Why this matters: In these days of mandated buyer representation agreements, buyers and sellers, as well as brokers, wonder how transaction agents are paid. While negotiating what fee amount each broker receives has changed, who pays the fees has not. Who pays the broker fees is still separately set out by the buyer and seller agent in cost-of-closing disclosures prepared and reviewed with their client.

Laying out the financial consequences for buyers and sellers

The primary concern of a seller on reviewing a purchase agreement offer, whether accepted or countered, is knowing how much money they can expect to receive at closing. Sellers are aware the amount they receive — the net sales proceeds — will not equal the price the buyer pays to acquire the property.

What sellers don’t know, until disclosed by their agent, is the actual net cash value of their equity after clearing mortgage debt and paying closing costs on the sale. This dollar amount, a material fact requiring disclosure in any real estate transaction, determines what amount the seller may anticipate in exchange for conveying their property to the buyer.

To advise on this amount, the seller agent prepares and reviews a seller’s net sheet form with the client. [See RPI Form 310]

Similarly, buyers can assess the financial obligations they incur to buy a property only when accurately advised of cash expenditures by their agent before signing a purchase agreement offer. Buyers need sufficient funds at closing to cover both the purchase price and associated acquisition and mortgage costs.

To document the cash a buyer must gather from various sources to acquire a property, the buyer agent prepares and reviews with their client a buyer’s cost sheet. First, the buyer needs to meet with a mortgage loan originator (MLO) to obtain a Loan Estimate of the costs to take out the MLO’s mortgage so the buyer agent can enter the MLO’s figures on the cost sheet.

The buyer’s cost sheet presents the financial obligations the buyer can anticipate in the transaction. Here, the consumer is not surprised after they decide to buy property. [See RPI Form 311]

Related article:

California homebuyers think twice about high homeownership costs

Buyer and seller representation antitrust overhaul

Beginning January 2025, new rules require buyer agents — who expect to earn and retain a fee — to enter into a buyer representation agreement, also known as a BRA, with their buyer-clients as soon as practicable (ASAP). To comply with the ASAP aspect, the agreement is negotiated and signed when the broker decides to be employed and authorized to act on behalf of the buyer before they begin to locate real estate to be acquired.

This change requires a written agreement to formalize the relationship between the buyer and their agent at the outset of their agency. The employment agreement ensures certainty about:

- responsibilities owed each other;

- the fee amount;

- when the fee is earned;

- who will pay the fees; and

- fee enforcement. [See RPI Form 103.1 and 103.2]

Traditionally for past fixed fees, buyers operated under implicit, if not informal, oral arrangements with agents. They were most often unaware of the amount of their agent’s fee except that the seller or the seller broker paid it. Moving forward, agents deciding to work with a buyer must enter into a written agreement laying out the amount of the buyer broker fee — agreed to with the buyer.

The representation arrangement together with the follow-up purchase agreement offer, provides for the seller to pay the buyer broker fee, as occurred in the past. This has not changed. What has changed is the transparency resulting from the buyer broker compliance with the fee disclosure code which eliminated the seller broker interference enforced by the local multiple listing service (MLS). A further change obligates the buyer to see to it their broker gets paid, a change benefiting the buyer broker.

Sellers are fast to take a close look at the fees involved in the transaction. Rumors fly that the buyer pays their broker, rather than the buyer is merely involved in setting the amount of the fee their broker receives while the seller still pays all broker fees.

For seller brokers, the regulated fee arrangements become troublesome when the seller perceives they are paying their broker too much, say, in comparison to what they are to pay the buyer broker. Or, when the seller erroneously claims they are now paying fees the buyer is to pay under the new separate fee-setting procedures.

Brokers and agents are positioned to handle this crucial role of discussing the fees in sales transactions with their buyer and seller clients under the new antitrust code. Agents, as the messengers of change, advise their clients about broker fees at the outset of their solicitation of a seller or buyer to employ the broker. Again, the elimination of consumer surprise is the rule.

A seller broker when preparing a seller representation agreement for review with the seller, concurrently prepares a seller net sheet to disclose, among other costs, the total fees to be paid by the seller on the transaction — the fees due brokers on both sides of a transaction. [See RPI Form 310]

A buyer broker discloses the payment of the fee due the buyer broker in the buyer representation agreement as fee provisions note the buyer broker fee amount and that it will be paid by the seller under the terms of any purchase agreement offer. Payment of the fee is reviewed again when the buyer broker prepares a purchase agreement offer and a buyer’s cost sheet for review with the buyer-client, disclosing the fee the buyer owes is paid by the seller on closing. [See RPI Form 311]

Related article:

Buyer Representation Agreements: The end of the “gold standard”

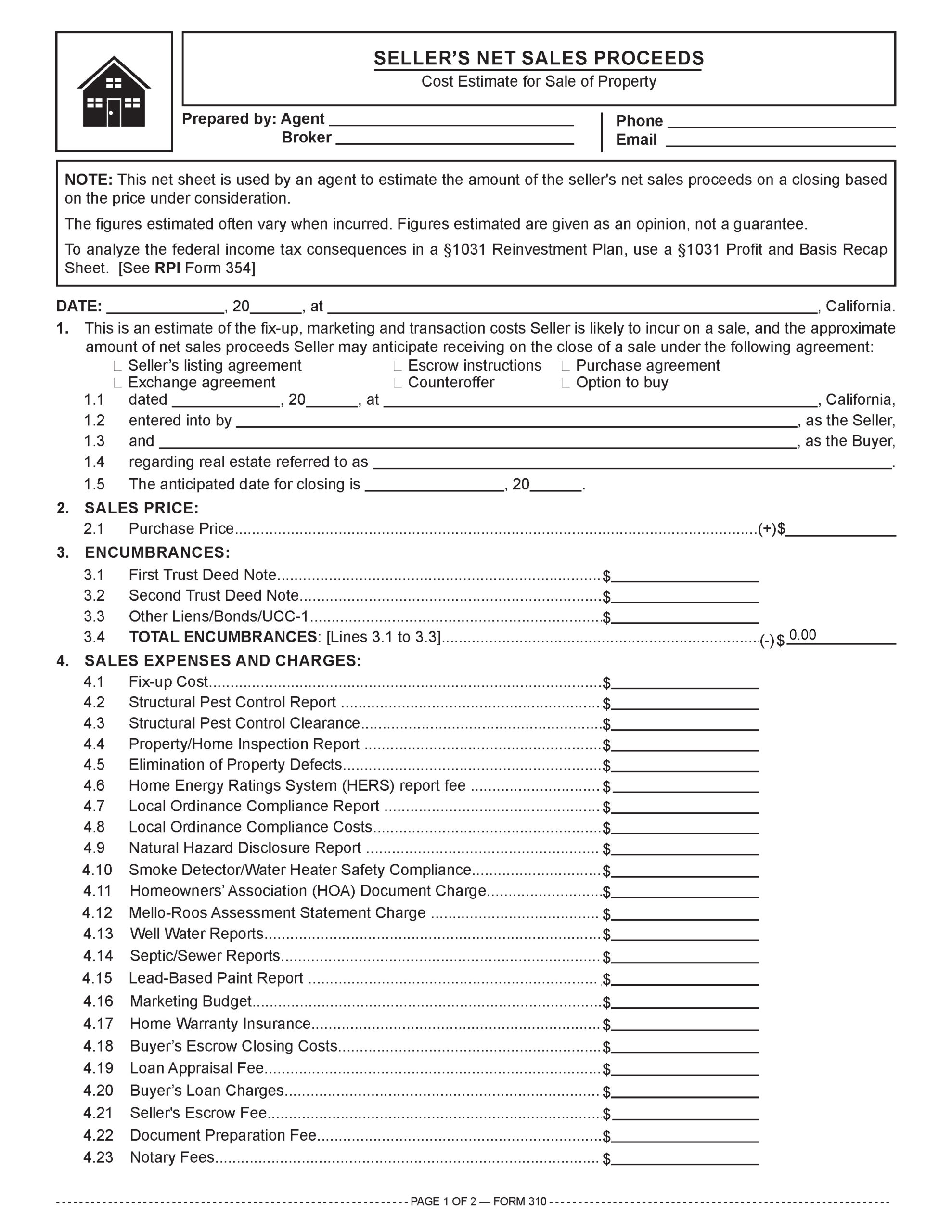

The seller’s net sheet

To review financial results of the price offered by a buyer in a purchase agreement, the seller broker uses a Seller’s Net Sales Proceeds form, also known as a seller’s net sheet. [See RPI Form 310]

The seller’s net sheet discloses the broker’s opinion of the offsets against the price the seller can expect on a sale at:

- the asking price agreed to in the seller representation agreement; or

- the price a buyer offers in a purchase agreement.

As a checklist, the seller broker or their agent uses a net sheet form to prepare and review with their seller the itemized sales costs and net proceeds the seller can expect on closing at the price and terms reviewed.

The amount of the seller’s net proceeds is easily determined and disclosed by the seller agent or calculated by programming for the net sheet form. The financial consequence of a sale is material information necessary as a prerequisite for a seller to agree to the price. Only when the seller has the net proceeds figure does the seller have knowledge sufficient to make a prudent decision to agree to an asking price or a buyer’s purchase price.

The seller’s net sheet displays the seller’s financial bottom line on the sale of a property. Thus, a net sheet review with a seller is part of every due diligence effort by a seller broker at the time of agreeing to represent the seller and again on receipt of a purchase agreement offer. [See RPI Form 310]

Critically, the time and effort expended to prepare a net sheet is a small due diligence premium to pay for assurance the agreed fees, costs and prorates are not disputed at the time of closing. The seller already knows what to expect on the close of the sales escrow.

The estimates entered on the net sheet by the seller broker or agent are based on information known or readily available to them on an inquiry of others (escrow officers or transaction coordinator (TC) programs).

Thus, the figures entered as estimates reflect the agent’s honestly held belief of the amounts the seller is likely to experience — they are not “guesstimates” which generate trouble for the broker.

Brokerage events triggering an agent’s preparation of the net sheet and review of its content with the seller include:

- soliciting or entering into a seller representation agreement [See RPI Form 102];

- submitting a buyer’s purchase agreement offer [See RPI Form 150];

- reviewing an offer to purchase an option [See RPI Form 161-1];

- preparing a counteroffer [See RPI Form 180]; and

- entering into an exchange agreement. [See RPI Form 171]

Analyzing the seller’s net sheet

A seller agent prepares the Seller’s Net Sales Proceeds form published by Realty Publications, Inc. (RPI) to inform their client about the expenditures the seller can expect to incur on the transfer of their real estate. [See RPI Form 310]

The seller’s net sheet itemizes:

- Encumbrances: improvement district bonds, mortgages and possible abstracts of judgment or tax liens to be assumed, reconveyed or released [See RPI form 310 §3];

- Expenses: repair and renovation expenditures, fees for investigative reports, broker fees and closing charges paid by the seller [See RPI Form 310 §4];

- Adjustments and Prorates: unpaid or prepaid items and any tenant deposits under rental or lease agreements taken over the buyer [See RPI Form 310 §§6 and 7]; and

- Net Proceeds: the dollar amount remaining of the purchase price funds after deducting all sales-related expenses, fees and charges, as well as the form the net proceeds will take (cash, mortgage, equity in replacement real estate, etc.). [See RPI Form 310 §8]

Related article:

The buyer’s cost sheet

The buyer’s cost sheet is designed as a checklist for the buyer agent to consider and enter their good faith estimate for the amount of costs their buyer can anticipate to finance and acquire a property, as well as the sources of the buyer’s funds. [See RPI Form 311]

The maximum price a buyer may offer for a property is the total funds they have available minus the acquisition costs.

Before a buyer’s cost sheet can be prepared for a buyer needing mortgage financing to fund the purchase price, the buyer agent arranges for their buyer-client to meet with a minimum of two MLOs. The MLOs will provide the buyer with a mandated Loan Estimate statement setting out the costs and cash requirements to take out a mortgage.

When the buyer broker determines and reviews with their buyer their transactional charges and mortgage costs, the buyer is aware of:

- the price they are paying for a property;

- the amount of upfront nonrecurring acquisition and mortgage charges to be paid (and who will pay them); and

- the source of all funds needed to close escrow and acquire the property.

Once the cost sheet has been reviewed, the buyer agent then undertakes steps to diligently locate qualifying properties, select one with the buyer for acquisition, and prepare and submit a purchase agreement offer. [See RPI Form 150 and 311]

Brokerage events triggering the buyer agent to prepare a cost sheet and review the costs with the buyer include:

- entering into a buyer representation agreement [See RPI Form 103.1 and 103.2];

- obtaining a Loan Estimate for an MLO’s mortgage;

- entering into a purchase agreement offer [See RPI Form 150]; and

- accepting a counteroffer. [See RPI Form 180]

Analyzing the buyer’s cost sheet

Buyer brokers and their agents use the Buyer’s Acquisition Costs — Cost Estimate for Acquisition of Property published by RPI when reviewing with their buyer-client the property pricing in a representation agreement, purchase agreement offer or counteroffer. The form allows the agent to prepare an estimate of acquisition costs and the source of funds to close a transaction. [See RPI Form 311]

The form contains a checklist of bookkeeping items typical of most purchases, including:

- acquisition costs;

- financing charges;

- prorations;

- funds required for an acquisition; and

- the buyer’s probable sources of funds. [See RPI Form 311]

Each section in the buyer’s cost sheet has a separate purpose, which cover:

- the acquisition and mortgage costs [See RPI Form 311 §§2 through 6];

- the closing charges (including prorations and adjustments) [See RPI Form 311 §§7 through 10]; and

- the buyer’s source of funds (savings, gifts, mortgages, etc.). [See RPI Form 311 §11]

Related article:

{kind=link}