sum of a property’s gross operating income minus the property’s operating expenses. The NOI sets the price to be paid and the mortgage amounts which may be serviced by the income generated by the property;

- the spendable income, for providing a cash-flow cushion reflected by the amount of the NOI remaining after servicing the mortgage financing (including information on mortgage balances, monthly payments, interest rates and any due dates); and

- the income tax consequences the prospective buyer is likely to experience during the first year of ownership due to allowable deductions of interest on trust deed mortgages and IRS depreciation schedules.

In the comment’s section of the APOD form, the seller’s agent enters local trends and factors known to the seller’s agent which are not necessarily readily observable or known to a prospective buyer or the buyer’s agent when viewing the property, or discoverable when reviewing the marketing package.

Expenses, as a percentage of scheduled income, are calculated on the APOD in the center column. Percentages are obtained by dividing each expense item by the scheduled income (100%). [See RPI Form 352]

The percentage calculated for each operating expense alerts the prospective buyer and their agent to data which varies from a range typically experienced by the type of income property involved.

Once the seller’s agent delivers the APOD to the prospective buyer and their agent, the special agency duty owed the buyer by a buyer’s agent is to review the skeletal property information received from the seller and the seller’s agent and advise the buyer on additional inquiries or investigations needed to understand and appreciate the ramifications of the disclosures.

Analyzing the APOD

An agent uses the Annual Property Operating Data Sheet (APOD) published by RPI when preparing a marketing package for an income property they listed for sale or conducting a due diligence investigation of the property for a buyer. The form allows the agent to gather rent and expense data for calculating the property’s net operating income (NOI) and estimating its annual reportable income or loss. [See RPI Form 352]

The APOD contains information regarding:

- the property type, including whether APOD figures reflect current operating conditions or are a forecast of anticipated operations [See RPI Form 352 §1];

- income, including the scheduled rental income less vacancies and discounts, effective rental income and gross operating income [See RPI Form 352 §2];

- expenses, including:

- electricity;

- gas;

- water;

- trash;

- insurance;

- taxes;

- management fees;

- resident manager salary;

- office expenses/supplies;

- advertising;

- lawn/gardening;

- pool/spa;

- janitorial;

- maintenance;

- repairs and replacements;

- phone;

- accounting/legal fees; and

- credit card charges [See RPI Form 352 §3];

- net operating income (NOI), calculated as the gross operating income less total operating expenses [See RPI Form 352 §4];

- spendable income, calculated as the NOI less total annual debts [See RPI Form 352 §5];

- property information, including the:

- price;

- loan amounts;

- owner’s equity;

- current vacancy rate;

- depreciation as indicated by an assessor of:

- improvements;

- land; and

- personal property; and

- required property disclosures [See RPI Form 352 §6]; and

- reportable income/loss as an annual projection for the buyer to fill out. [See RPI Form 352 §7]

Form navigation page published 08-2021. Updated 01-2026.

Form last revised 2011.

Form-of-the-Week: The Annual Property Operating Data Sheet (APOD) and Tenant’s Property Expense Profile — Forms 352 and 562

Form-of-the-Week: Annual Property Operating Data Sheet (APOD) and Tenant Estoppel Certificate (TEC) — Forms 352 and 598

Article: Material facts and your opinions – liability exposure minimized

Article: Transparent solicitation of offers via a marketing package

Article: Determining creditworthiness in seller financing

Blog: Tiny homes join ADUs in the housing shortage fight

Brokerage Reminder: The seller’s broker’s due diligence

Brokerage Reminder: Carryback financing – the creditworthy buyer and mandated disclosures

Word-of-the-Week: Fiduciary duty