Mortgage interest rates have increased over half a percentage point since the beginning of November, representing a loss of thousands of dollars in buyer purchasing power.

One reason for the increase is the bond market anticipating the Federal Reserve’s (the Fed’s) move to increase interest rates, expected at the December 13-14 meeting. HousingWire indicates some bond market members see a rate hike as a certainty in December. However, the rate increase is expected to be small, perhaps just a quarter percentage point. Further, this time last year when the Fed was expected to increase the short-term interest rate — and they did, by half a percentage point — average mortgage rates inched higher by just 0.2 percentage points, and dropped following the rate increase.

Another reason for the steep change stems from shifting bond market expectations following the November 8 election. Interest rates tend to inch higher under a Republican-controlled government, as inflation tends to rise during Republican administrations. Higher inflation means members of the bond market will require higher returns — interest rates — to continue to exceed inflation, according to Bankrate.

How will the rate rise influence home sales going forward, and how have home sales already been impacted?

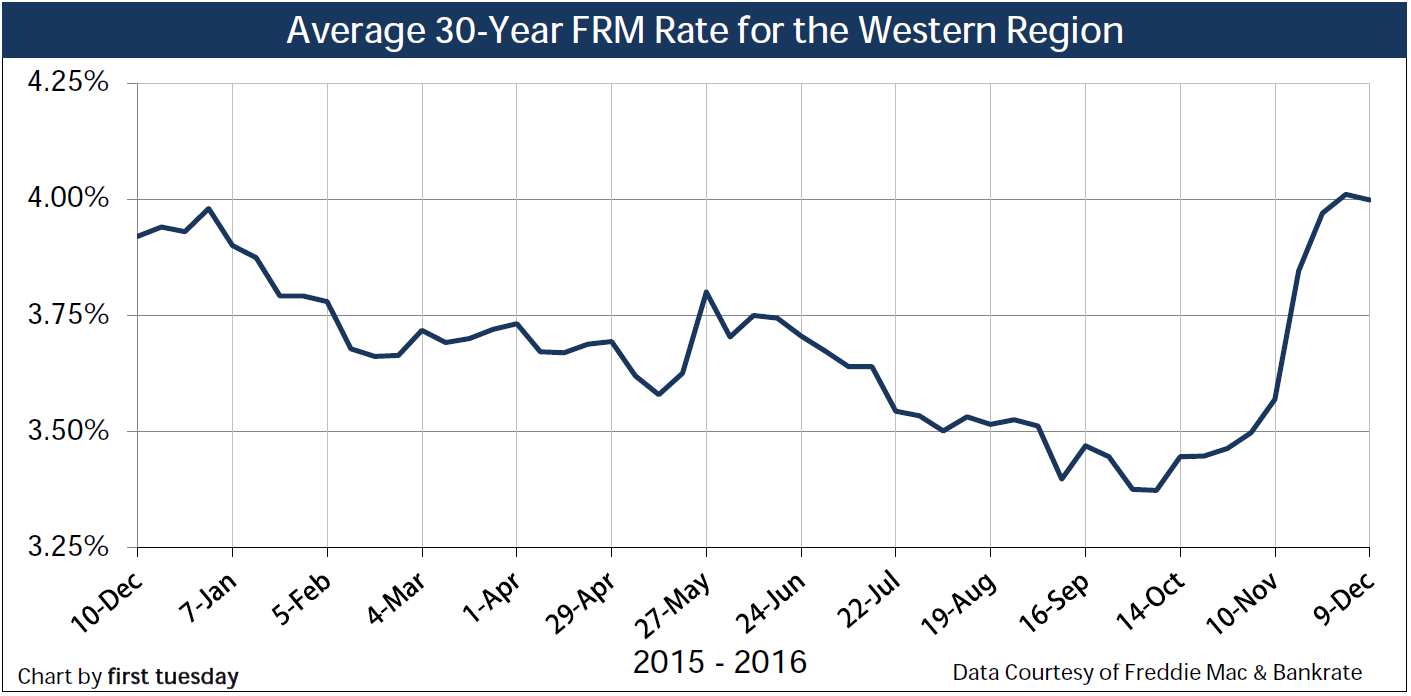

Two months ago, in the week ending October 7, the 30-year fixed rate mortgage (FRM) rate averaged 3.37% in California. At the time, a homebuyer with an average monthly household income of $5,016 and a 20% down payment had access to $350,600 in mortgage principal, based on a mortgage payment equal to 31% of their monthly income. This figure represents the typical homebuyer’s buyer purchasing power.

One month ago, in the week ending November 10, the 30-year FRM rate averaged 3.57%. This rate bump decreased the average mortgage principal available to $342,000.

Most recently, in the week ending December 9, the 30-year FRM rate averaged 4.0%. This rate increase lowered the average mortgage principal available to $325,800.

Therefore, over the course of just two months, the average homebuyer saw their buyer purchasing power decreased by about $25,000. The decrease is even worse nationwide, where average FRM rates have increased much faster, averaging around 4.25% in the first week of December.

Homebuyers searching during this period who are reliant on financing can choose to:

- pay the difference — equal to hundreds or thousands of dollars more over a year of payments;

- settle for a less expensive home;

- put off homeownership while they save for a bigger down payment; or

- give up and choose not to buy.

Redfin, a national real estate brokerage, surveyed homebuyers to find out their likely future course of action if rates rise a full percentage point or more. The survey found:

- 46% will settle for a less expensive home;

- 18% will put off homeownership while they save up a larger down payment; and

- only 7.5% will give up.

The remainder — 28.5% — said they won’t change their plans since they are not “sensitive” to rate changes. However, since the percentage of all-cash buyers who aren’t reliant on financing is typically less than this figure (the historical average of all-cash buyers in California is about 14%), it’s likely this high share of fancy-free buyers is somewhat optimistic. Unless the homebuyer is currently operating below their means, the difference in mortgage payment represented by the rate change can be overwhelming. The New York Times observes the rate change in the two weeks following the election caused the monthly payment on a $400,000 mortgage to rise by $700 a year, or about $60 a month.

Of course, today’s average rate of 4% is still well below the average pre-recession rate of 6%-6.5%. But with the sub-3.5% rates experienced just a couple months ago fresh in homebuyers’ minds, the difference is stark.

The market has already felt the impact of higher rates. The Mortgage Bankers Association (MBA) releases a nationwide weekly mortgage application survey. The number of mortgage applications has decreased significantly since the November 8 election, when mortgage rates began to shoot up. In the week ending:

- November 11, mortgage applications decreased 9.2% from the previous week;

- November 16, mortgage applications recovered some of the ground lost election week, increasing 5.5% from election week;

- November 25, mortgage applications fell again, decreasing 9.4% from the previous week (this includes an adjustment for Thanksgiving); and

- December 2, mortgage applications continued to decrease a slight 0.7% from the previous week.

For reference, mortgage applications tend to rise or fall by less than 4% each week this time of year (with the exception of the weeks following the 2012 election, when mortgage applications actually rose significantly).

While applications decrease, home sales in escrow where homebuyers didn’t lock-in their interest rates likely saw their deals killed, too. Further, even though home sales data is not yet available for the month of November, all of this activity points to a significant decrease in sales volume likely in November and December.

Home prices typically follow sales volume movement within 9-12 months. Home sales volume has already been slowing in the second half of 2016, and reports will likely show this previously gradual slowdown turning down more sharply in the last couple months of 2016, indicated by the decrease in mortgage applications. As a consequence, first tuesday forecasts home prices will fall in 2017.

Prices are already showing hesitation in some California regions, specifically in the expensive Bay Area markets and in some high-tier Southern California markets, where prices are level or declining compared to previous months but still above this same time last year.

Real estate and mortgage professionals: How do you think the mortgage rate increase is impacting sales volume and prices in your area? Share your experience in the comments below.

{kind=link}