Why this matters: Those entering the real estate market need to understand business cycles which impact an annual return on an investment (ROI) in a parcel of real estate as compared to an annual return from an investment in a stock market business. The risks assumed are very different when compared.

Investment cycles

Which provides a better overall investment: stocks, or real estate?

First, consider timing. The time to acquire an investment opportunity is when prices have trended low and before an aggressive upward trend sets in, most recently experienced for real estate in 2013 with the pandemic-era being an outlier.

Stocks too have a pricing cycle. When it is not the time to buy it is because holding cash presents a value option, exercised by investing that stockpiled cash when prices recede to recession levels after they peaked.

Both investments have gatekeepers called brokers an investor has to deal with. It is extremely difficult to buy stocks or real estate without a broker being involved. While stockbrokers provide the margin financing, usually maxed at 50% of the stock’s price on purchase, real estate brokers may provide the financing:

- by acting as an MLO;

- referring the buyer to an MLO; or

- placing the mortgage for funding with another source.

Both real estate and stock markets have periods of profitability peaks and troughs. They run closely to each other as they are controlled by the same economic conditions present in each business cycle’s period of recession, recovery, repeat. The economy is always in flux, and a flat appearing period is merely a temporary solace when the economy is shifting into a recession or recovery period.

Stock prices, now at historic heights, are up 7% from a year earlier in the first quarter (Q1) of 2025. This rapid stock price rise reflects a temperamental economic situation, as the U.S. economy’s uncertainty tumbles into the current recession.

California home prices have taken a steadier path of a 3% year over increase in Q1 2025, continuing long term growth with 2022 as the beginning of an exception. As interest rates have soared following the historic lows of 2020-2021, buyer purchasing power has dropped, putting the brakes on home price increases and slowly reversing course.

Home prices are also far over their historic mean price and a continuing rise in capitalization rate settings are now hitting the value of investment properties. All pricing is set to plunge in the near future, not likely to find a bottom until around 2028.

Uncertain economic conditions are adversely affecting jobs, import taxes are raising the cost of imported products and materials, higher than normal consumer inflation shows no clear sign when it will come down, and federal management of immigration blur forecasts for the housing market.

For real estate investors not wanting or needing to cash out, 2025-2027 remains a hold phase. For the next buy phase, look ahead for the bottoming and beginning rebound for the real estate market’s best pricing and mortgage rate period, expected to arrive after 2028.

Updated August 20, 2025.

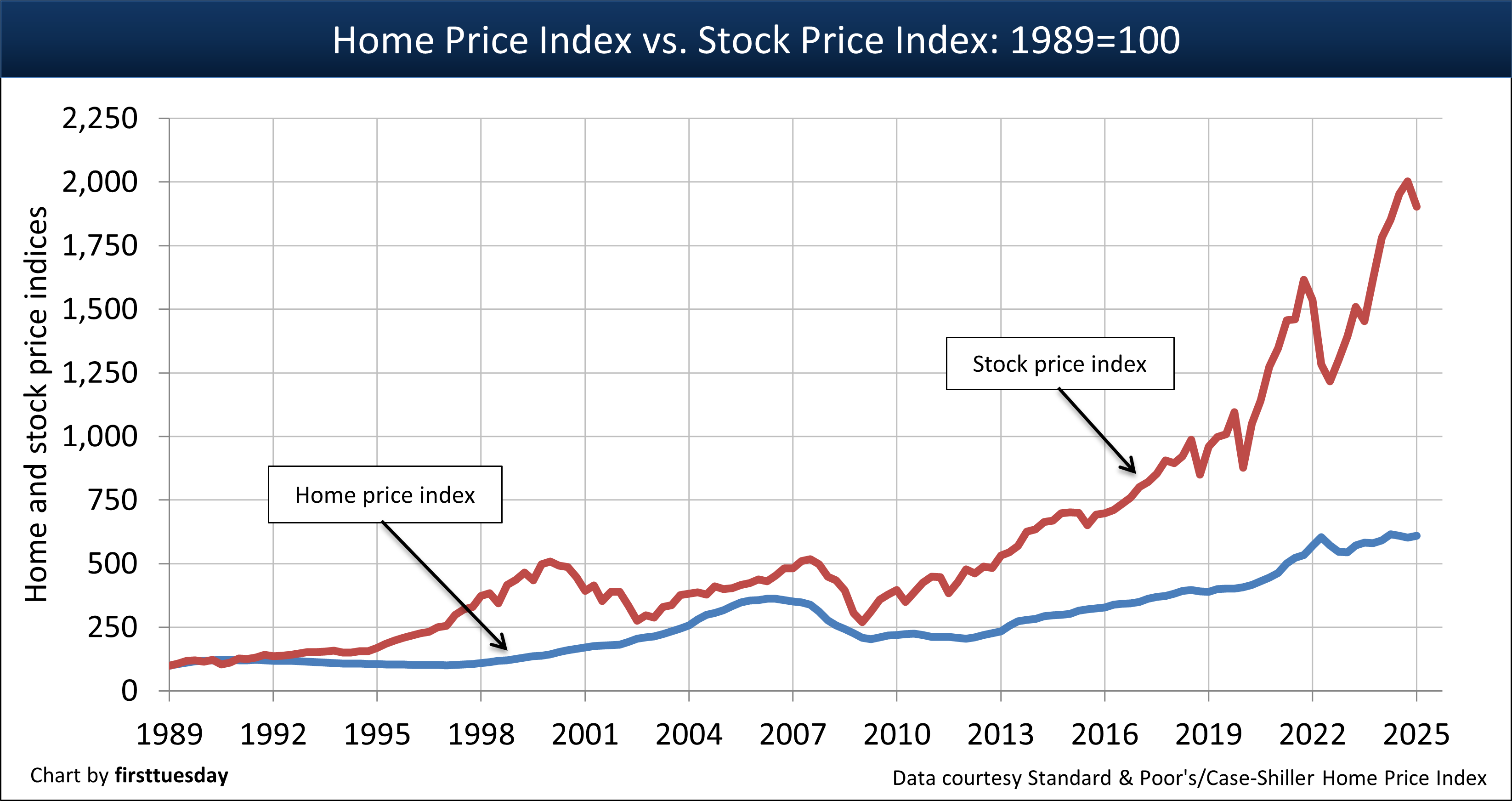

Editor’s note — The chart above displays the average price index of homes sold in three California areas: Los Angeles, San Diego and San Francisco. Other types of real estate (i.e., commercial) are not included, but their pricing runs parallel to home price movements and leads movement.

Editor’s note — The chart above displays the average price index of homes sold in three California areas: Los Angeles, San Diego and San Francisco. Other types of real estate (i.e., commercial) are not included, but their pricing runs parallel to home price movements and leads movement.

Chart update 8/20/25

| Q1 2025 | Q1 2024 | Quarterly change | Annual change | |

| Home price index 1989=100 | 431 | 419 | +1% | +3% |

| Stock price index 1989=100 | 1,903 | 1,782 | -5% | +7% |

Stocks: a volatile choice

The chart above displays two indices:

- California home prices; and

- stock prices (S&P 500).

These indices track price movement (not actual prices). The stock price index in Q1 2025 reflected a growth of 7% from a year earlier. During the same period, California home prices are 3% higher, though now falling back each month. Expect changes to the annual home price to turn negative heading into 2026 as rapidly rising inventory for sale is made unstable when owners of many available properties simply test the market and bail when they do not get their asking price quickly.

Home prices rise and fall in a generally smooth fashion, as seen in the chart above. Stock prices, on the other hand, display much more volatile movements within very short time periods. That’s because stock transactions occur more rapidly than home sales due to liquidity differences.

For a home sale, it takes months to market property for sale, locate a buyer who enters into a purchase agreement and navigate through an escrow period for mortgage approval and documentation in order to close. Conversely, stocks are traded – both bought and sold – in an instant.

Thus, stock prices tend to rise or fall based on momentum much more quickly than home prices. Further, stocks, unlike real estate, are frequently bought on rumor, sold on facts.

Stock prices: a history of speculative trading

Stocks picked up steam in the 1980s, rising more quickly from 1990 to the 2010s — a period when interest rate reductions declined to zero in 2013 and stagnated until 2017. The long-term upward price slope was subject to a steep incline in the mid-1980s, the dot-com bubble of 2000 and again in the Great Recession of 2008.

Each were brought on as the Federal Reserve (the Fed) raised interest rates to send the country into routine business recessions and adjust the economy for excesses — as again took place in 2017 during the zero lower bound interest rate hangover.

Stock bubbles occur when speculators essentially seek profits on momentum bets without concern for overvaluing a stock or respecting investment fundamentals. Prudent investors who look forward with long-term purchase stock they perceive as currently undervalued based on historical reference, anticipate its price will grow in the future and reach its full value.

In the case of the mid-2000s stock bubble, called the commodities bubble (or sometimes the commodities super cycle). This bubble imploded in 2008 when the financial crisis hit and the Great Recession emerged. However, in 2009 the stock market recovered due in large part to the advent of zero-cost money for leveraging acquisitions. As of mid-2025, the stock market is still up — though rather unstable — for much the same reason: easy financing to leverage all purchases.

Real estate: the choice for greater stability

Real estate prices experience bubbles, too. They are just not usually as explosive as stock market bubbles. The primary difference is the liquidity challenge present in real estate sales. An exception is the Millennium Boom, which was due mostly to Wall Street infiltrating the real estate business by becoming its near-exclusive source of mortgage funding for the entire nation.

Compared to stock investors, who may lose a fortune in a single day, real estate income property investors have a much longer time period to react to changing property sales volume and pricing in order to minimize their losses through liquidation.

Further, while enduring a real estate bubble is financially problematic for short-term investors — speculators — bubbles have much less influence on long-term real estate investors. Their losses are primarily limited to tolerable short-term reductions in rental income when not excessively leveraged. During a recession, buy-to-let investors are a stabilizing influence on prices as they are able to invest in property and do so without borrowing funds at high mortgage rates.

Historically, income property prices are drawn toward the mean price trendline, a reflection of the gradual upward movement of consumer inflation — and wages — over the years. Unlike stocks, real estate is fundamentally tied to the cost of labor, materials and space. That said, cyclical real estate prices change in tandem with local demographic’s personal income and population.

Levels of involvement

Both require different levels to manage the investment. Real estate demands the investor’s time and effort reviewing a property that a stock market investment does not, despite both involving evaluating the type of product and potential for growth, net profits and dividends. The aim of real estate investments is to either:

- locate a return which includes a premium rate for the time spent by an owner operating the property; or

- retain property management at the expense of a management fee to handle the constant mundane needs of property and tenants.

For stocks, the business comes with management who tend to the daily demands of company services, inventory and employees while the investor is passively involved — like real estate under 100% property management.

Evaluating the investment

Real estate investments are based on a capitalization rate set separately for every parcel at the time of purchase analyzing:

- the type of use a tenant makes of the property;

- the age and obsolescence of the property; and

- the population demographics in the area.

In a stock purchase, these decisions are left to the CEO of the business invested in.

For investors, real estate and stocks are long-term investments providing income and profits from inflation and appreciation based on investment fundamentals. Short term investors are called speculators as they are not deterred by fundamentals. They invest based on momentum they see in pricing trends for both real estate, as flippers, and in stock, as day traders.

The difference in the two sets of speculators is the stock market trader sees near instant results, and real estate requires maybe a year or two before resale reveals wins or losses in less volatile price changes than stock.

Real estate – values run with consumer inflation!

Homeownership is an easy investment choice for tenants considering a rather permanent residence. Factually, real estate is a store of wealth that has proven to be a decent hedge against inflation when held long-term.

Conversely, federally insured savings accounts rarely pay interest rates equal to the rate of consumer inflation, much less greater. However, homes are a relatively safe place to park money via a buildup in equity through mortgage principal reduction and long-term gains mostly controlled by consumer inflation levels. The owner’s risk of loss is covered by insurance, and a significant equity provides quick — not instant — liquidity for emergencies requiring cash.

Stock prices increased more rapidly than home prices in recent years. Thus, stocks bought and sold in the recent past have been a more profitable investment than real estate bought and sold during the same period.

However, given the crap-table-like instability of stock market investments, long-term investors prefer income-producing real estate for being:

- less volatile and, thus, less risky than the stock market when properly leveraged or free of mortgage debt;

- more likely to cover inflation and produce a higher annual return (through rental income) than interest received on bonds or a savings account; and

- a tangible source of increasing wealth and, thus, profit through property price appreciation during ownership due to the demographics of its location.

Another benefit of an income property investment is the easy predictability of rents.

Rental income receipts change with the local population’s income and density trends, whereas changes to the prices of stocks and real estate react to interest rates in the cost of borrowing and capitalization rates for setting asset values — and later prices.

Yet, operating expenses and costs of ownership go with a real estate investment, involving management of the rental income to cover carrying costs and expenses like:

- maintenance;

- property taxes;

- insurance premiums;

- locating and moving in tenants;

- mortgage debt carrying costs;

- acquisition costs; and

- the extremely high cost of selling.

Real estate investors are best served by committing to several years of ownership — a decade or two. As incomes (individual and rental) move upward in tandem with consumer inflation, property values increase in locations where population density and incomes are rising. Further, when the population grows and wages increase faster than the rate of inflation, property prices build wealth by moving beyond the rate of inflation, called property appreciation.

Thus, while rental income provides an annual rate of return on a property’s worth, the wealth in the property is itself recovered on resale – including price inflation and appreciation in the property’s value. With buyer purchasing power falling and a buyer market emerging, real estate owners will find the current home prices slipping until the recession period’s arrival of speculators who collectively stop the decline and increase home prices.

Scale of return

As liquid or illiquid assets; investments like stocks can be disposed of within minutes and cashed out or, like real estate, take months determining whether to sell, time on the market until a buyer is located, process the sale, and anticipate the likelihood for failure of a deal and then repeat the process.

As a physical asset, real estate is permanent, with loss of improvements covered by insurance while the owner may use it, rent it or maintain it vacant. A stock, as it is intangible, is a fractional share or stock participation which is always passive for investors and thus never involved. Except for occasional voting, the stockholder investor can in no way reach, use, manage the company, or spend their human capital to salvage the asset.

Both real estate and stocks are lender financed. Leveraging is borrowing to buy things such as real estate purchase-assist mortgages or stock purchase margin accounts. Mortgages in a period of dropping prices or lost income too often offer a slow death before a foreclosure sale, giving the investor time to raise cash to recapitalize their ownership. Other lender financed investments, as with margin accounts, present a fast death with very little notice or time to raise cash.

Small investors can only invest in stock while wealthy investors acquire both stocks and real estate investments. The stock market is fractionalized with hundreds, thousands, or millions of individual investors owning stock in a company. Real estate is individually owned or owned by pass-through entities like partnerships and LLCs comprised of a few wealthy investors. However, small investors can get into real estate via the stock market with an entity issuing stock called an REIT.

Reaping the rewards

Both markets and their investments have measures to evaluate each opportunity purchased. Whether investing in a type of ownership or variation on ownership such as group investments or tranches, both use reciprocal positions for analyzing value tied to the Net Operating Income (NOI) of the investment.

Stocks use a P/E factor called Price to Earnings ratio. Real estate uses the yardstick of a capitalization rate. A stock’s P/E of 33 is the mathematical equivalent of a parcel of real estate with a cap rate of 3% — not a particularly interesting annual return on investment for any investor.

PE ratios in the NY exchanges in August 2025 are around 29 PE average. The historic mean PE for the exchanges in recent decades coinciding with declining interest rates led to a PE of 19, which is a cap rate of 5%. Not at all what an investor in real estate will settle for.

All income types are reported for income tax purposes. Stocks are reported as portfolio category income and real estate income property reported as passive tax category investments (so long as the ownership is actively involved in management). Neither investment is considered trade or business category income or profits.

Related article:

{kind=link}

I appreciate your effort. Thankyou for sharing

well written content highly recommend that

Just amazing way of writing article highly recommend that content

There are so many blog i read right know but any one of them satisfy me but this one is so informative blog …

Crisp and a good read. Thanks for sharing!

A significant difference between Stock Market Investments is the investor’s focus. The stock market investor is focused on appreciation (capital gain) while the real estate investor is focused on current income (rents).

As a real estate investor I do not track the value of my properties. I do keep close track of the income. In a housing market decline rents are “sticky downward”. That is, they tend to decline slowly and usually only with a change in tenants. Unlike stocks, real estate investments are also usually leveraged offering greater potential return in the long run.

As a stock market investor I receive daily (even minute by minute) updates of value making fluctuations more apparent and stressful.

The stock market is more like gambling. Throwing your money down and hoping for a quick return. It is a curious situation since you are really buying an interest in a company. Virtually all companies seek to make current net income for their owners. But that does not seem to be the focus of stock market investors.

It is noted in this article that stock prices began their greater climb in the 1980’s and that the recent rise in values is largely due to cheap money. My question is, hasn’t there been a measurable change in the market based on the increased existence of individual retirement programs? There are only so many ways to invest a 401k. Most passive retirement plans will dump money into these markets every month whether the stock prices are up or down.

Thanks for sharing such a good and useful information