Here is the second post in our new study series — Down payment download — detailing the significant cost reductions achieved by mortgage-funded buyers when they acquire home ownership with a 20% cash down payment. This series showcases the damaging transfer of homebuyer wealth when a premature purchase of a home is paired with purchase-assist funding from a loan-to-value (LTV), threshold-busting mortgage.

Every DRE licensed agent branding themselves for a reliable practice in referral home sales must understand and communicate the financial consequences of the down payment amount to each prospective buyer-client who will use mortgage funds to purchase their first home.

Read the first installment Down payment download: Why 20%

Why this matters: First-time homebuyers considering the financial benefits evolving from a 20% down payment must balance societal pressure and institutional inducements to own, not rent, with the time needed to build savings out of their household income. Real estate agents and brokers trained in the math of mortgage-funded home purchases are qualified and thus duty bound to give their buyer-clients advice on decisions they must make for their largest, most complex financial arrangement.

Sourcing 20% down

What a household is able to pay monthly for their needs doesn’t change much, controlled primarily by their total household gross income. First-time homebuyers navigate the level of rent they pay for housing while budgeting to financially handle the purchase of the property they intend to own. With both means for possessing property — as a tenant or an owner — the limit a household can reasonably spend on housing with an acceptable standard of living is set by their income.

The borrowing capacity of a household establishes the amount of mortgage funding they can borrow; the total based on the current mortgage rate and monthly payments set as 31% of their gross income. The mortgage payments for ownership parallel what the same household can pay as a tenant for rent, say, 1/3rd of their gross income.

Nationally, the rent-burdened — those paying more than 1/3 of their income on housing costs — represent nearly half of renters now experiencing a reduced standard of living. With California’s proportionately high cost of housing, the ability to pay rent and concurrently pile up cash savings for a down payment severely interferes with household plans to own a home early in life.

But just because a homebuyer aims to pay the same monthly amount to own a home as they do to rent, does not mean that this buyer is getting the same value for their money when owning versus renting.

As a further limitation on indebted households, MLOs apply a debt-to-income ratio referencing payments on all forms of household debt to shield them from the risk of default by an insolvent borrower. The ratio, around 41% of gross income, sets a ceiling limiting the payment amount an indebted household can borrow at once and which dictates the mortgage principal.

The only option for buyers to compensate for the ceiling placed on their borrowing capacity due to existing debt is to offset their debt-to income ratio with:

- large cash reserves;

- consistent employment at the same place for more than five years;

- high credit rating; and

- a mortgage with a low loan-to-value ratio (LTV).

Today’s expensive move from renting to owning

The widening gap between renting and buying the same or comparable housing is even more pronounced with California’s current high real estate prices. But as always in California, a premium is paid for the allure of living or investing in property here, the appreciation factor used to evaluate property in California. The appreciation factor, estimated at 1.5% annually, is in addition to the annual consumer inflation figure generally held at 2%.

Amongst the largest metro areas, there are a few pockets where the buy-versus-rent gap has stalled or gone down since the previous year: namely San Diego, Sacramento, and Riverside.

Still, according to a 2023 study, California renters, compared to owners of the same or similar property, save on average:

- $1,400 per month in San Francisco;

- $1,200 per month in San Jose;

- $1,100 per month in Los Angeles;

- $800 per month in San Diego;

- $700 per month in Sacramento; and

- $550 per month in Riverside.

For homeowners, that dollar amount difference is pulled from their gross income every month. Meanwhile renters, with their greater flexibility, get to keep and use it at their own discretion. Homeowners pay a premium price, called pride of ownership, when putting extra money into ownership instead of renting a comparable property.

The financial squeeze of actively saving while paying rent is justified when quickly saving up a down payment. This explains why in a 2024 annual trends report from Zillow, 63% of buyers purchase and share ownership with at least one other person. 52% with a partner or spouse.

Even when sharing the commitment to save with another person, clients of a well-informed buyer agent are guided to other cost reductions and long-term savings.

Related article:

Today’s homebuyers take on the highest mortgage payments ever

Shop multiple MLOs, until you drop

Getting pre-qualified is the only way to get the precise picture of your financial ability to borrow capital to pay for a home. Apply for pre-qualification with at least three MLOs, for no other reason than to meet with them, either online or in person. You will learn through discussions with the MLO about the processes and procedures when you ultimately find a home and need a mortgage.

After you round up your 20% down payment, your shopping for an MLO entails comparison shopping for the lowest interest rate, lowest annual percentage rate (APR), lowest and fewest fees, and in turn the most favorable variety of mortgage payment terms. By applying with at least three MLOs you’ll see the significant variation in interest rate and APR quotes between lenders.

Most homebuyers make the huge mistake of applying only to one MLO, then telling the MLO they have no competitors or they were referred by their agent. This instantly eliminates the homebuyer’s natural ability to get the best mortgage arrangements simply by refusing to shop thoroughly and take advantage of an MLOs desire to beat their competition and garner your mortgage business. Without offers from more than one MLO for the type of mortgage you want, you certainly will leave money on the MLO’s table.

Also, with a 20% down payment, FHA mortgages provide more favorable rates while conventional mortgages increase the mortgage rate to compensate for the loss of default insurance.

To best establish the differences between offers made by different MLOs, homebuyers have the option of quickly comparing the rates, costs and terms offered by each MLO. All MLOs use the same loan estimate form for easy parallel cost comparison. Further, the buyer agent can fill out firsttuesday’s Mortgage Shopping Worksheet so the buyer can further analyze their options to make an informed decision. [See RPI Form 312]

Related article:

Monthly mortgage costs eliminated by 20% down

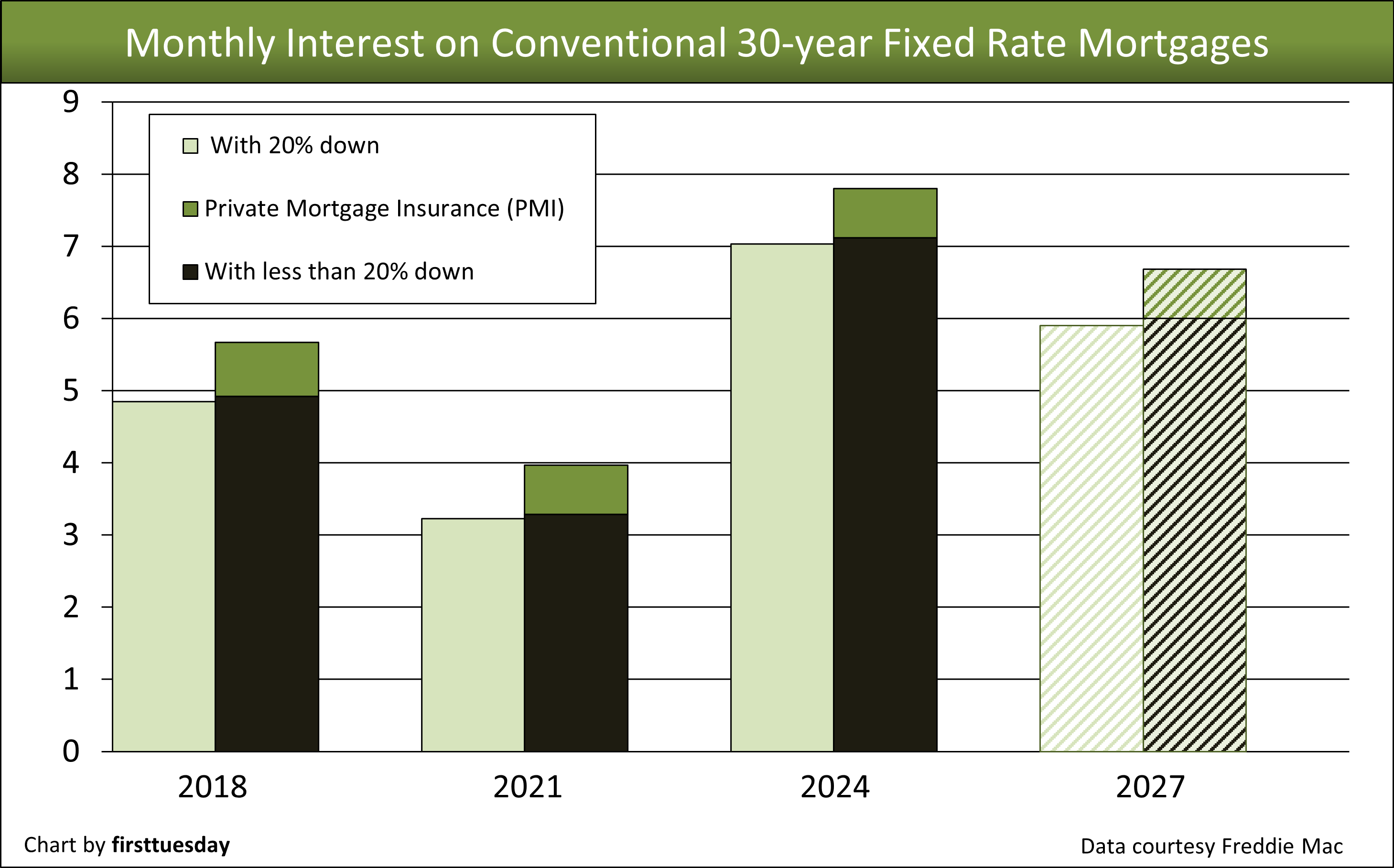

For mortgage funding needed to buy a home with less than a 20% down payment, the MLO offsets their elevated risk of loss by requiring mortgage default insurance. The annual premium is nearly 1% of the mortgage balance. This premium is paid by the homebuyer with the mortgage payments, treated no differently than additional interest. Suddenly, an August 2025 rate of 6.6% FRM actually totals 7.3%, the penalty for not savings a 20% down payment. As of August 2025, mortgage default insurance added a:

- 55% mortgage insurance premium (MIP) rate for an FHA mortgage with a 3.5% down payment, or

- 68% private mortgage insurance (PMI) rate for a similar mortgage with a 5% down payment.

These different rates alone undersell the story about all the costs. Unlike the FHA’s MIP, the PMI version of default insurance ends once a mortgage balance reaches an LTV of 80%. Of course, with a 20% down payment this default insurance premium is avoided, saved to be put to better household use – that standard of living thing.

Figure 1

Chart update 7/14/25

| 2024 | 2021 | 2018 | Predicted 2027 | |

| Mortgage interest rate with 20% down | 7.04% | 3.23% | 4.85% | 5.90% |

| Total monthly costs with less than 20% down | 7.80 | 3.97% | 5.67% | 6.68% |

The math of savings

For this example, our California buyer acquires a $500,000 home with a 3% down payment and mortgage funding at a 7% interest rate. Thus, the mortgage amount borrowed includes the extra $85,000 needed by the buyer to make a 20% down payment rather than the 3% down payment.

However, $85,000 short for a $100,000 down payment comes at a huge additional cost to the homebuyer. For our initial analysis of the additional costs of failing to gather up a 20% down payment, the buyer is hit with:

- interest on the $85,000, when not accumulated for a 20% down payment; plus

- the premium charge for mortgage default insurance.

The default insurance premium tacked onto a mortgage is additional “interest” of around 0.7% annually. However, it is calculated monthly on the entire principal balance of the mortgage, not just the amount exceeding 80% of property value. Again, a 20% down payment eliminates the default insurance premium and interest on the amount not borrowed to buy the home.

On a $500,000 home price with 3% down, MIP/PMI alone is $3,500 annually for a decade or more. This is $1,000 more than the interest earned annually on the $85,000 when left in a savings account – at $2,500.

Setting aside the fact this piggyback default insurance rate singularly reduces the owner’s standard of living, it is handed over as an additional decades-long expense for the personal satisfaction of hurrying into homeownership without prior planning.

In an alternative scenario of financial leveraging, a buyer with the 20% down payment parked in savings may decide to make only a 3% down payment. They keep the $85,000 cash as set aside for other investment opportunities. Here, the buyer needs a greater annual return from the alternative use of the $85,000 more than just the 7% interest paid annually on the $85,000 portion of the mortgage – $6,000 – and the default insurance premium paid on the total mortgage debt – $3,500.

These direct mortgage costs incurred solely on the $85,000 retained in savings total $9,500, an 11% cost to “borrow” the $85,000 mortgage money the buyer already had on hand. These direct costs are paid annually for lack of the 20% down versus the paltry $2,500 earned on $85,000 in a savings account, or an alternative and riskier bet on a very high return elsewhere exceeding the 11% cost of borrowing the $85,000.

Yes, a 20% down payment has an opportunity cost when using savings to buy a home, but here, the owner suffers a $7,000 annual net loss for simply deciding on a 3% down payment and retaining the savings.

Note: Future installments of our Down payment download series will cover the full financial breakdown of homeownership including benefits and costs of mortgage financing with a 20% down payment.

Related article:

Preparing your timeline ‘til ownership

A household looking to save up cash for a 20% down payment to own the hypothetical $500,000 residence needs to determine what amount they are going to set aside monthly in a savings account from their gross household income (before withholding). The key to sustainable home ownership while maintaining a respectable standard of living is to establish and commit to a savings plan, start saving the monthly budgeted amount and keep at it until achieved.

California’s mean household income was almost $134,500 in 2023 although specific regions vary drastically.

Estimating that a dual income household is setting aside 10% of their gross income every month, their goal of a full down payment of $100,000 is reached in about 7 to 8 years of the same saving routine. A very aggressive savings plan of, say, 25% of monthly income takes around 3 years, not including the modest interest built up in the interim period.

These savings efforts do not permit the aspiring homebuyer to live the present lifestyle of their acquaintances who do not save and thus diminish their future standard of living.

The household race to quickly save enough cash to enjoy the advantages flowing from a 20% down payment negates the anxiety in waiting longer to own their own piece of the community.

Lining up your bucks for a shot at ownership

All of these benefits come about when a buyer raises down payment funds from any source as part of their 20% down payment plan. A fortunate primary source nowadays can be a gift from a relative with a cash-heavy estate unneeded in their retirement.

Also, down payment assistance (DPA) programs are available for a homebuyer who qualifies by having:

- a credit score of 620 or higher;

- a favorable debt-to-income ratio;

- a reliable source of income; and

- status as a first-time homebuyer.

Some debt assistance programs comprise interest free loans with repayment when you sell the property or pay off your existing mortgage. Others are lump sum grants for a down payment that are not debts to be repaid, often granted based on your profession or inadequacy of income. In decades past of long-term employees, some employers contributed to down payments for good reason.

While programs have individual requirements a buyer must meet, the largest national contributor to buyers through DPA programs were banks. Government and nonprofits contributions made up 12% and 8% of buyers receiving assistance.

Buyers skeptical about what their cash savings can achieve are not alone. 60% of first-time buyers in 2024 reported purchasing their home with some amount of down payment assistance.

Even unconventional sources can bulk up the saving process. First-time homebuyers may withdraw up to $10,000 penalty-free from an IRA or Roth IRA account as a contribution to the down payment.

But the best path to homeownership for a household is still to save consistently, shop smart and depend on yourselves.

Economic cycles do bring home prices into range

Critical thinking for homebuyers with patience suggests the business cycles in our economy give cash savings a fully foreseeable opportunity value option. This value option is delivered cyclically as a decline in home prices. Home prices always drop from peak boom-time pricing, like what occurred mid-2022, as recessions inevitably set in allowing this option to be exercised.

Thus, a homebuyer acquires greater amenities as the prices of nicer homes trend downward into the homebuyer’s ideal price range. These are dollar facts, not dreams, and they come true in every business cycle for the cash-enhanced buyer.

All property prices are anticipated to fall in the coming years as for-sale inventories rise and dropping prices form a bottom, likely around 2028. This process in the real estate market today has been underway since the mid-2022 price peak. Better pricing, together with the near certainty mortgage rates will also decline, gives buyers the ability to borrow greater mortgage amounts.

Lower property pricing and lower mortgage rates mean a 20% down payment of $100,000 will buy a property with more amenities than previously planned. And — thank you very much — the mortgage payment will also be lower for that 80% LTV $400,000 mortgage origination. Thus, strong financial winds are now at your back.

The value of ownership

To this end, financially prepared buyers need to understand the economic context of timing their purchase, the opportunities that make purchasing a home an even stronger financial boon and ways to save successfully. 91% of 2024 buyers did not anticipate one or more of the costs they experienced on becoming an owner. This is the result of the classic nondisclosure MO persistent among real estate agents representing sellers. The seller agents will not get or will not provide operating cost data on a property they offer for sale. Buyer brokers are in no position to contact the seller to get data on these material facts for their buyer to make decisions. [See RPI form 306]

As the gatekeepers for a buyer’s entry into the real estate world, buyer agents are advocates as well as advisors for their buyer-clients. Thus the agent can empower their buyers through advice to make wiser financial decisions about buying and taking out a mortgage, long before their buyer signs that purchase agreement. To be most helpful for a buyer, a buyer agent always enters into a representation agreement authorizing them to locate and give advice on suitable property their buyer considers acquiring. [See RPI form 103.1]

Investment properties require special attention to fully understand the costs of purchasing, operating, and maintaining a property an investor considers for acquisition. Sellers and their brokers can best inform a buyer when the buyer requests information on the costs of ownership by using a property operating statement or RPI Form 352 — Annual Property Operating Date Sheet (APOD) and related property disclosure forms.

While an alert homebuyer watches the trends in weekly mortgage rates to best time their purchase, their buyer agent actively works to protect their client’s money from being lost – wasted – to the system of mortgage financing. A competent buyer agent knows their client finds the best mortgage opportunity when:

- applying to multiple MLOs;

- improving their credit score;

- timing their application to submit them to MLOs around October and November; and

- balancing their financial preparedness by rounding up at least a 20% down payment.

Opportunities like mortgage interest deductions (MID) and mortgage points benefit the richest homebuyers by reducing their income taxes through reporting paperwork and professional know-how.

Related article:

First-time homebuyers and households of color most impacted by interest rate hikes

Save in case of emergency

Cash reserves are not just investment tools, but vital emergency funds. A healthy emergency fund is a reserve set aside to cover immediate and urgent costs of sudden crises, ranging from medical bills to car trouble to veterinary costs. These unexpected and time-sensitive expenses have adverse consequences for the unprepared.

Dipping into an emergency fund is not to be treated lightly and never used as a cost saving tool. Any anticipated savings by using emergency funds instantly evaporates with a single instance of household bad luck.

Homeowners in trouble make up the majority of filers for Chapter 13 bankruptcy. Studies in other states show 80% of those who file a bankruptcy petition had homes with a loan-to-value ratio (LTV) over 90%. Rainy day funds and careful planning keep unanticipated monthly expenses from escalating into family destroying financial consequences.

Homebuyers who invest more capital – cash – into ownership up front are rewarded in the short and long term with significant cost reductions and a far greater return on investment over the life of the mortgage.

The responsibility is on the buyer and their agent to understand the limits of a potential homeowner’s ability to meet the financial obligations of ownership.

Editor’s note – The next article in the Down payment download series examines mortgage financing with different down payment amounts.

Related article:

Black mortgage applicants denied almost twice as often as white applicants

{kind=link}