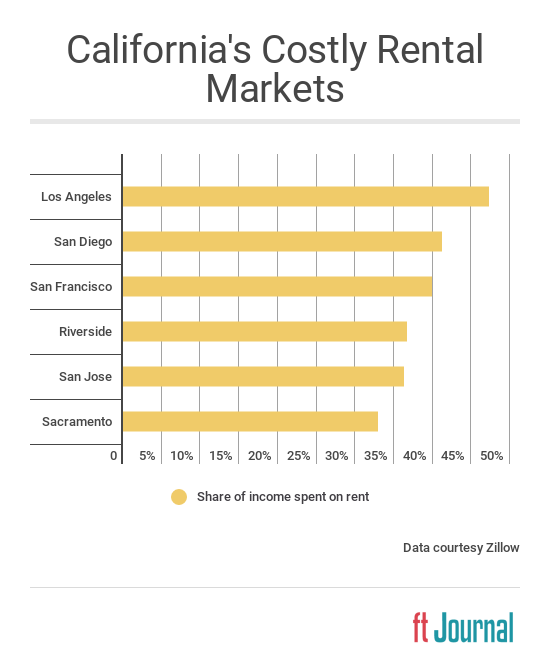

Six of the ten least affordable markets for renters are in California.

According to a Zillow analysis, the nation’s least affordable rental markets include:

Nationally, the average U.S. renter spends about 28% of their income on rent each month. Financial experts recommend keeping rent or mortgage payments to a maximum 31% of household income.

Zillow arrives at its most costly rental markets by assuming the area’s median income compared to the local median rent. This produces an abstraction, as it doesn’t represent any single renter — but it is still useful for real estate professionals to get an idea of each region’s trends.

And the trends are alarming — in Los Angeles, nearly half the average income is spent on rent. This is one very significant reason why Los Angeles’ homeless population has jumped in recent years — increasing 30% from 2016 to 2017 alone.

The trend is worrisome even in Sacramento, where the average renter spends a more manageable 33% of their income on rent. That’s because rent does not include the other housing costs associated with renting, namely utilities.

But is this information on the rental market really useful to real estate agents, who with rare exception focus on sales rather than rentals?

Why rentals matter to sales agents

Yes! Rents are one of the many gears that keep your local housing market moving. If rents become too high, other parts of the market will soon feel the effects.

Take Los Angeles for example. Renters here pay way too much for rent due to a shortage of low- and mid-tier rental options. As a result, they are forced to:

- pair up with roommates to make rent — an option that delays household formation; or

- pay a huge chunk of their paycheck on rent — an option that delays homeownership since there is little leftover to save and build up a down payment.

This dynamic is part of why homeownership is so low in Los Angeles, about 52% at the start of 2018. Another symptom of high rents is the low turnover we see in Los Angeles, along with low sales volume.

These dynamics are repeated across the state, and real estate professionals are beginning to feel the pinch of slowing sales.

The solution will arrive with more multi-family construction.

This type of construction showed minimal growth in 2017 after dipping in 2016, doing nothing to help the state’s rock bottom rental vacancy rate. But the coming years promise to be more productive for construction, as state legislators turn their focus to increasing the low- and mid-tier housing stock.

Expect more construction to help pull back rent increases in 2019-2020 and spur the next boom in home sales, which will occur around 2020-2021.

Related article:

{kind=link}