Will income inequality lead to falling real estate prices?

- Yes. (52%, 13 Votes)

- No. (48%, 12 Votes)

Total Voters: 25

Homebuyers are wealthier by necessity

Homebuyers look a little different today, don’t they?

During the cheap-money years of the Millennium Boom, taking out a mortgage was as easy as having a pulse, walking into your local bank and signing on the dotted line. Anyone could become a homeowner — as long as you were willing to agree to risky, disguised mortgage terms. Indeed, many Millennium Boom homebuyers were under-qualified and over-leveraged, premature inductees into the world of homeownership.

We all know what happened next: the housing market crashed, millions were plunged underwater and the concurrent foreclosure and financial crises began.

Today we operate under a new paradigm more grounded in fundamentals. Homebuyers need to jump through a few more qualifying hoops to get a mortgage. One of these hoops is proving the ability-to-pay back the mortgage, which means sufficiently high income is a requirement.

A recent analysis of homebuyer incomes by CoreLogic shows average homebuyer incomes rose 20% from 2000-2008, after adjusting for inflation. Then during the Great Recession, homebuyer incomes fell back to 2003 levels and remained level from 2009-2012.

The most dramatic change in homebuyer incomes occurred in 2013-present. Homebuyer incomes have increased dramatically since 2013, far surpassing pre-recession levels. Homebuyer income is roughly 70% higher than it was in 2000, as of Q4 2014. This recent jump in average homebuyer income is indirectly due to the simultaneous rise in home prices. That is, the income of potential homebuyers is not rising. Rather, those on the cusp of qualifying to purchase are pushed out as home prices rise beyond reach. This leaves home buying to those wealthy enough to qualify. As a result, today’s homebuyers are made up of different, wealthier households than in the previous decade. Those who may have otherwise qualified to purchase under lower prices are now relegated to renting.

The income gap widens

From 2000-2013, median three-person household income (including rental and homeowner households) decreased:

- 9% for low-income households (with incomes below $44,700);

- 6% for middle-income households (with incomes between $44,700-$122,000); and

- 6% for high-income households (with incomes higher than $122,000).

Thus, today’s household incomes are level with 1997 incomes, according to the Pew Research Center. Yet home prices have risen an astounding 160% from 2000 through the end of 2013 (they have risen even higher, 220%, as of 2014).

Thus, even as average income declines, homebuyers need to be wealthier by necessity in order to enter into homeownership.

The long-term effect of rising home prices and falling incomesis viewed in California’s diminishing homeownership rate, as more homes end up in the hands of investors with extensive financial reserves. That’s one of the reasons why multi-family construction is recovering faster than single family residence (SFR) construction. New households need somewhere to live, and when they can’t qualify to purchase a home at today’s elevated prices, they turn increasingly to rental housing. Builders will keep up with demand for more rental housing as long as they aren’t encumbered by zoning restrictions.

San Francisco’s housing market is a prime example of what happens when zoning isn’t adjusted to meet demand. Here, construction starts are severely limited while housing expenses have no ceiling. Low- and mid-income households are forced out of the city and into the suburbs, and real estate transactions are severely stifled.

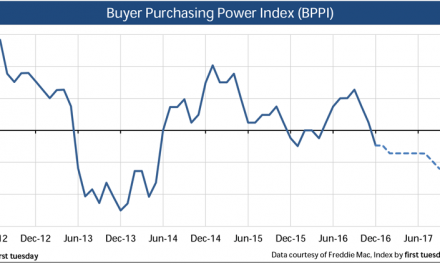

California’s homeownership rate is just over 53% as of Q4 2014, down from nearly 61% at the height of the Millennium Boom. California’s homeownership rate historically hovers around 55%. However, homeownership is going to linger below normal for the next several years. This is due not just to the income-home price imbalance, but to the further hit to buyer purchasing power from rising FRM rates beginning in late 2015 or early 2016.

Incomes linked to home prices

To review, from 2000 to 2013:

- the median three-person household income decreased 6%-9%;

- homebuyer incomes increased 70%; and

- home prices increased 160%.

This data supplies three critical conclusions:

- income growth since the Millennium Boom is imbalanced in favor of wealthier buyers, particularly in recent years;

- homeownership is increasingly out of reach for low- to mid-income households; and

- home prices are unsustainably high and need to fall to accommodate most owner-occupant incomes.

So why have prices continued to rise in the face of falling incomes?

Cash-heavy speculators drove the artificial (and temporary) 2013 price jump. This rapid price rise could never have been fueled by end user demand, since California incomes are insufficient to support such high prices.

Now that speculators have receded, our housing market rests in the hands of weary end users of real estate. Are they up to the challenge? Most of these potential homebuyers — those of low- to mid-income status — can no longer qualify to purchase a home now that home prices have risen so far out of reach. Thus, expect home prices to decline out of necessity throughout 2015, bottoming around mid-2016.

{kind=link}

First Tuesday is wrong once again.

Purchasing by Speculators and investors has not receded–but is still alive and well!

Every bank foreclosure put up for sale (always at 90% of market value) has five full asking price cash offers the first week from investors!!

The demand by investors to purchase rental houses is still there, and is not going away anytime soon.