The number of young adults who own a home has declined significantly since the early 2000s. At the same time, the average student debt load has increased rapidly. Is this a coincidence, or are the two factors related?

A recent study by Federal Reserve economists answers: yes, many of the young adults who would otherwise have become homeowners in the past decade have been prevented due to their increasing levels of student debt.

Like any other type of debt, student loan debt is incompatible with qualifying for a mortgage, as it decreases the debt-to-income ratio (DTI). Most lenders allow DTIs no higher than 31% at the front-end (including the mortgage) and 43% at the back-end (other debts included). But unlike other common debts, such as auto or credit card loans, student debt balances tend to be much higher — and the schedule for pay-off is commonly set at a long 10-20 years.

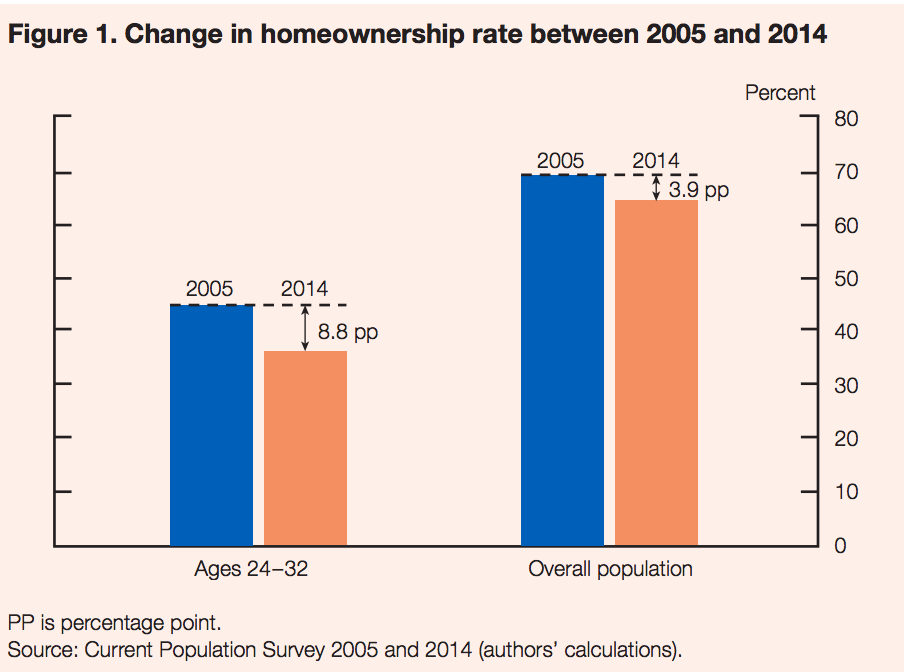

Source: Consumer and Community Context | Jan 2019

This chart from the Federal Reserve study shows the U.S. decline in homeownership rate from 2005 to 2014. Homeownership declined for all segments of the population from its inflated rate at the height of the Millennium Boom — 2005 — to a healthier level in 2014. But the decline was much worse for young adults, falling 8.8 percentage points for individuals aged 24-32 compared to 3.9 points for the general population.

During this time, the average U.S. student debt load for this age group doubled, from about $5,000 in 2005 to $10,000 in 2014. The study’s authors estimate approximately 20% of the steep decline in young adult homeownership is due to the rise in student loan debt. This translates to 400,000 fewer homeowners nationwide, due solely to student debt.

California homeownership declines among the young

Here in California, the average homeownership rate for 25-34 years-olds declined from:

- 43.5% in 2005; to

- 34.0% in 2014.

This 9.5 percentage point drop is a more dramatic loss than the U.S. average. One reason is related to the rising cost of education here and elsewhere.

Nationally, the average tuition rose 42% from 2006 to 2011. This is steep, but not as burdensome as here in California, where tuitions increased over 50% during those same five years, according to the College Board. Higher tuition payments translate directly to higher student loan amounts.

Further, more students are attending college and taking out student loans every year. This has positive implications in the broader housing market, as more college-educated residents means these renters and homebuyers are more likely to have higher incomes and quality, secure jobs, helpful when qualifying for a mortgage. But over the short-term, these expensive degrees mean a dramatic loss in purchasing power as long as former students are paying off the balances.

The good news is that the year is now 2019, a decade-and-a-half since tuition rates and student debt loads began to increase dramatically. Most student loan plans have payments set up to be paid off over ten years. Thus, while the market has been adjusting to higher student loan payments for several years now, the big pay-off is in sight for many.

Once student loans are paid off, these young adults will find themselves with hundreds of additional dollars in their pockets each month, which can easily be put towards saving up for a down payment.

Further, the housing market is at a tipping point in 2019, with prices tilting down. High prices during this past recovery have been especially difficult on this young, would-be homebuyer segment. Now that prices are poised to decrease over the coming years — expected to bottom in 2021 — first-time homebuyers will finally have the purchasing power available to jump in to homeownership. These first-time homebuyers will tend to be older, but also wiser, than previous generations of first-time homebuyers.

Related article:

{kind=link}

Education is an integral part to keep a society on a path to progress. Student debt amounts to $1.5 TRILLION of unsecured loans and if it is not managed properly it would make the last real estate crisis seem immaterial. The cost of education has become prohibitive because the centers of higher education have created a very expensive bureaucracy (pensions, coaches, salaries, perks, etc, etc). In comparison Canada’s cost is half that of the US’s cost of education. Just look at the UC System’s management compensation, huge salaries, benefits and pensions.

Youngsters and their parents get saddled with huge debt which that chokes their economic lives.