Protection for buyers and lenders

A real estate broker represents an owner of income-producing property who wants to sell or refinance their tenant-occupied property. The broker prepares a marketing package to be handed to prospective buyers or lenders to induce them to enter into a transaction with the owner. It will include an annual property operating data sheet (APOD). [See RPI Form 352]

To prepare the APOD, The broker requests and receives a Profit and Loss statement from the owner setting out rents and expenses the owner actually incurred operating the property.

Also for a due diligence

An APOD is completed for two situations: The actual current income and expenses, and the potential or anticipated income and expenses determined in the broker’s due diligence CMA review. The prepared APOD will provide buyers or lenders with an accurate summary of financial information on the operating income and expenses the property is likely to generate. [See RPI e-book Real Estate Property Management, Chapter 61]

Though reliable when competently prepared, buyers and lenders who rely on APOD figures need to corroborate the income and expense numbers and other leasing arrangements prior to closing.

Related Video: Estimates as Projections or Forecasts

Click here for more information on an agent’s use of estimates and opinions.

The objectives of a tenant estoppel certificate

When handling the sale or refinance of a tenant-occupied property, closing needs to be conditioned on the buyer or lender’s receipt and further approval of Tenant Estoppel Certificates (TEC), one signed and returned, or not, by each tenant occupying the property. [See RPI Form 598]

The TEC summarizes the terms of the financial and possessory provisions in each tenant’s lease agreement, and whether the landlord and tenant have fully performed their obligations. [See RPI Form 598]

The TEC’s objective is to confirm the current status of:

- rent schedules;

- security deposits;

- possessory and acquisition rights; and

- the responsibility for maintenance and other operating or carrying costs.

Thus, the TEC will reveal any option or first refusal rights held by the tenant to:

- extend or renew the lease;

- buy the property;

- lease other or additional space; or

- cancel the lease on payment of a fee.

Critically, the lease agreement needs to contain a TEC provision before the owner may require a tenant to sign and return a TEC to confirm the leasing arrangements. [See RPI Form 552 §18]

The TEC provision calls for the tenant to:

- sign and return a TEC which has been filled out and sent to them within a specific period of time after its receipt; or

- waive their right to contest its contents when the tenant fails to sign and return the TEC submitted for their signature.

Tenant response on receipt of a TEC

A TEC includes a statement indicating a buyer or lender will rely on the information provided by the TEC when deciding to lend or purchase. Thus, the representations made in the TEC are to be factual, not just guesswork. [See RPI Form 598 §12]

In the TEC, the tenant acknowledges the accuracy of its contents by either:

- signing and returning it; or

- failing to respond, which waives the right to contest the accuracy of its contents.

Either way, a buyer or lender may rely on the TEC’s content as complete and correct statements on the terms and conditions of the lease. [Calif. Evidence Code §623]

The fully processed TEC prevents any later tenant claims made in a dispute with the buyer or lender that its terms are in conflict with the contents of the lease agreement.

A buyer or lender asserts their right to rely on and enforce the terms stated in the TEC by presenting the tenant’s TEC as a defense to bar contrary claims made by the tenant, called estoppel. Thus, the tenant is estopped from denying the truth of the information in the TEC or later claiming conflicting rights.

Related article:

May a landlord evict a tenant under the Ellis Act after unknowingly altering the terms of the lease?

TEC substantiates prior representations

A completed APOD form received by a buyer presents an accounting summary of a property’s income and expenses. Thus, it represents the present income flow and operating expenses a prospective buyer may reasonably expect the income-producing property to generate in the immediate future. [See RPI Form 352]

To verify the data, the buyer’s agent reviews the seller’s records for operating expenses, rent rolls, leases and TECs. When the estoppel certificates are substantially the same as the data contained in the APOD and the leases, and the expenses are verified, the transaction will most likely close. [See RPI e-book Real Estate Practice, Chapter 35]

Prior to closing, the buyer needs to:

- review and analyze each lease agreement the owner has entered into with the tenants;

- compare the results of an analysis of rent and maintenance provisions in the lease agreements to the figures in the APOD received before the offer was submitted; and

- confirm the rent schedules, possessory rights, maintenance obligations and expiration of the leases by serving conforming TECs on the tenants and reviewing their responses.

Analyzing the Tenant Estoppel Certificate

An escrow officer or owner’s broker uses the Tenant Estoppel Certificate published by Realty Publications, Inc. (RPI) when handling the closing of a sale or refinance of a tenant-occupied property which is contingent on confirmation of rents, deposits and other leasing arrangements between the tenant and owner. The form allows the broker to provide the buyer or lender with a summary of the financial and possessory terms of the tenant’s lease agreement and whether the owner and tenant have fully performed their obligations. [See RPI Form 598]

The Tenant Estoppel Certificate verifies:

- whether possession is held under a lease or rental agreement [See RPI Form 598 §1];

- any modifications to the rental or lease agreement [See RPI Form 598 §2];

- whether the tenant has assigned or sublet the premises [See RPI Form 598 §3];

- the term of the lease [See RPI Form 598 §4];

- the current monthly amount of rent [See RPI Form 598 §5];

- the amount of the security deposit [See RPI Form 598 §6];

- personal property owned by the landlord which the tenant is in possession of [See RPI Form 598 §7];

- any improvements the tenant needs to or can remove on vacating the premises [See RPI Form 598 §8];

- whether the landlord or tenant is in breach of the lease or rental agreement [See RPI Form 598 §9];

- whether the tenant holds any options or right of first refusal to buy the real estate [See RPI Form 598 §10]; and

- whether the tenant has caused a lien or encumbrance to attach to their leasehold interest in the property. [See RPI Form 598 §11]

Related article:

Analyzing the APOD

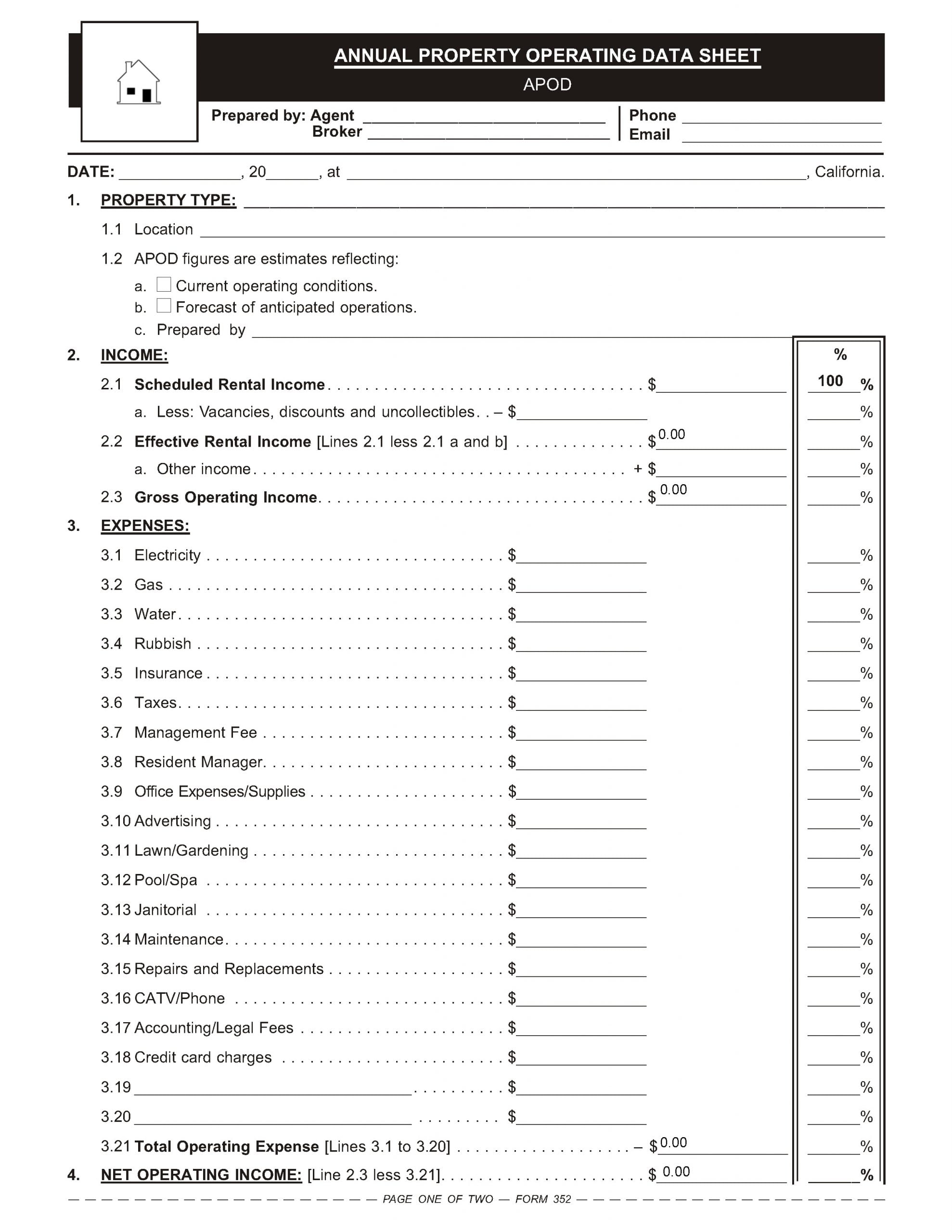

An agent uses the Annual Property Operating Data Sheet (APOD) published by RPI when preparing a marketing package for an income property they listed for sale or conducting a due diligence investigation of the property for a buyer. The form allows the agent to gather rent and expense data for calculating the property’s net operating income (NOI) and estimating its annual reportable income or loss. [See RPI Form 352]

The APOD contains information regarding:

- the property type, including whether APOD figures reflect current operating conditions or are a forecast of anticipated operations [See RPI Form 352 §1];

- income, including the scheduled rental income less vacancies and discounts, effective rental income and gross operating income [See RPI Form 352 §2];

- expenses, including:

- electricity;

- gas;

- water;

- trash;

- insurance;

- taxes;

- management fees;

- resident manager salary;

- office expenses/supplies;

- advertising;

- lawn/gardening;

- pool/spa;

- janitorial;

- maintenance;

- repairs and replacements;

- phone;

- accounting/legal fees; and

- credit card charges [See RPI Form 352 §3];

- net operating income (NOI), calculated as the gross operating income less total operating expenses [See RPI Form 352 §4];

- spendable income, calculated as the NOI less total annual debts [See RPI Form 352 §5];

- property information, including the:

- price;

- loan amounts;

- owner’s equity;

- current vacancy rate;

- depreciation as indicated by an assessor of:

- improvements;

- land; and

- personal property; and

- required property disclosures [See RPI Form 352 §6]; and

- reportable income/loss as an annual projection for the buyer to fill out. [See RPI Form 352 §7]

Related article:

Want to learn more about selling, refinancing or managing income properties? Click an image below to download the RPI book cited in this article.

{kind=link}