MLO Mentor is an ongoing series covering compliance best practices for mortgage loan originators (MLOs). This article discusses the importance of appraisal independence. Enroll in firsttuesday’s 8-Hour NMLS CE to renew your California MLO license and learn more about fraud and abuse prevention in your practice.

Undue influence on property value

During the Millennium Boom, real estate valuations exceeded the historical trendline by more than double the true market value of the properties. The real estate industry has since discovered appraisers were unduly influenced by interested parties to arrive at specific values. This was one of the causes of the depressed market conditions during the Great Recession.

The following rules were enacted to curb the industry’s abusive influence over appraisal valuation.

Related article:

Correlation of Values and Creation of the Appraisal Report

These rules apply to appraisals of principal dwellings securing open- or closed-end personal-use loans, called covered transactions and to individuals who provide settlement services, called covered persons, including:

- lenders;

- appraisal management companies;

- real estate agents and brokers;

- loan originators;

- attorneys;

- title representatives; and

- escrow representatives. [12 Code of Federal Regulations §1026.42(a)-(b); 12 United States Code §2602(3)]

The borrower, guarantors and any individuals who live with the borrower but are not on the loan are not subject to these prohibitions. [Official Interpretation of 12 CFR §1026.42(b)(1)-2]

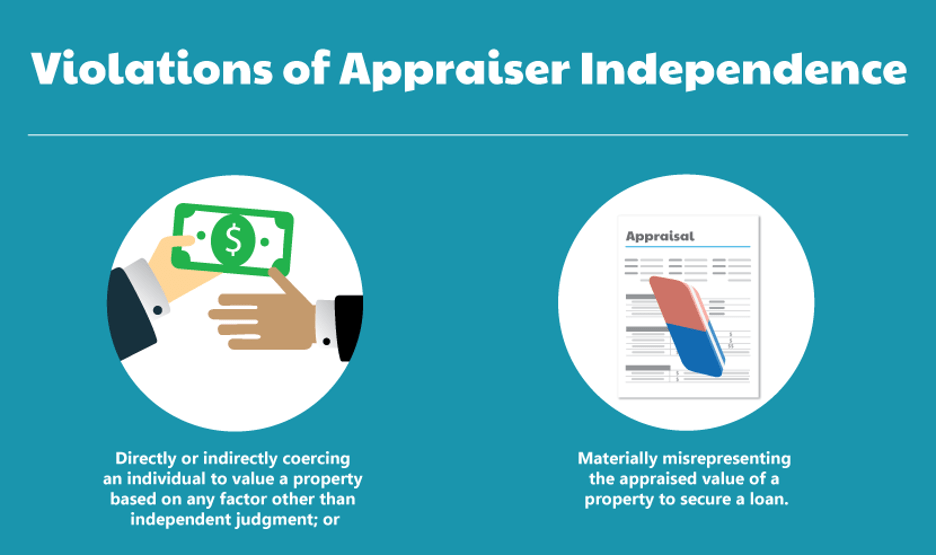

It is unlawful for a covered person to violate appraisal independence.

Violations include:

- directly or indirectly coercing, extorting, colluding with, instructing, bribing or intimidating any person who provides valuations into valuing a property based on any factor other than independent judgment; or

- materially misrepresenting the appraised value of a property to secure a loan. [12 CFR §1026.42(c)(1)-(2)]

Note that the prohibition against coercion is not only in relation to appraisers, but to any person providing values of a borrower’s principal dwelling. For instance, a covered person is prohibited from coercing a real estate agent to assign a value to a borrower’s principal dwelling based on anything other than the real estate agent’s independent judgment. [Official Interpretation of 12 CFR §1026.42(c)(1)-3]

Other examples of improper influence include:

- seeking to influence an appraiser to provide a minimum or maximum value on the dwelling;

- withholding or threatening to withhold timely payment unless the appraiser values a property above a certain amount;

- withholding or threatening to withhold future business from an appraiser unless the appraiser values a property above a certain amount;

- demoting, terminating or threatening to demote or terminate an appraiser due to the appraiser’s failure to value a property above a certain amount;

- conditioning the ordering of an appraisal report or the payment of an appraisal fee, salary or bonus on the opinion, conclusion, valuation or preliminary value estimate requested from an appraiser; and

- inducing an appraiser or another person connected with the loan to falsify the appraised value. [12 CFR §1026.42(c)(1)-(2)]

However, anyone with an interest in a real estate transaction may:

- ask an appraiser to consider additional relevant property information, including information regarding comparable properties;

- ask an appraiser to provide further explanation for the valuation;

- ask an appraiser to correct errors in the appraisal report;

- obtain multiple valuations in order to assure reliability in value assessment;

- withhold compensation due to a breach of contract or inferior service; or

- take action permitted or required by federal, state or agency regulations. [12 CFR §1026.42(c)(3)]

Related article:

Prohibitions against conflicts of interest

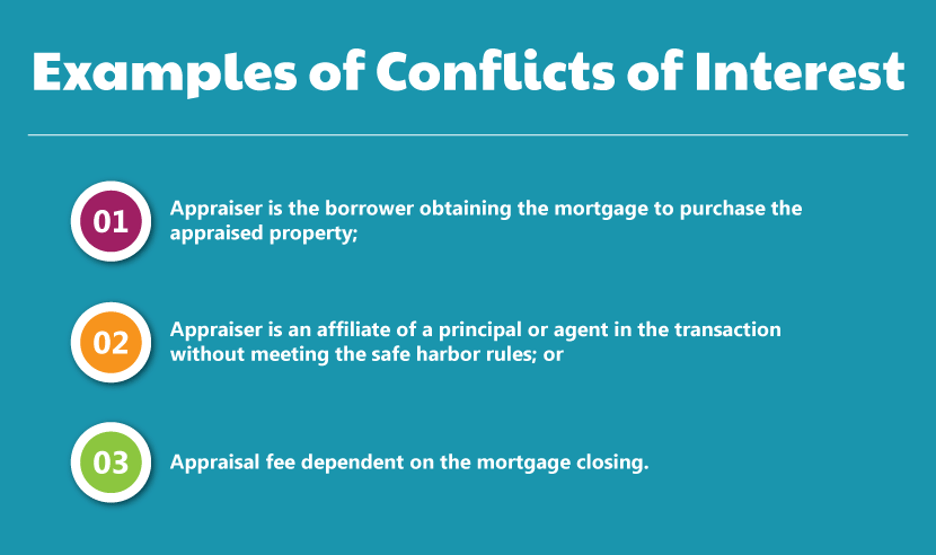

An appraiser or appraisal company is prohibited from having a direct or indirect interest, financial or otherwise, in the property being appraised. For instance, the appraiser cannot also be the borrower obtaining the loan to purchase the home. [12 CFR §1026.42(d)(1)]

An appraiser who appraises a property has a prohibited interest in the property if the appraiser or an affiliate of the appraiser serves as a covered person (loan officer, mortgage broker, lender, etc.) on the same transaction without meeting the safe harbor rules, or receives compensation dependent on the loan closing. [Official Interpretation of 12 CFR §1026.42(d)(1)(i)-2]

An appraiser is not in violation of the undue influence prohibition simply by being an employee or affiliate of the lender. The regulatory commentary on this issue is careful to state that the prohibition on undue influence is highly dependent on the facts of a specific situation. [12 CFR §1026.42(d)(1)(ii); Official Interpretation of 12 CFR §1026.42(d)(1)(ii)-1]

Two separate safe harbor tests exist to exempt an appraiser/covered person relationship from interested party prohibition.

When the covered person is an employee or affiliate of a lender which had assets of more than $250 million during the past two calendar years, the appraiser does not have a conflict of interest if:

- the compensation of the appraiser is based on factors other than the appraised value of a property or the closing of the covered transaction;

- the appraiser reports to staff other than the lender’s staff responsible for generating or approving covered transactions, called the loan production staff; and

- the loan production staff is not responsible in any way for selecting, retaining, recommending or influencing the appraisal staff. [12 CFR §1026.42(d)(2)]

When the covered person is an employee or affiliate of a lender which had assets of $250 million or less during the past two calendar years, the appraiser does not have a conflict of interest if:

- the compensation of the appraiser is based on factors other than the appraised value of a property or the closing of the covered transaction; and

- the lender requires that any person who orders, performs or reviews an appraisal for a covered transaction is unconnected with the decision to approve or not approve the same transaction, a separation referred to as a firewall. [12 CFR §1026.42(d)(3)]

In reviewing the need for appraiser independence, also called valuation independence, the Federal Reserve Board of Governors (who were the stewards of Regulation Z (Reg Z) at the time this rule was ushered in) acknowledged that smaller lenders, especially in less-populous areas of the country, would have a difficult time locating quality independent appraisal firms and appraisal management companies with which to work on a regular basis.

The inability to entirely divorce themselves from on-staff appraisers and affiliated appraisers would thereby decrease the flow of mortgage moneys to these areas — a result contrary to the consumer interest championed by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). Thus, the safe harbor tests were born.

The existence of two tiers of safe harbor tests reflects the practicality of relative levels of staff at a larger lender vs. a smaller lender. Smaller lenders, in general, are less likely to have discrete separations between appraisers and loan production staff. Thus, they are required to safeguard appraiser independence with a less formal, though no less stringent, firewall. [75 Federal Register 66554]

Paying appraisers

Lenders and their agents (including any appraisal management companies hired by the lender to oversee the appraisal process) must compensate fee appraisers at a rate that is reasonable in the market area of the property being appraised. [12 CFR §1026.42(f)(1)]

A fee appraiser is:

- a state-licensed or -certified appraiser who receives a fee for performing an appraisal but is not an employee of the entity ordering the appraisal; or

- an appraisal firm that employs licensed or certified appraisers and receives a fee for the appraisal, excluding appraisal management companies. [12 CFR §1026.42(f)(4)(i)]

Editor’s note — The companies in the second bullet point above are different from appraisal management companies. The role of appraisal management companies is to be the distinct managerial body for lenders, to allow lenders to comply with the conflict-of-interest avoidance rules for appraisals set forth by Reg Z. The companies referred to in the second bullet point are appraisal firms who employ appraisers, and who contract out their services to lenders and appraisal management companies. The Board specifically exempted these appraisal firms from the requirement of having to pay a “customary and reasonable” fee to the appraisers working under them because the firms often pay appraisers on an hourly basis and provide employment benefits (e.g., health insurance) to the appraisers in their employ. Requiring these firms to pay each employed appraiser the “full” price for an appraisal in addition to the existing employment consideration was acknowledged by the Board to be too great of a financial burden. [75 FR 66575]

In contrast, an appraisal management company performs the following actions on behalf of the lender:

- recruits, selects and retains fee appraisers;

- contracts with fee appraisers to perform appraisal services;

- manages the process of the appraisal, including ordering and submitting appraisal reports and general accounting for the appraisal process; and

- reviews and verifies appraisals. [12 CFR §1026.42(f)(4)(iii)]

The determination of a fee appraiser’s compensation must take into account:

- the type of property (e.g., attached or detached, single family residence vs. manufactured home);

- the scope of work (e.g., exterior only vs. interior and exterior, or number of comparable properties);

- the timeframe in which the appraisal is required to be performed;

- the fee appraiser’s qualifications;

- the fee appraiser’s experience and professional record; and

- the quality of the fee appraiser’s work. [12 CFR §1026.42(f)(2)(i)]

Alternatively, the lender can determine the fee appraiser’s compensation based on:

- fee schedules, studies or surveys of appraisal fees performed by objective third parties such as government agencies, schools or private research firms; or

- rates paid to a representative sample of appraisers in the geographic market of the property.

Fees paid to fee appraisers by appraisal management companies are not to be included in fee schedules, studies or surveys used to determine a fee appraiser’s compensation. [12 CFR §1026.42(f)(3)(iii)]

These compensation rules do not prohibit a lender from negotiating a volume-based discount with a fee appraiser, as long as the fees are still customary and reasonable. [Official Interpretation of 12 CFR §1026.42(f)(1)-5]

The lender is further prohibited from entering into any contracts or agreements which allow price fixing, market allocation or engaging in any actions which restrict an appraiser from entering a market, or force an appraiser to leave a market, in violation of antitrust laws. [12 CFR §1026.42(f)(2)(ii)]

Prohibition against extending credit and reporting requirements

If a lender is aware of a violation of appraisal independence, they are prohibited from using that appraisal report to make a loan, unless the lender has confirmed that the appraisal does not misrepresent the value of the property. [12 CFR §1026.42(e)]

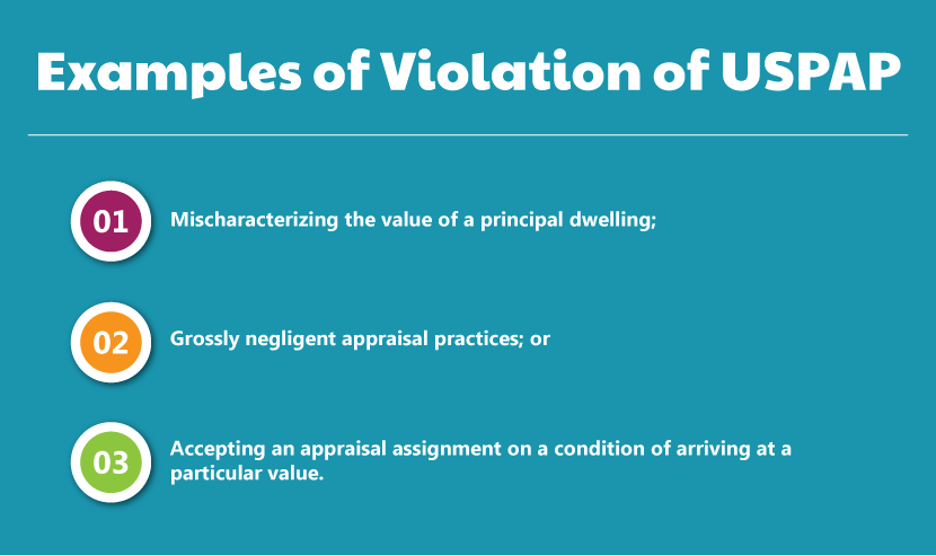

Additionally, a lender who becomes aware of any appraiser materially violating the USPAP or other federal or state rules controlling appraiser ethics must report the appraiser to the state agency regulating appraisers within a reasonable time of discovering the violation. A material violation is defined as any valuation which significantly affects the value of the borrower’s principal dwelling. [12 CFR §1026.42(g)]

Examples of material violations include:

- mischaracterizing the value of a principal dwelling;

- performing an assignment in a grossly negligent manner; or

- accepting an appraisal assignment on a condition of arriving at a particular value. [Official Interpretation of §1026.42(g)(1)-2]

Examples of nonmaterial violations which do not require reporting under this prohibition include:

- an appraiser’s disclosure of confidential information; or

- an appraiser’s failure to carry errors and omissions insurance. [Official Interpretation of §1026.42(g)(1)-3]

As a covered person, it’s important to keep in mind these appraisal rules and violations in order to prevent and curb abusive and improper influence.

Related article:

Mortgage Concepts: Is it a violation of appraiser independence?

{kind=link}