The impacts of rising mortgage interest rates are rippling throughout the housing market. In fact, first tuesday readers recently voted interest rates will be the biggest factor to influence real estate in 2019.

One of the most direct impacts we are seeing with rising interest rates is decreased buyer purchasing power. This dynamic measures how much mortgage principal homebuyers are able to qualify for with the same income and mortgage payment. In other words, this time last year when mortgage rates were lower, a homebuyer was able to qualify for a higher purchase amount compared to a similar homebuyer in today’s market with the same mortgage payment. That’s because today’s buyer is seeing more of their payment go towards paying off the higher interest rate.

The result is homes rising beyond reach of mortgaged homebuyers. The hardest hit are those already operating at the top of their budget — for the most part, this includes low- and moderate-income homebuyers in search of suitable affordable housing.

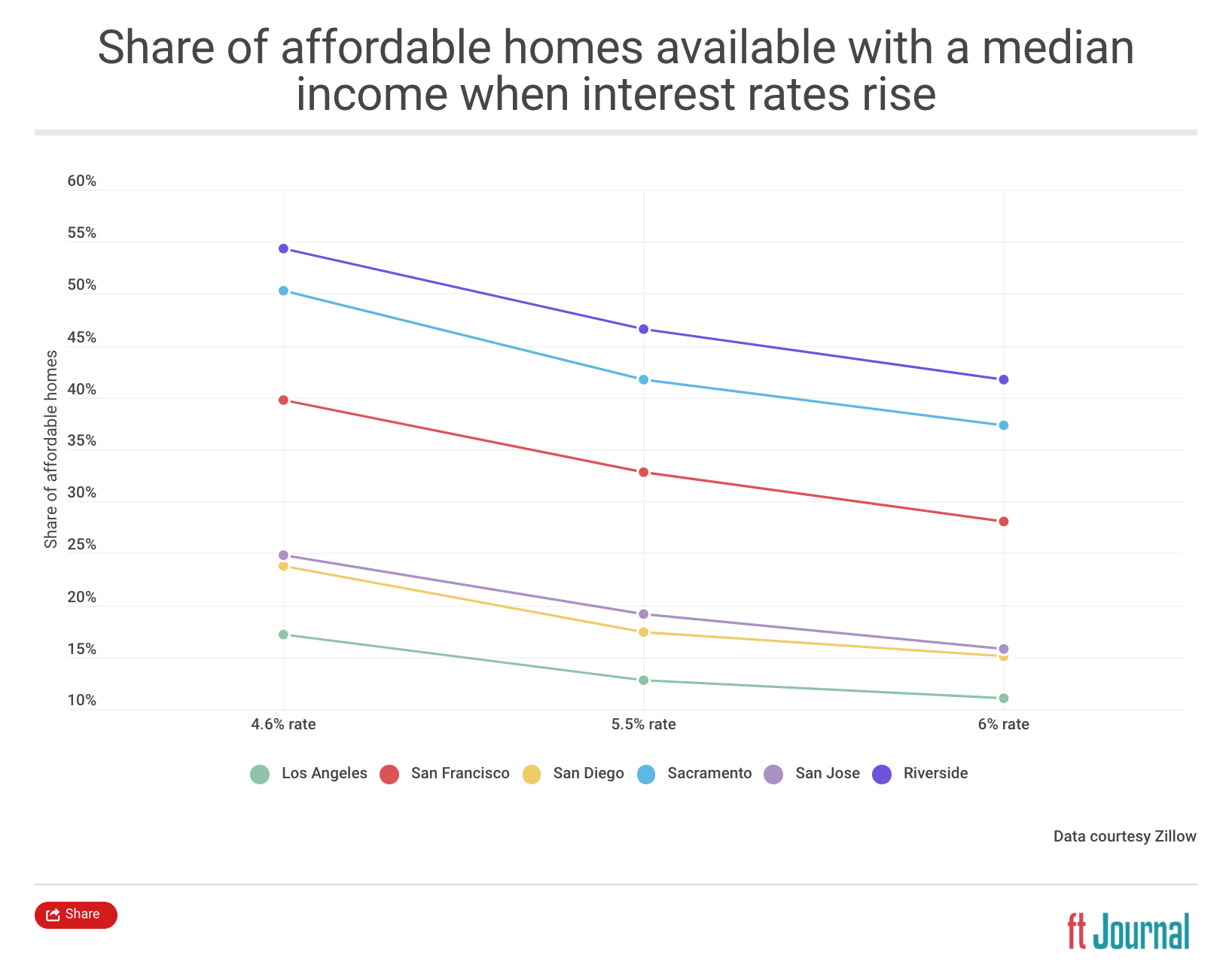

This chart shows the share of homes available to homebuyers in a given metro who earn the area’s median income and spend no more than 30% of their income on a monthly mortgage payment. This share is played out in California’s major metros, at:

- today’s average interest rate on a 30-year fixed rate mortgage (FRM);

- a 5.5% average interest rate; and

- a 6.0% average interest rate.

Nationally, increasing the 30-year FRM rate from today’s rate to 5.5% reduces the average price a typical homebuyer is able to pay by $35,000. If home values remain the same, this reduces the share of homes for which the average homebuyer qualifies by 5.4%, according to Zillow.

This isn’t just an exercise in math either — Zillow forecasts interest rates will increase from their present national average of 4.6% to 5.5% by the end of 2019. When rates continue to rise in later years, the number of homes affordable to the typical homebuyer will plummet.

The interest rate cycle

After three decades of falling from their heights reached in the mid-1980s, interest rates hit their cyclical bottom in 2012. While rates vary from day-to-day, U.S. interest rate trends follow a 60-year pattern, rising for about 30 years, then falling for the next 30 years, and repeat.

Now, as we make our way through the next interest rate cycle, the coming two-three decades will see a broad trend of rising rates. Higher rates will impact the real estate market in a number of ways.

Related article:

The lull before the storm: 16 factors set to rise with interest rates

One of these ways is explored in Zillow’s analysis, which shows how homebuyer purchasing power will be reduced under a rising rate regime. The author goes on to say that it will also discourage sellers from listing, as their purchasing power on a replacement property is also negatively impacted. This will spill over into rents, too, as fewer potential homebuyers are able to buy and so demand for rentals increases.

But one thing the report does not acknowledge is that home prices are determined ultimately not by sellers, but by homebuyers. The long-term impact of rising rates will be to pull back on home prices.

Homebuyers will be eager to remain at the same price point, even as their purchasing power is reduced by higher interest rates. Therefore, more offers will come in below listing price and more price cuts will occur (this is already happening). The result will be falling home prices.

first tuesday forecasts the overall trend for home prices will be down in 2019-2020. Prices are expected to bottom in 2021, rebounding in the years following.

{kind=link}

Excellent analysis. Suggest that agents/consultants should explain to buyers that higher interest rates may cause problems qualifying for the loan but they should always attempt to do the impossible to purchase a home because as interest rates go up, the value of the home goes up exponentially.