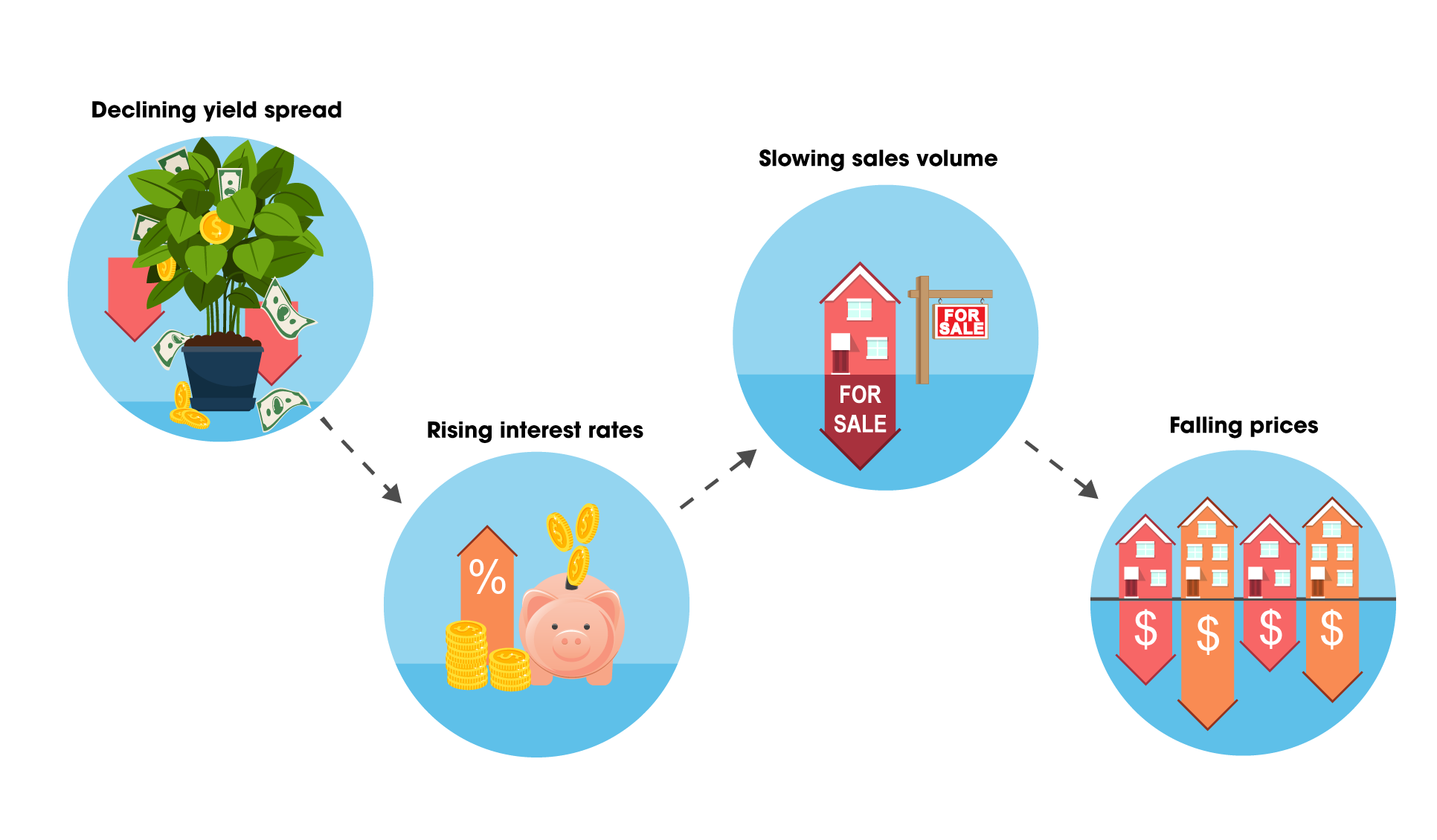

The yield spread continued to decline in Mary 2018, falling to below 1%. Experts expect this trajectory will continue for 12 or more months, and it most likely will. The surprise will be when it nears or hits zero, pancaking the economy into a recession some 12 months on. But you, dear reader, have now been warned.

For an introduction, the yield spread has prophetic power, its level indicating the likelihood of a recession, status quo or recovery expansion for the economy one year forward. The spread is a figure set as the difference between the short-term borrowing rate set by the Federal Reserve (the Fed) and interest rates on longer term Treasury Notes, determined by bond market activity.

Meanwhile, home prices continue in the opposite direction, confusing for some real estate investors caught between rising prices and signals of the coming economic slowdown. The average price of low-tier homes in California has increased 11% over a year earlier as of February 2018.

Today’s low yield spread suggests an economic slowdown, observable in reduced home sales volume in 2018-2019. By mid-2019, the yield spread will have slipped to near or at zero. Home price movement will then track in a delayed sympathetic response to the decelerating pace of sales volume experienced 12 months earlier, in 2018.

Complicating factors for the yield spread’s prognosis include 2018’s sluggish home sales volume, brought about by destructively low for-sale inventory and rising mortgage rates. Pent-up homebuyer demand is likely to diminish the negative effects of a slowing economy rather than simply melt away in reduced purchasing and increased savings. The housing shortage and buyer demand ensure California’s home price decline in the coming recession will be shallow and brief.

[infogram id=”yield-spread-pricing-recessions-1h7v4pewy5gd6k0″ prefix=”MQf”]This chart shows the yield spread (the red line) alongside California’s low-tier home price index (the blue line). The home price index shows average price movement in California’s three major cities: Los Angeles, San Diego and San Francisco.

The yield spread is a national figure, and is a leading indicator of future economic conditions throughout the nation’s economy.

What is the yield spread?

The yield spread is a monthly figure set as the difference between the 10-year Treasury Note (T-Note) and the 3-month Treasury Bill (T-Bill).

The figure is useful as a prognosticator of forward economic conditions because it reflects both:

- what the Federal Reserve (the Fed) thinks about the sustainability of the present level of inflation and employment conditions (shown in the 3-month T-Bill); and

- what bond market investors sense as the likely trend in future economic activity (shown in the 10-year T-Note).

Consider this pervasive cyclical event: several months to one year before each economic recession hits — a period of downturn in total goods and services — the yield spread consistently dips to near or below zero, called a yield spread inversion.

A yield spread inversion is produced by:

- the 10-year bond market forecasting a future downturn in the economy; and

- the Fed raising short-term interest rates to correct the level of inflation and employment and cool off an overheated economy.

Sometimes even a near-inversion is enough to bring on a recession.

When the yield spread approaches zero, real estate agents can expect a reduced home sales volume (which will already be slipping, as in 2018), lending and leasing. Then, within 12 months, prices will flatten and begin to drop, along with mortgage originations. Rents will slip, but not to the same degree as real estate sales volume and prices will drop. The delay in price adjustments following a peak in sales volume results from the sticky price phenomenon brought about by money illusions of sellers and landlords (and appraisers as they look backward for valuation trends, not forward).

The relationship between the yield spread and home prices

The yield spread shows an inverse relationship with home prices — moment by moment. That is, when the yield spread is declining, home prices are rising and vice-versa.

But there is much more to the chart than what is immediately apparent. That is, a rising yield spread does not directly cause home prices to fall. Rather, the yield spread heralds in a predictable series of events that become the shape of the economy and ultimately influence home prices, whether those of a recovery or a recession.

That’s because the yield spread indicates future economic conditions (not current conditions like consumer confidence reports). So when the yield spread begins steadily declining concurrent with the Fed consistently raising the short-term rate as began in Dec 2016, rising prices typically react in about two years by decelerating to flatten at a peak. Then prices typically retreat for two or three years until events cause prices to bottom. Thus, we are on course to see pricing peak in California housing by mid-2019.

For example, consider the 2008 Great Recession.

Leading up to 2008, the yield spread began declining as far back as mid-2004. In an effort to cool off an overheated economy, the Fed began at the same time to consistently increase its short-term rate.

This activity continued from mid-2004 through mid-2006 when the yield spread went below zero. In our current business cycle, the yield spread will not likely approach zero until mid-2019.

Meanwhile in the 2004-2006 period, as the Fed was increasing its short-term rate, long-term interest rates were also rising, discouraging homebuyers from taking out mortgages. The average interest rates on a 30-year fixed rate mortgage (FRM) rose from 5.7% in July 2005 to 6.8% one year later (more recently, FRM rates have been rising steadily since mid-2017, following the path before the Great Recession).

Also influential — due to the upward short-term rate drive by the Fed and a disproportionate share of homebuyers using adjustable rate mortgages (ARMs) — the average 5/1 ARM rate rose from 5.0% in January 2005 to 6.3% in July 2006.

Higher interest rates discouraged homebuyers, causing sales volume to reverse course in mid-2005 and decline as interest rates rose. But home prices continued to rise for another 12 months, finally peaking in mid-2006.

By the time home prices peaked in 2006, the yield spread had hit zero and was ready to rise back into positive territory (introducing a period of recovery). The Fed had done its job inducing a recession, and now busied itself pulling back rates in preparation for the recovery phase of the next business cycle.

The recession to come was intended to be a normal business recession, but then came the fallout from the massive mortgage fraud of the mid-2000s (mortgage lenders, grading agencies, appraisers, MLOs) that enveloped the entire global banking system, turning the slowdown into the Great Recession of 2008.

The yield spread and prices in 2018 and beyond

Today’s consistently falling yield spread indicates an economic slowdown in 2018 and 2019, with a brief recession likely in 2020. Sales are already slowing in response, also inhibited by today’s low inventory and rising long-term interest rates.

Still, prices continue to rise without surprise. Low-tier home prices are currently 11% higher than a year earlier, mid- and high-tier prices 9% higher.

But today’s flat sales volume and rising interest rates will eventually work to pull back home prices, likely beginning in mid-2019, before the recession sets in. first tuesday forecasts price increases will slow by the end of 2018 and flatten, peaking around mid-2019.

But the rate of housing starts of all types is a wild card for pricing — will starts dramatically increase in 2018, or remain sluggish in the move to get more housing on the markets? The timing of the flattening or pace of dropping prices will largely depend on the volume of starts.

Another wild card in this cycle is pent-up buyer demand. It is purported to be very strong, but will likely fall back with a recession, driving some to save, reduce consumer debt and avoid purchasing major items like homes — unless the price is right, part of the bottoming process in a recession. Builders will learn a lot about location (more than price range) in the coming recession. But the housing shortage is such that most homes on the market will sell within a reasonable time without major price cutting in projects closest to urban centers.

The yield spread dipped below one percent in mid-2018, due to the Fed raising the short-term rate and investors seeking the safety of U.S. Treasuries, signaling a greater likelihood of a recession. After the yield spread hits zero or near zero, likely in mid-2019, a recession will follow one year later. However, the coming recession will likely be brief and moderate, as consumer demands from income-earning residents will keep the economy afloat.

Also, the adverse effect on home prices during the coming recession will be minimal, as homebuyer demand currently outstrips inventory, the total opposite of inventory conditions and homebuyer demand going into the 2008 Great Recession. Construction starts will fill the supply gap left by today’s shrinking inventory. This will keep unemployment of undereducated and low-skilled portions of the population from rising too high in the upcoming recession — at least for California. Expect the unemployed across the nation to head our way and fill construction jobs.

The approaching recession will delay the next housing boom. This boom will be fueled by demand from a burgeoning first-time homebuyer population and retiring Baby Boomers who are poised to sell and relocate in large numbers.

Savvy real estate brokers and agents will keep an eye on the yield spread (also construction starts and “ice-cube” buyers) over the next two years to prepare for their involvement in future home sales, and program their conduct and finances accordingly.

{kind=link}

The recent tax reform also has an affect on housing as it takes away the likelihood of using your home costs as a tax deduction. Many people may not realize this until they do their taxes in 2019 (for 2018) and find their standard deduction is way more than their total itemized deductions. We may see quite a bit more homes on the market in spring 2019 as those with ample equity and over two years in their property try to cash out.