This form is used by a buyer broker when an absentee-owner/investor will purchase an interest in an owner-occupied one-to-four unit residential property in foreclosure, to prepare an offer containing all the terms, conditions and disclosures required of an equity purchase transaction.

Equity purchase transactions

An equity purchase (EP) transaction occurs when the owner-occupant of a one-to-four unit residential property in foreclosure conveys the property to a buyer who acquires it for rental, investment or dealer purposes. The buyer is referred to as an EP investor.

When the buyer acquires the property for use as their personal residence, an EP transaction does not occur, and EP rules do not apply.

Equity purchase statutes apply to all EP investors regardless of the number of EP transactions the investor completes, or whether the investor is in the business of buying homes in foreclosure. [Segura v. McBride (1992) 5 CA4th 1028]

The EP investor and all agents involved in the transaction use a written agreement containing statutory EP notices. Failure to use the correct forms subjects the EP investor and their agents to liability for all losses incurred by the seller-in-foreclosure, plush significant penalties. [Segura, supra]

Editor’s note – The Equity Purchase Agreement published by Realty Publications, Inc. (RPI) complies with all statutory requirements and properly sets forth the right of the seller-in-foreclosure to cancel. [See RPI Form 156]

Cancellation may occur within five business days

After entering into an agreement to sell their principal residence that is in foreclosure, the seller-in-foreclosure has a five-business-day right to cancel the agreement. This period commences on acceptance of an EP agreement containing the notice of the seller’s cancellation rights. During this time period, the seller is permitted to cancel the sale, with or without cause.

The seller’s cancellation period expires at:

- Midnight (12:00 a.m.) of the fifth business day following the day the seller accepts an EP agreement; or

- 8:00 a.m. of the day scheduled for the trustee’s sale, whichever occurs first. [Calif. Civil Code 1695-4(a)]

A business day is any day except Sunday and the following federal holidays:

- New Year’s Day;

- Washington’s Birthday;

- Memorial Day;

- Independence Day;

- Labor Day;

- Columbus Day;

- Veterans’ Day;

- Thanksgiving Day; and

- Christmas Day.

When the EP investor acquires title and transfers or encumbers the property before the cancellation period expires after notice, the EP investor is further subject to:

- a statutory penalty of three times the amount of the seller’s monetary losses; or

- a minimum $2,500 civil penalty. [CC 1695.7]

An EP investor who violates the five-day cancellation period or takes unconscionable advantage of the seller-in-foreclosure is subject to imprisonment and a fine no greater than $25,000 or both for each violation. [CC §1695.8]

“Unconscionable advantage” includes the engagement in any practice which operates as a fraud or deceit upon the seller-in-foreclosure.

Analyzing the EP agreement

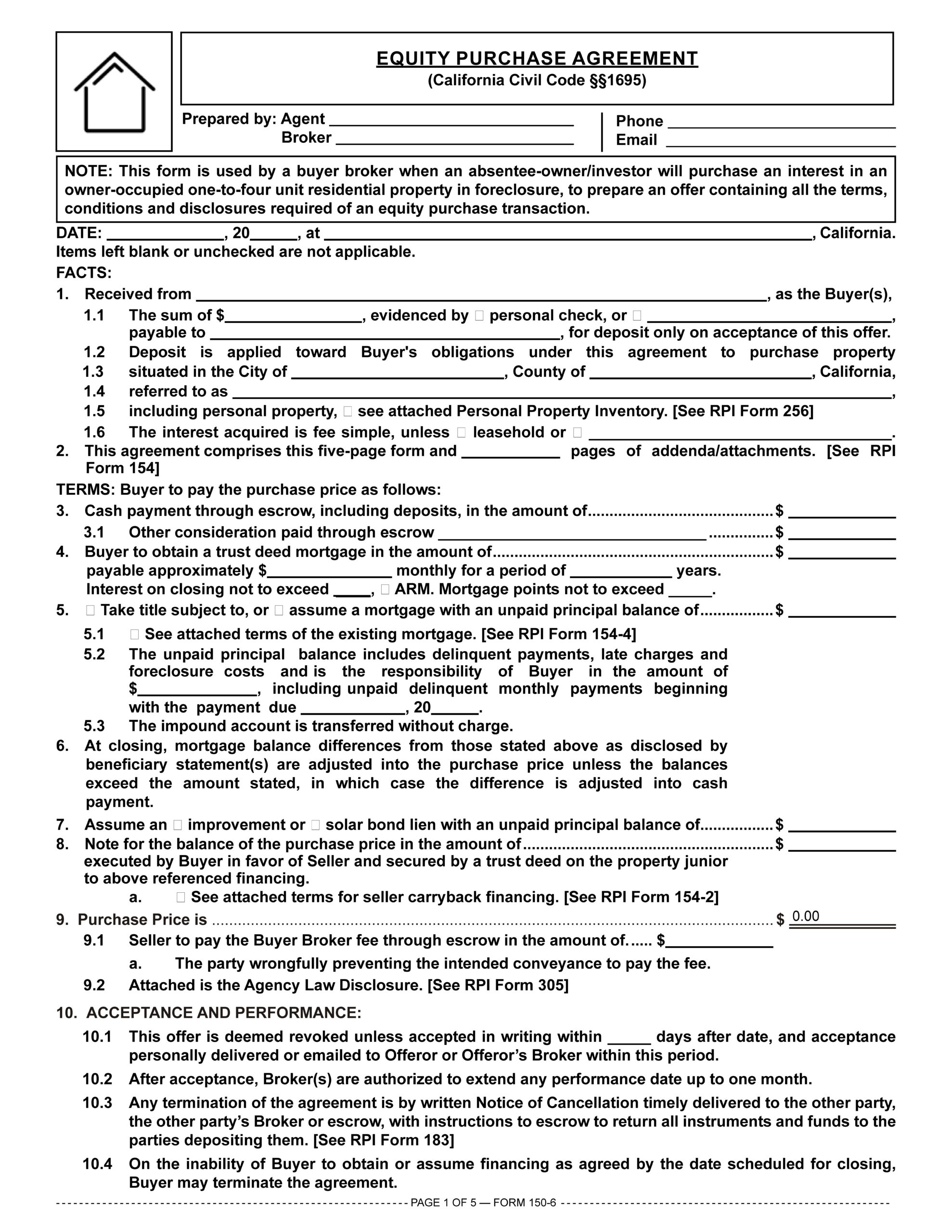

The equity purchase (EP) agreement is used to prepare a written offer to be submitted by an investor or their agent to purchase a one-to-four unit residential property in foreclosure which is occupied by the seller-in-foreclosure as their principal residence. [See RPI Form 156]

The terms for payment of the price are structured to include a lump sum amount of cash to be paid to the seller for their equity in the property. Thus, all adjustments, prorations, credits and offsets are formulated to deliver to the seller this lump sum amount unchanged since it is based on the seller’s representations of outstanding sums owed on all encumbrances affecting title to the property.

Each section in the Equity Purchase Agreement has a separate purpose and need for enforcement. The sections include:

- Identification: The date of preparation, the real estate and any personal property to be purchased, and the number of pages comprising the entire agreement, including addenda, are set forth in Sections 1 and 2.

- Price and terms of payment: All the typical variations for payment of the price are set out in Sections 3 through 10 as a “checklist of provisions.” The EP investor or their agent selects the terms of purchase by checking boxes and filling blanks in the desired provisions. While the subject matter of the various provisions is typical, the terms each contains are not. All financial aspects are biased in favor of the investor, such as prorates and adjustments, since EP transactions are structured as the payment of a lump sum for the conveyance.

- Acceptance and performance: Aspects of the formation of a contract, excuses for nonperformance and termination of the agreement are provided for in Section 11, such as the time period for acceptance of the offer, the broker’s authorization to extend performance deadlines, the financing of the price as a closing contingency, procedures for cancellation of the agreement, a sale of other property as a closing contingency, cooperation to effect a §1031 transaction and limitations on monetary liability for breach of contract.

- Property conditions: The EP investor’s confirmation of the physical condition of the property as disclosed prior to acceptance is provided for in Section 12. It is confirmed by the seller’s delivery of reports, warranty policies, certifications, disclosures statements, an environmental, lead-based paint and earthquake safety booklet, any operating cost and income statements and any homeowners’ association (HOA) documents not handed to the EP investor prior to entry into the purchase agreement.

- Closing conditions: The escrow holder, escrow instruction arrangements and the date of closing are established in Section 13, as are title conditions, title insurance, hazard insurance, prorates and loan adjustments.

- Brokerage and agency: The release of sales data on the transaction to trade associations is authorized, the brokerage fee is set, and the delivery of the Agency Law Disclosure to both EP investor and seller and the disclosure of compliance with bonding requirements are provided for as set forth in Sections 14 and 15, as well as the confirmation of the agency undertaken by the brokers and their agents on behalf of one or both parties to the agreement.

- Seller’s right to cancel: Mandated by law, the notice to the owner-occupant seller whose home is in foreclosure is set forth in Section 16, disclosing the seller’s right to cancel the entire transaction within five business days after they enter into this agreement. The notice is one of two major additions imposed on standard purchase agreements by EP law and is of a larger text than the boilerplate provisions of the form as statutorily required. The other is the Notice of Cancellation used by the seller to implement the right to cancel during the five-business-day period following the seller’s acceptance.

- Signatures: The seller and EP investor bind each other to perform as agreed in the purchase agreement by signing and dating their signatures to establish the date of offer and acceptance.

- Cancellation Notice: Separate from the actual EP purchase agreement is the form completed by the EP investor, in duplicate, that the seller will use if they choose to cancel the agreement. By signing and delivering one of the easily detachable cancellation forms to the EP investor at any time before midnight of the fifth business day after the date the seller signs the agreement, the seller effectively cancels the entire EP purchase agreement, with or without reason.

Form navigation page published 05-2021.

Form last updated 01-2026.

Article: Form 156 – The equity purchase agreement

Form-of-the-Week: Equity Purchase Agreement and Equity Purchase Agreement with Short Sale Contingency – Forms 156 and 156-1

FARM: Client Q&A: What is an equity purchase transaction?

Article: Syndicating the equity purchase

Article: Equity purchase investments

Video: Purchasing the Equity in a Seller’s Residence in Foreclosure

I have been away from the industry for some time & I was wondering if equity purchase agreements are still required? I have spoken to a few real estate agents and investors and no one seems to know what I’m talking about when I refer to an Equity Purchase Agreement or NODPA. Did the laws change or are they simply unaware due to the lack of Foreclosures in the recent market? Thank you.

The form downloaded is form RPI 150 not RPI 156, please revise it, many thanks.

Hello! Thank you for alerting us to this error, the correct link has been updated in the article. You may also download RPI Form 156 here.

Best regards,

Editorial Staff