Operating expenses disclosed to tenants

Prospective tenants and buyers retain brokers to inform them of relevant conditions surrounding a property considered for acquisition. Brokers and their agents are the presumed experts, licensed and trained in the issues affecting pricing and users of property. Relevant information includes the costs of occupying and ongoing operations within a space, collectively called operating expenses.

As for a landlord and their leasing agent, their role in marketing space is limited to:

- disclosing facts about the property that adversely affect the value and use of the property; and

- avoiding misleading disclosures.

The duty the landlord’s broker owes tenants does not require them to advise tenants about any adverse consequences the disclosed facts might have on them. Advice on the consequences of the facts disclosed is the duty owed to the tenant by the tenant’s broker. Here, the landlord’s broker owes the tenant only a limited general duty of honesty and fair dealing, whereas the tenant’s broker owes the tenant a greater fiduciary duty.

When the tenant is represented by an agent, they receive advice on a property before leasing and are better prepared to make informed decisions when selecting among all available properties.

The role and burden of ascertaining the consequences of a property’s essential facts falls on the tenant’s leasing agent.

The factual information and assistance which a landlord’s broker may offer prospective tenants falls into one of three general categories:

- The property’s physical aspects, including square footage, shipping facilities, utilities, HVAC units, tenant improvements, sprinkler system, condition of the structure, soil, geologic hazards, toxic or noise pollution, parking, etc.;

- The conditions of occupancy affecting the use and enjoyment of the property, i.e., facts available on request from title companies (CC&Rs, trust deeds and vesting), planning departments (uses permitted), redevelopment agencies, business tax rates, police and fire department response times, security, natural hazards and conditions of the neighborhood surrounding the location; and

- The cost of operating the leased premises when put to the expected use.

A property’s operating costs include business taxes local agencies charge a tenant for conducting business in their jurisdiction. Taxes weigh on the selection of available space, as does access to highways and the client’s market if the business is conducted in person. Business taxes vary greatly from city to city, as do police response times and criminal activity.

A property’s operating expenses are part of its signature, distinguishing it from other available properties. Data on a property’s operating costs are gathered and set forth on the property expense profile which is handed to prospective tenants. These profiles are used by leasing agents to induce tenants to rent their landlord-client’s space rather than other comparable space. [See RPI e-book Income Property Brokerage Chapter 16; see RPI Form 562]

Property-related expenditures incurred by a tenant of a specific property during the leasing period are classified as:

- recurring operating expenses;

- nonrecurring deposits or charges; or

- rent and payments on mortgages secured by the tenant’s leasehold.

Comparative cost analysis

Tenants, their leasing agents and property managers compare the costs a tenant will incur to occupy and operate in a particular space against the costs to operate in another available space, a type of comparative cost analysis.

The tenant’s comparative cost analysis is even more relevant to negotiations during periods of economic slowdown. Overbuilding or a decline in the number of commercial tenants increases vacancy levels. When this occurs, sound economics will dictate a reduced rental rate until demand for space fills up the present supply of available space and rental rates rise again.

When tenants search for space without the pressure of high occupancy levels and the attendant scarcity of space, they are more likely to compare properties. They are also more likely to select a property based on operating costs or the cost of tenant improvements (TIs), rather than rent alone.

Landlords leasing their properties for below-market rents need to be queried for information and history on the operating costs the tenant will incur in addition to the rent. Below-market rent raises suspicions of property obsolescence due to aging and loss of function, or excessive operating costs such as utility charges, local taxes, security needs, use requirements, neighborhood issues and crime.

Without knowledge of property operating costs, the prospective tenant is left to speculate about the total costs (in addition to base rent) of leasing the property. For the tenant, this is a financially unsound starting place for negotiating a lease.

At a bare minimum, the tenant’s leasing agent is duty bound to bring known and readily available data to the tenant’s attention. The tenant may then obtain additional information during negotiations or by requiring the information from the landlord through a contingency provision before taking occupancy.

At their best, the tenant’s leasing agent not only advises, but also investigates and reports on the data they collect. They also provide analysis and recommendations to the tenant they represent. Landlords’ leasing agents are generally unhappy about these inquiries, preferring reduced transparency and instant uninformed action – an asymmetry of information.

The landlord either knows or can easily obtain from their property manager or current tenant the actual costs of operating their property for the intended use. Thus, property operating data is readily available to the landlord.

When the landlord or the landlord’s broker refuses to supply the data to the tenant, the tenant’s broker may:

- investigate the expenses the current and prior tenants have experienced;

- make any offer to lease contingent on getting and reviewing the operating data; or

- use a letter of intent (LOI) to provide a method of getting information. [See RPI Form 185]

Armed with the knowledge of the total costs, the tenant’s broker may comfortably disclose the operating expenses to their client.

Best practices when disclosing operating costs include:

- the preparation of a property expense profile for each available unit, prepared by the landlord or property manager and signed by the landlord [See RPI Form 562]; and

- a comparison by the tenant and the tenant’s broker of the economic cost of rent, and other operating expenses for one space versus the parallel costs incurred in other qualifying spaces.

With documentation and a comparative analysis of rent and operating costs complete, the tenant and the tenant’s broker can intelligently negotiate the best lease arrangements available for the tenant in the local market.

Occasionally, a landlord may be tightlipped about the operating data due to various arrangements with numerous tenants. In this case, the landlord may insist on (or be offered by the tenant) a confidentiality agreement before releasing any data to the prospective tenant.

Tenants who forego representation by an agent lose the benefit of a comparative analysis. Critically, they also incur significantly greater risk since they miss out on the experience and advice of a licensee retained to represent their best interests.

The contents of the Property Expense Profile for tenants

An owner and their leasing agent use the Tenant’s Property Expense Profile published by RPI (Realty Publications, Inc.) when preparing a marketing package for the lease of a property. It discloses the property’s operating costs to the prospective tenant, allowing them to review the monthly property operating costs and deposits they will likely incur on taking possession of the property. [See RPI Form 562]

The Tenant’s Property Expense Profile contains:

- the date, address of the subject property and name of the prospective tenant [See RPI Form 562];

- a description of the property type and its location, as well as a checklist stating whether the estimates reflect current expenses of occupancy or are a forecast of anticipated expenses of occupancy [See RPI Form 562 §1];

- monthly operating expenses are entered and totaled, then added to the monthly lease payment to arrive at a total monthly expense figure [See RPI Form 562 §2];

- deposits are entered and totaled, with a dollar amount allocated to each individual category, such as security, electricity, water, sewage, gas and phone deposits, as well as a space to list other types of deposits not listed, to arrive at a total deposit amount [See RPI Form 562 §3]; and

- the landlord’s signature, the prospective tenant’s signature and the information of the tenant’s broker and agent. [See RPI Form 562]

Operating data disclosed to buyers

A broker and their agents need to advise a prospective buyer or tenant of any material facts that may affect the value or desirability of the purchased or rented property. A broker marketing property as an income-producing investment also owes a duty to the buyer to research and disclose whether the property produces adequate income to meet the buyer’s investment objectives.

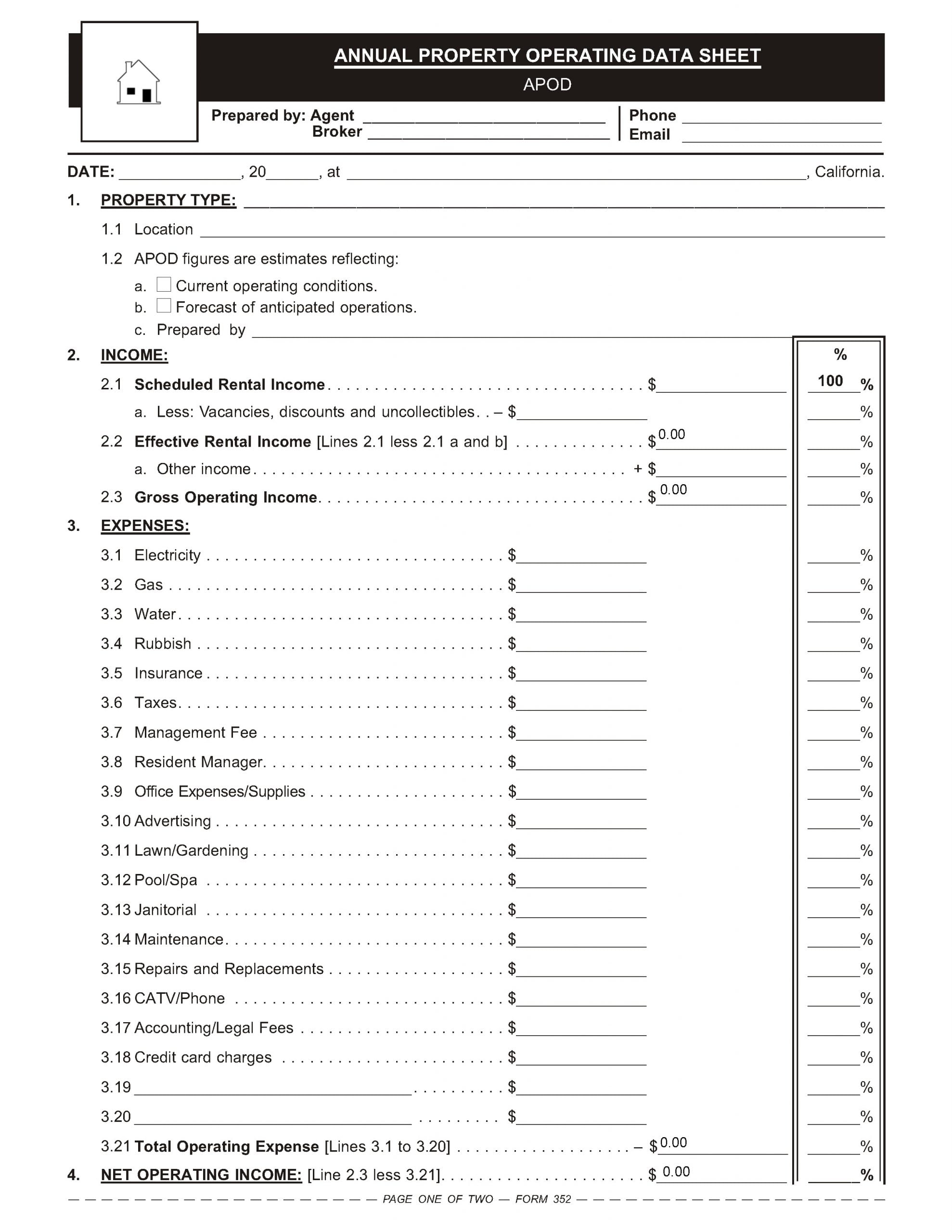

An annual property operating data sheet (APOD) is a worksheet used when gathering income and expenses on the operation of an income producing property, to analyze its suitability for investment. [See RPI Form 352]

Operating data is gathered and entered on the APOD by the seller and the seller’s agent. The APOD provides information about the property’s fundamentals and is handed to prospective buyers or their agents.

An income-producing property’s operating data is the glue attaching the commencement to the conclusion of a transaction. When the data is deficient or defective in its content, the adhesiveness of the data is lost. The transaction will not close without a price adjustment.

By design, the APOD is intended to induce prospective buyers to rely on its content to decide just what price to offer to buy the property. Thus, with the presentation of an APOD to a prospective buyer or their agent, negotiations have begun.

When negotiations produce a match, a prospective buyer enters into a purchase agreement with the seller. The conclusive act by the buyer and the buyer’s agent is the completion of their due diligence investigation to verify the accuracy and future relevance of the income data contained in the APOD.

To verify the data, the buyer’s agent reviews the seller’s records for operating expenses, rent rolls, leases and tenant estoppel certificates. When the estoppel certificates are substantially the same as the data contained in the APOD and the leases, and the expenses are verified by the buyer’s agent, the transaction will most likely close.

Property information which needs to be separately disclosed to a prospective buyer so they may determine the property’s worth includes recent “spikes” in expense items, such as:

- utilities;

- evictions necessitated by delinquencies;

- security re-evaluations needed due to incidents of crime on the premises;

- loss of a local industry which employs a significant percentage of area tenants;

- assumable or locked-in financing;

- rent control adjustments; and

- mortgage commitments.

Related Video: Estimates as Projections or Forecasts

Click here for more information on this topic.

The APOD contents

A buyer’s agent or broker uses the Annual Property Operating Data Sheet (APOD) published by RPI when gathering income and expenses on the operation of an income-producing property. It allows the buyer to analyze the property’s suitability for investment purposes. [See RPI e-book Due Diligence and Disclosures Chapter 35; see RPI Form 352]

An APOD, prepared by a seller’s agent and handed to a prospective buyer, provides operating information on the property, including:

- the estimated net operating income (NOI), which is the net revenue generated by an income producing property as the return on capital, calculated as the sum of a property’s gross operating income minus the property’s operating expenses. The NOI sets the price to be paid and the mortgage amounts which may be serviced by the income generated by the property;

- the spendable income, for providing a cash-flow cushion reflected by the amount of the NOI remaining after servicing the mortgage financing (including information on mortgage balances, monthly payments, interest rates and any due dates); and

- the income tax consequences the prospective buyer is likely to experience during the first year of ownership due to allowable deductions of interest on trust deed mortgages and IRS depreciation schedules. [See RPI e-book Tax Benefits of Ownership Chapter 2]

In the comment’s section of the APOD form, the seller’s agent enters local trends and factors known to the seller’s agent which are not necessarily readily observable or known to a prospective buyer or the buyer’s agent when viewing the property, or discoverable when reviewing the marketing package.

Expenses, as a percentage of scheduled income, are calculated on the APOD in the center column. Percentages are obtained by dividing each expense item by the scheduled income (100%). [See RPI Form 352]

The percentage calculated for each operating expense alerts the prospective buyer and their agent to data which varies from a range typically experienced by the type of income property involved.

Once the seller’s agent delivers the APOD to the prospective buyer and their agent, the special agency duty owed the buyer by a buyer’s agent is to review the skeletal property information received from the seller and the seller’s agent and advise the buyer on additional inquiries or investigations needed to understand and appreciate the ramifications of the disclosures.

{kind=link}