Why this matters: Presently, new construction starts are inadequate, limited by either obstructive zoning or excessive construction costs which adversely affect inventory for sale and property pricing in 2026. Real estate agents and brokers looking for guidance in available real estate data need to understand owner and tenant occupancy turnover controls sales and leasing volume. Further, turnover is based on a balance between local for-sale inventory, construction starts and jobs.

Slow to move, both construction and pricing

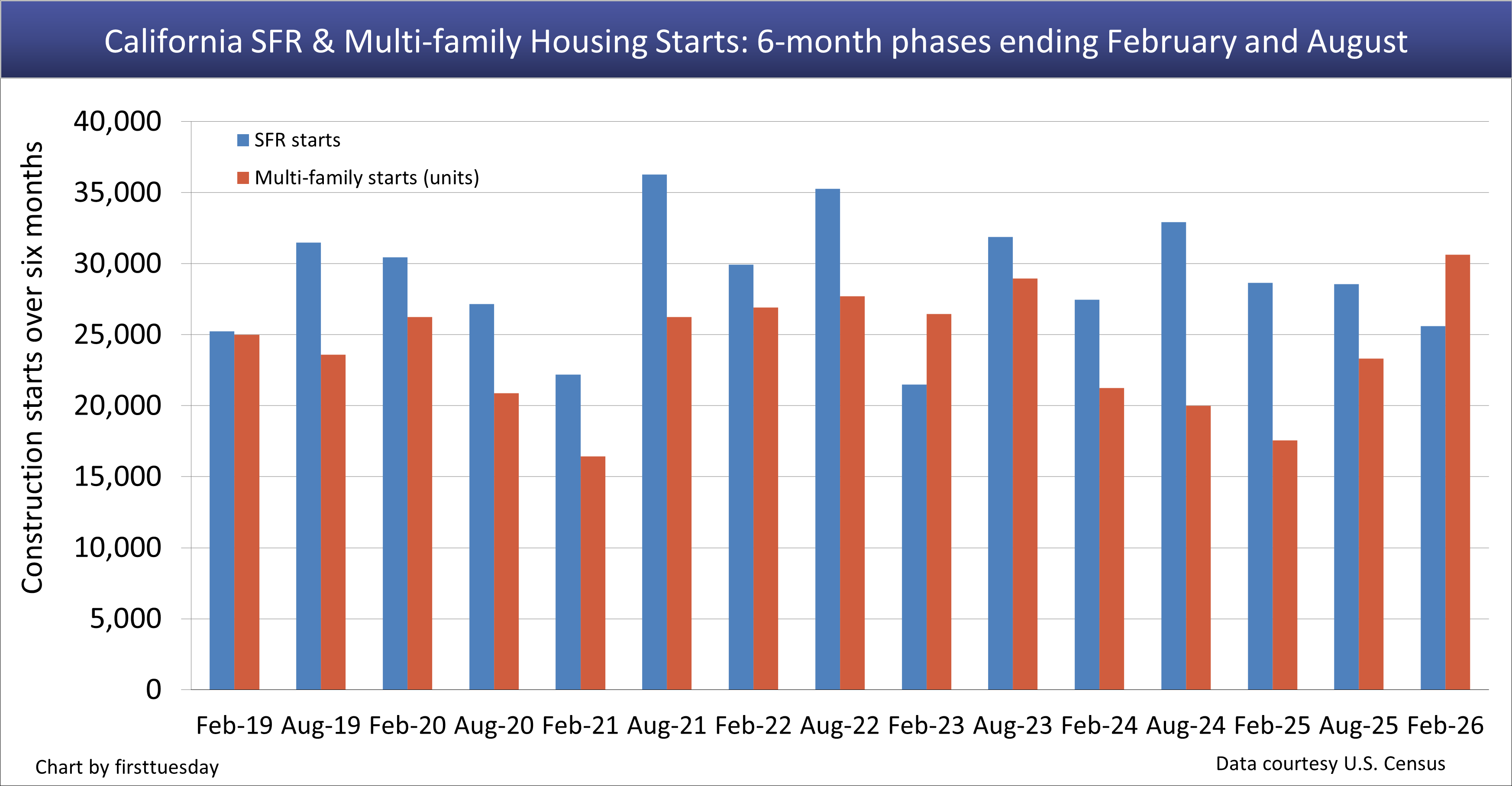

Single family residential (SFR) construction starts during the six-month phase ending February 2026 were down 11% from the same phase one year earlier. During the same six-month phase, multi–family construction starts were up 74.5% from a year earlier.

For a more balanced view, multi-family construction during the year 2025 experienced a 21% increase over the prior year, with starts on 47,200 new units. Multi-family rentals were in higher demand during this past decade compared to new SFRs since renting the family’s housing takes less of the monthly household income than ownership of similar property.

But to meet demand, new multi-family construction continues to hit national roadblocks in the form of labor and supply shortages, lack of local entrepreneurial general contractors and uncertainties about the cost of tariffs and wars on the price of materials. This is on top of politically aggressive not-in-my-backyard (NIMBY) advocates. These are headwinds stopping normal turnover and thus sales and leasing.

However, the increasing popularity of the builder’s remedy goes beyond pressuring local agencies to increase permits, the remedy now demands permits by reducing local politics to solely administrative issuance. Although not a new workaround, a builder’s remedy project is now controlled by state zoning and subdivision laws, instead of the local governmental hierarchy.

This allows bigger and taller residential projects to come about by overriding local housing elements when they do not comply with state housing law.

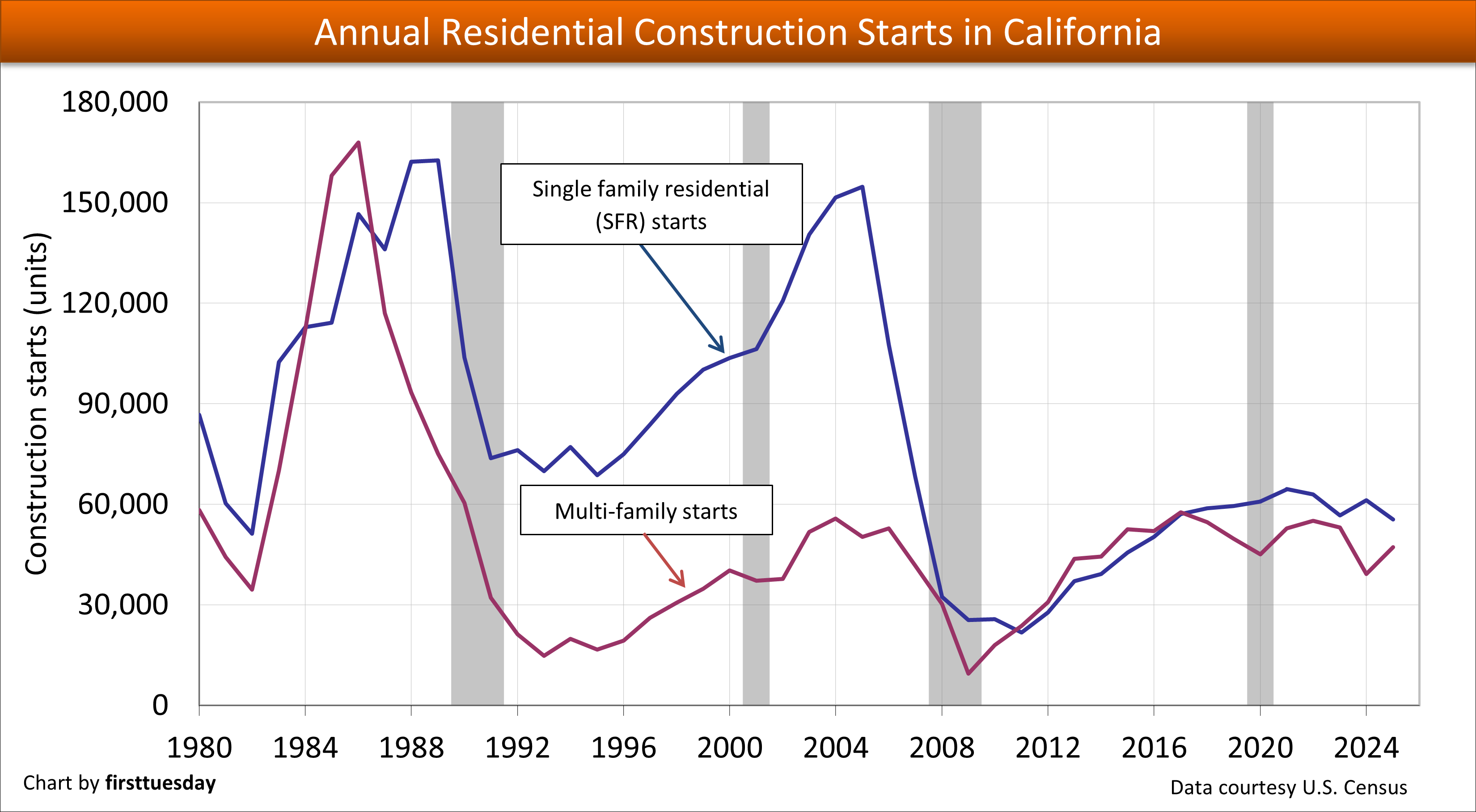

In contrast, SFR construction starts in 2025 were down 9% from the previous year, for a total under 55,500 new SFR starts. This downward movement follows a construction bounce in 2021. The surge then was the result of homebuyer fear of missing out (FOMO), low home-resale inventory, and demand for remote locations. Away from the coastal communities, construction starts occur without the zoning interference that takes place in coastal urban centers.

And yet, even with our population growth increasing overall since 2012, the construction of units was just a fraction of the starts needed to meet housing demand.

State-initiated legislative efforts to add to the low- and mid-tier housing stock — where the lack of starts has hit home — have focused on encouraging more multi-family construction in recent years. As a result, metro areas with the highest annual increases in multi-family construction include Los Angeles, Riverside and Santa Clara. The most anemic growth occurs where zoning remains deliberately restrictive for housing, including Orange County, San Francisco, and San Jose.

While builders, primarily local general contractors, were beginning to cash in on legislative incentives and rising homebuyer demand, leaping mortgage rates and downward spiraling sales volume (pulling pricing down in tow) crushed builder sentiment in 2022, causing starts to plummet. That is where builders find themselves in 2026.

Since the 2022 peak in pricing, housing across all price tiers in California’s major metro areas have not moved up which will eventually permit consumer inflation to catch up, rather than prompt a dramatic drop in the price tags. As the trend setter, the most expensive local housing felt the effects of our current real estate recession first.

As of January 2026, all tiers of housing in San Diego and the middle- and high-tier priced housing across Los Angeles are flat, having risen less than a full percentage point since January a year earlier. Only the high-tier of San Francisco and the low-tier of Los Angeles showed a forward annual increase, but for very different reasons. Los Angeles needed to spend 2025 rebuilding after devasting wildfires destroyed some 10,000 homes. Meanwhile, San Francisco’s most expensive real estate defies expectations due to extremely low inventory and high demand.

A study published in July 2025 showed existing California resale homes were priced significantly higher than new ones. One of the few states with this used-vs-new inversion, Californians looking to buy new homes face the largest difference in beneficial pricing compared to any other state in the country. While California homebuyers purchasing an existing home face 25% higher prices than buyers of new homes in the same area.

With prices overall starting to slip throughout the state, builders are motivated to grab the attention of buyers before recessionary prices push potential homeowners to wait for all home prices to bottom. Sellers of existing housing on the other hand may pull their property from the market rather than drop asking prices in order to compete with already less expensive brand-new homes.

Thus, residential construction starts will not reach their full potential until after the coming economy-wide recession. Prices will likely bottom by 2029, motivating buyers to act, as the real estate recovery begins to work its way out of its recession. Consumer inflation will incentivize equal or greater wage increases to coincide with yesterday’s flat prices that have held for four years and are likely to continue or decline as for-sale inventory climbs. These conditions allow job holders to pay effectively lower prices in the next few years.

Updated May13,2026.

Chart 1

This chart illustrates the number of California residential construction starts during semi-annual phases ending in February and August.

Chart update 5/13/26

Chart update 5/13/26

| Six-month period ending | Feb 2026 | Feb 2025 | Annual change |

| SFR Starts | 25,601 | 28,633 | -10.6% |

| Multi-family Starts | 30,616 | 17,545 | +74.5% |

| 2025 | 2024 | 2023 | 2005 peak | |

| SFR Starts | 55,483 | 61,229 | 56,655 | 154,700 |

| Multi-family Starts | 47,228 | 39,156 | 53,052 | 50,300 |

*Any forecasts made by firsttuesday are based on current new home sale trends, actual construction starts and current government policies.

Detached single family residential construction trends in California:

- 25,601 SFR starts took place in the six-month period ending February 2026. This is 3,032 fewer starts than occurred during the same period one year earlier, an 11% decrease.

- In 2025, SFR starts totaled 55,483. This is up 9.4%, or 5,746 starts, from 2024.

- For perspective, the past cycle’s peak year in SFR starts was 2005 with 155,000 starts. The following trough was 2011 with 22,000 starts, the year before our recent recovery set in following the Great Recession of 2008.

Detached SFR forecast:

- firsttuesday‘s projection for SFR starts in 2026 is a decrease from the prior year, as is currently the case with the beginning of 2026 down 8% compared to 2025 as of March. The forecast for 2026 is most affected by the downward pressure brought on by consistently high interest rates which slash buyer purchasing power, and increased consumer caution brought on by trade embargos, taxed imports and now wars.

- Expect SFR starts to remain below their potential in the next two plus years, until a recovery from the next recession picks up steam, likely around 2029.

- Subdivision final reports will remain low until local developers determine a return of aging first-time homebuyers is on their sales horizon.

- The next peak in SFR starts will likely occur during the boomlet period in the years following 2029-2030.

Multi-family housing construction trends:

- 30,616 multi-family housing starts took place in the six-month period ending February 2026. This is 13,071 more starts than occurred during the same period one year earlier, a 74.5% increase.

- 47,228 multi-family housing starts took place in 2025. This was 20.6% higher than 2024, and below 2018 when multi-family starts hit their most recent peak.

- For perspective, the past business cycle peak year in multi-family housing starts was 2004 with 55,822 starts. The lowest year was 2009 with just 9,500 multi-family housing starts as an excess of units already existed.

Multi-family housing forecast:

- firsttuesday forecasts multi-family housing starts to be up in 2026 from the past year. As the economy stumbles, builders of residential improvements are hampered by increased inflation from induced shortages in construction materials, workers panicked over volatile deportation conditions, mortgage lenders keeping a tight fist on funds, and taxes remaining elevated on imports.

- Due to the rise of the builder’s remedy, more multi-family housing projects will open in new, desirable locations. As SFR projects decline, the pressure on multi-family housing will incentivize new development through 2027.

- Multi-family housing starts were expected to rise at a gradual pace beginning in 2020, as several legislative changes aimed at increasing multi-family construction encouraged more building of dense, low- and mid-tier housing. However, pandemic disruptions and tightening lines of credit pushed multi-family construction numbers down significantly in 2020-2021, picking up significantly since 2022.

- For 2026, we will see a much-diminished residential development environment as the USA moves into its first world-wide trade war in 90 years. Meanwhile, the population consolidates into larger households per unit to weather the related causes of consumer inflation.

- Opportunities for residential construction wait until another economic revolution is installed in the USA, after moving into higher education and resulting skills following the end of a century of American industrial revolution started in the 20th century.

- The next peak for multi-family housing starts will likely appear after 2028 and beyond, but only after the coming recession bottoms and moves into recovery.

Statistics related to California housing:

- 14.88 million total housing units existed in California in 2024, 13.8 million of which are occupied and 7.7 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.

- Prior to 2020, California population growth had been increasing at a rate of 0.5%-1% per year. But California’s population has since begun to decline, the result of more deaths than births alongside more residents moving to other states than moving in. As an offset, those moving in possess higher education, skills and wealth than those moving out of California.

- Roughly 18.2 million people were employed in California in December 2025. This is above the number of jobs held at end of 2019, prior to the 2020 recession and pandemic economy, according to the California Employment Development Department (EDD).

- California’s residential rental vacancy rate was 4.8% in 2025.

Related articles:

California’s shifting residential vacancy rates tell a story

{kind=link}

What is the source of this data? It is interesting, but won’t be as useful in public policy debates unless we know the precise source of these numbers. Please reply with sourcesd. Thanks. J

construction is a very good way to produce more work and improve better living developments.

Could you fix the first number in this statement you have? $ million is wrong.

Statistics related to California housing:

4 million total housing units existed in California in 2019, 13.2 million of which are occupied and 7.2 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.

James,

Thank you for alerting us to this typo. We have fixed the error and gone ahead and updated these statistics with the latest numbers.

Thanks for reading!

Great content, thanks for sharing.

This make no mathematical sense.

“4 million total housing units existed in California in 2019, 13.2 million of which are occupied and 7.2 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.”

13.2 mil + 7.2 mil = 20.2 million. You said there were 4 million total. If you made such a basic error in math, how could we expect accuracy in any part of the article?

Double check your math.

The writer appears to have meant “14” not “4” million. !3.2 million occupied units means that about 800,000 were vacant. Subtract the 7.2 owner occupied from 13.8 million occupied to get 6.6 million occupied by renters. These numbers are consistent.

It would be helpful to know if any of the multi-family construction increase is privately financed as opposed to gov’t subsidized (ie: “affordable” construction.

Lots of useful information, thank you. I noted the construction chart going back to the 1980’s. The chart shows a total collapse of multi-family development beginning about 1986. I wonder how much of this may have been caused by the Reagan tax changes? Prior to that there was a period where limited partnerships built or bought apartments and commercial properties. After the tax change many people decided it was better to invest in a larger personal residence rather than a small income property and the limited partnership industry disappeared. Any thought on how tax law and government policy other than zoning laws can affect change?

If you add factors of living in CA… it is extremely costly. Land banking will do good but… having such a high tax state with cost of living so high… plus capital gain on both Federal and State end… does it really make sense???

I used to be positive about CA… real estate… as an investment…

Your own home, ok, but mortgage plus high property tax plus all others…

What is your intake?

New construction will only come back when we stop some of the wayward government t programs. No more debt forgiveness and no more refinancing underwater properties (Harp). It’s time to let the marketplace get back to normal buyer and seller demand conditions so employment will return and demand will new homes will follow. Just hope we elected the right person this time around.

THE BLACK SWAN

It interests us how so many persons, when offering their predictions as to what turn future events and trends might take, virtually NEVER figure in a black swan event.

What is that? A black swan event is a dramatic, even cataclysmic event that comes on suddenly and unexpectedly and can have a drastic effect on any prognostication based solely on observable, historical, or cyclical trends.

The huge storm in the East–hurricane Sandy–is a type of black swan event. A huge earthquake would be one on the West Coast. Such things can turn the trend-lines upside down. Massive damage means massive reconstruction. Is it good or bad for the economies so affected?

MASSIVE SOLAR EVENT IN THE NEAR FUTURE?

And no one is figuring in the possible catastrophic solar event that astrophysicists are saying could very likely hit before the end of 2012 or during 2013. (for more info on that see: AthenaAcademy.net/home/current_news). Would such an event bring negative consequences or positive? Apparently Earth has gone through such monumental solar events in the past.

Builders are “Re-active” to demand. They are NOT Pro-Active and build for the DEMAND. Long term investors shoot for 5-10 years out like me. I bought thousands of Acres in 2009 to 2012 at the BOTTOM BOTTOM LOW! Builders are consumers of LAND.