Why this matters: A mortgage loan originator (MLO) processing an SFR mortgage application pulls a credit report, advises the applicant of the credit agency’s score and any derogatory financial information which suggests adverse action on the application. Critical to approval, the applicant provides the MLO with explanations for the derogatory items so the MLO can process the application.

This process pits the mortgage applicant and the MLO against unverified and incomplete credit agency information about payment history. However, the basis for mortgage lending is the applicant’s present ability to pay and the value of real estate as security, not a score from a remote third party.

The consumer mortgage

A consumer mortgage is a debt:

- incurred primarily to fund personal, family or household purposes;

- secured by a parcel of real estate containing one-to-four residential units; and

- owner occupied or buyer to occupy.

Consumer mortgages are either:

- conventional mortgages; or

- government-related mortgages.

A conventional mortgage is any mortgage that is not made, insured or guaranteed by the federal government.

A government-related mortgage is a mortgage insured by the Federal Housing Administration (FHA), guaranteed by the U.S. Department of Veterans Affairs (VA) or guaranteed or funded by the U.S. Department of Agriculture (USDA).

The ability of a buyer or owner to obtain financing is an integral component of most real estate transactions, whether fee simple or leasehold.

The submission of a mortgage application to a private or institutional mortgage loan originator (MLO) is the catalyst setting the machinery of the regulated mortgage industry in motion to provide consistent and expected results as housing policy.

However, lenders rely heavily on credit scores to make their lending decisions, be it on a mortgage, a credit card or a car loan. Most buyers know they have a credit score, and its general use, but few consider the nuts and bolts behind the score — that is, until they apply for a mortgage and are denied or offered unfavorable terms.

Thus, understanding credit management and credit scores is intrinsic to an individual’s understanding about the likely availability of a mortgage.

Related article:

Credit report score, the past vs the present

An individual’s consumer credit score is a credit agency’s trailing indicator of the applicant’s probability to repay debt obligations. However, MLOs initially use the score, a single three-digit figure, as the sum for an individual’s debt payment history reported in an easy-to-apply number. The score is used like a gross rent multiplier (GRM) number is used to initially qualify an income property for acquisition.

The score, obtained in a third-party credit report, guides an MLO in their initial response to an application. For a homebuyer, their management of accurate credit information in a credit report on their financial behavior is critical to success when seeking a mortgage.

Using the information complied in a credit report, the MLO now starts a more thorough analysis of the risk of default the homebuyer presents when originating a mortgage to fund their purchase of a home.

A homebuyer’s mortgage application submitted to an MLO authorizes the MLO to pull the homebuyer’s credit report to assist the MLO to determine whether the applicant is apt to pay as agreed. [See RPI Form 302]

A FICO score is supplied by one of three credit reporting agencies (TransUnion, Experian and Equifax). An alternative credit score model developed by the three reporting agencies, called VantageScore, also produces an acceptable credit score. The report contains information about the payment history and credit standing of a buyer as viewed by the credit agency — the score.

A traditional FICO credit report guides an MLO in their review of the buyer’s past (trailing) performance for repaying debt obligations. The newer VantageScore claims to offer a more predictive model for how likely consumers are to repay their debts in the future. Debt reporting includes amounts of money owed, past and present, on:

- loans or financing agreements;

- judgments or tax liens; or

- retail and bank credit accounts.

The MLO is allowed to charge the buyer for the cost of the credit report.

Notably, neither the credit reporting agency nor the credit report assures, much less guarantees, the future performance by the buyer to make payments on the mortgage. For the MLO, the report content in no way addresses or provides evidence of the buyer’s ability to pay, the basis for repayment and qualification for mortgage default insurance (PMI/MIP).

The separate issue for an MLO of a household’s ability to make monthly payments on a mortgage debt is resolved by an income and net worth financial analysis performed by the MLO. The data needed is supplied in the mortgage application submitted to the MLO by the homebuyer or owner seeking the mortgage.

Ability to pay is confirmed by investigating an applicant’s employment status, income and assets. The MLO applies an income-to-payment ratio to set the maximum amount of mortgage funding available to the applicant. Generally, the ratio limits monthly mortgage payments to 1/3rd of the household’s gross income expectations.

This income-to-payment ratio is used by a buyer agent to approximate the mortgage funds likely available to the buyer-client to buy a home.

Related FARM Letter:

The credit score consequences in use

Most MLOs and landlords rely heavily on an individual’s credit score, most often the Fair Isaac Corporation (FICO) Score. This score is calculated by each of the three credit reporting agencies based on payment reports the agencies receive from banks, MLOs, credit card issuers and landlords.

The debt information received is primarily from institutional lenders, called traditional credit sources. However, landlords, employers, utilities and other non-traditional credit providers now also provide agencies with information since individuals with cash often do not borrow, carry no debt on their credit card which accrues interest, and have no bank-type credit history.

Credit reporting agencies are limited to three operators consisting of TransUnion, Experian and Equifax. As aggregators of debt behavior on individuals, these agencies collect and condense the information they receive into a score. Each agency independently calculates the score they issue on an individual from the data they have compiled.

Although FICO scores are the most common credit rating system used for mortgage underwriting, Fannie Mae and Freddie Mac (Government-Sponsored Enterprises) have recently accepted an alternative rating system, VantageScore.

VantageScore uses a smaller amount of credit history to generate a score based on a predictive model. It was developed by the three main credit reporting bureaus (Equifax, Experian and TransUnion).

Related article:

A FICO generated credit score is based on the individual’s installment debt payment behavior and consists of:

- 35% payment history;

- 30% amounts owed;

- 15% length of credit history;

- 10% new credit opened; and

- 10% type of credit used.

The range of FICO credit scores among the agencies are from a low of 300 to a high of 850. Generally, MLOs rank credit scores by tiers of probability for debt performance, such as:

- poor when they are below 580;

- fair when they are between 580-669;

- good when they are between 670-739;

- very good when they are between 740-799; and

- excellent when they are 800 and higher.

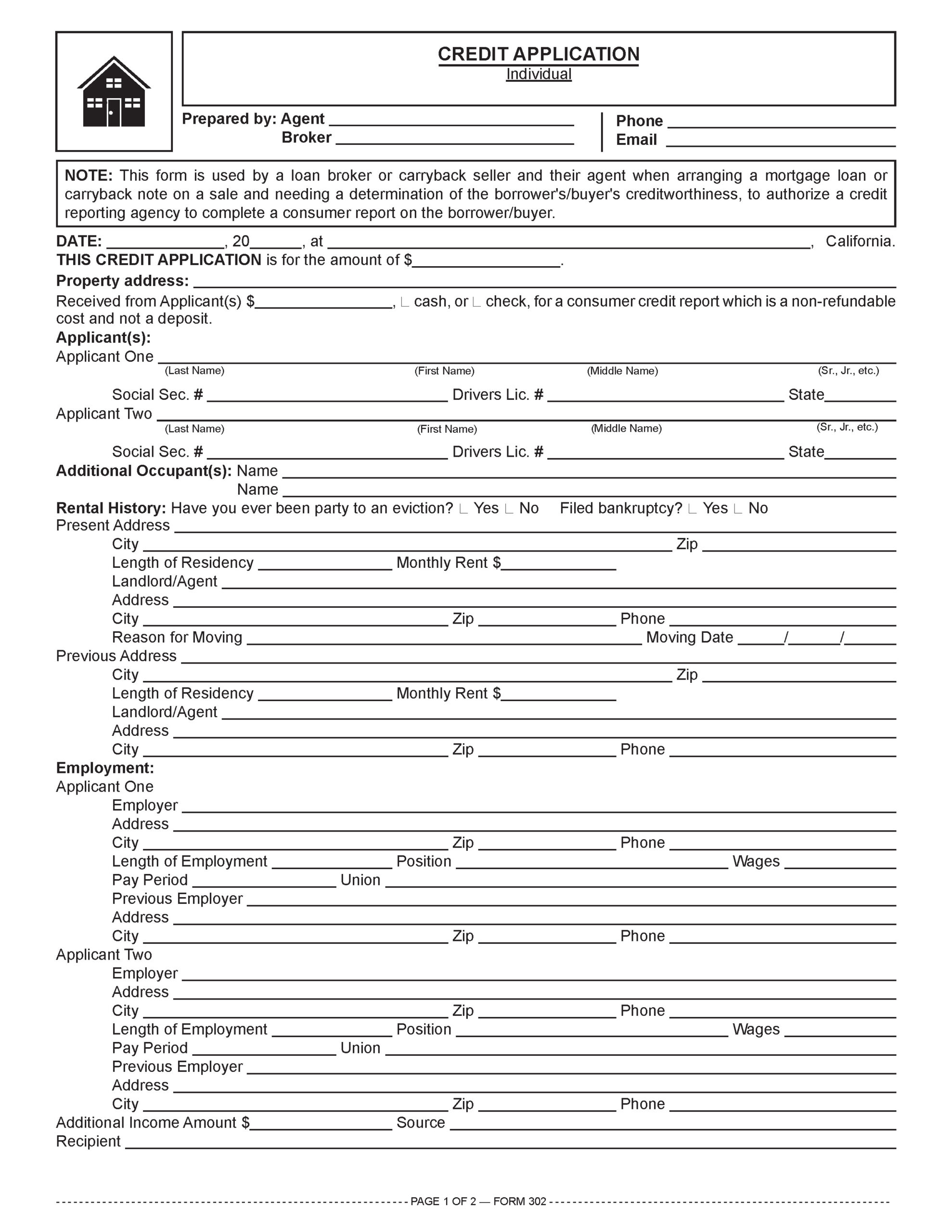

Critical to applicants for a mortgage, an MLO discloses to the applicant their credit score and key debt information adversely affected their credit score. The MLO credit data is presented to the applicant by using a form called the Credit Score Disclosure Exception Notice. [See RPI Form 217]

Related FARM Letter:

FARM: About those free credit reports for your annual review

Mortgage-related credit reports

The consumer credit report pulled by an MLO or carryback seller to finance $150,000 or more on the purchase of a home contains more trailing payment information than a tenant screening report used by landlords, including:

- bankruptcies predating the report by no more than ten years. Chapter 13 bankruptcies stay on file for seven years, but Chapter 7 bankruptcies remain for ten years;

- civil suits and judgments, and records of arrest predating the report by no more than seven years;

- paid tax liens predating the report by no more than seven years;

- accounts placed for collection or charged off as a loss predating the report by no more than seven years; and

- records of criminal activity predating the report by no more than seven years; and

- foreclosures remaining on the record for seven years.

Foreclosures negatively impact a score between 85-160 points.

Bankruptcies reduce a score by about 130-240 points.

30-day mortgage delinquencies reduce a credit score between 60-110 points, and the impact is higher for 60- and 90-day delinquencies.

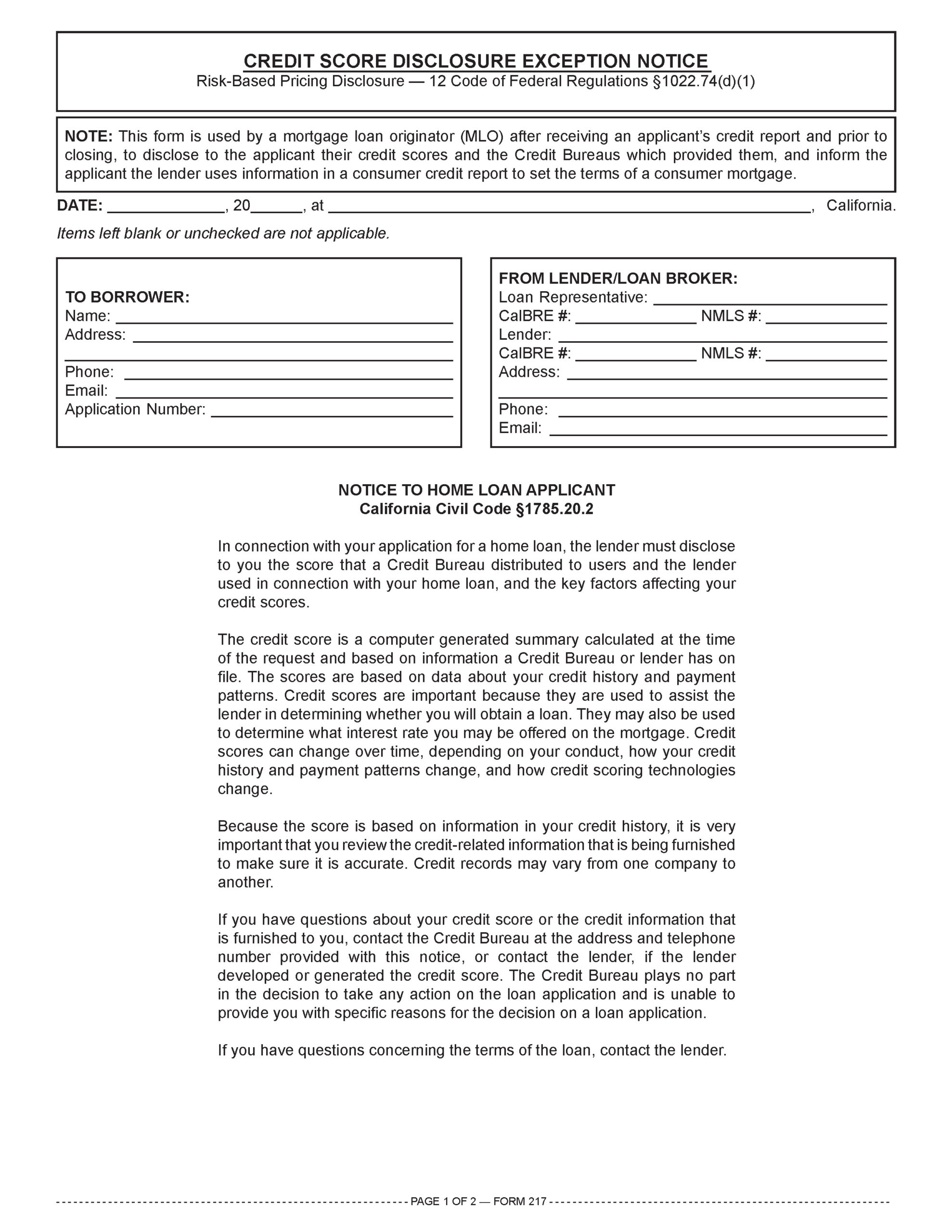

An MLO informs a mortgage applicant that their credit score affects their qualification for a mortgage by using a form called the Notice to Home Loan Applicant. [See RPI Form 217-1]

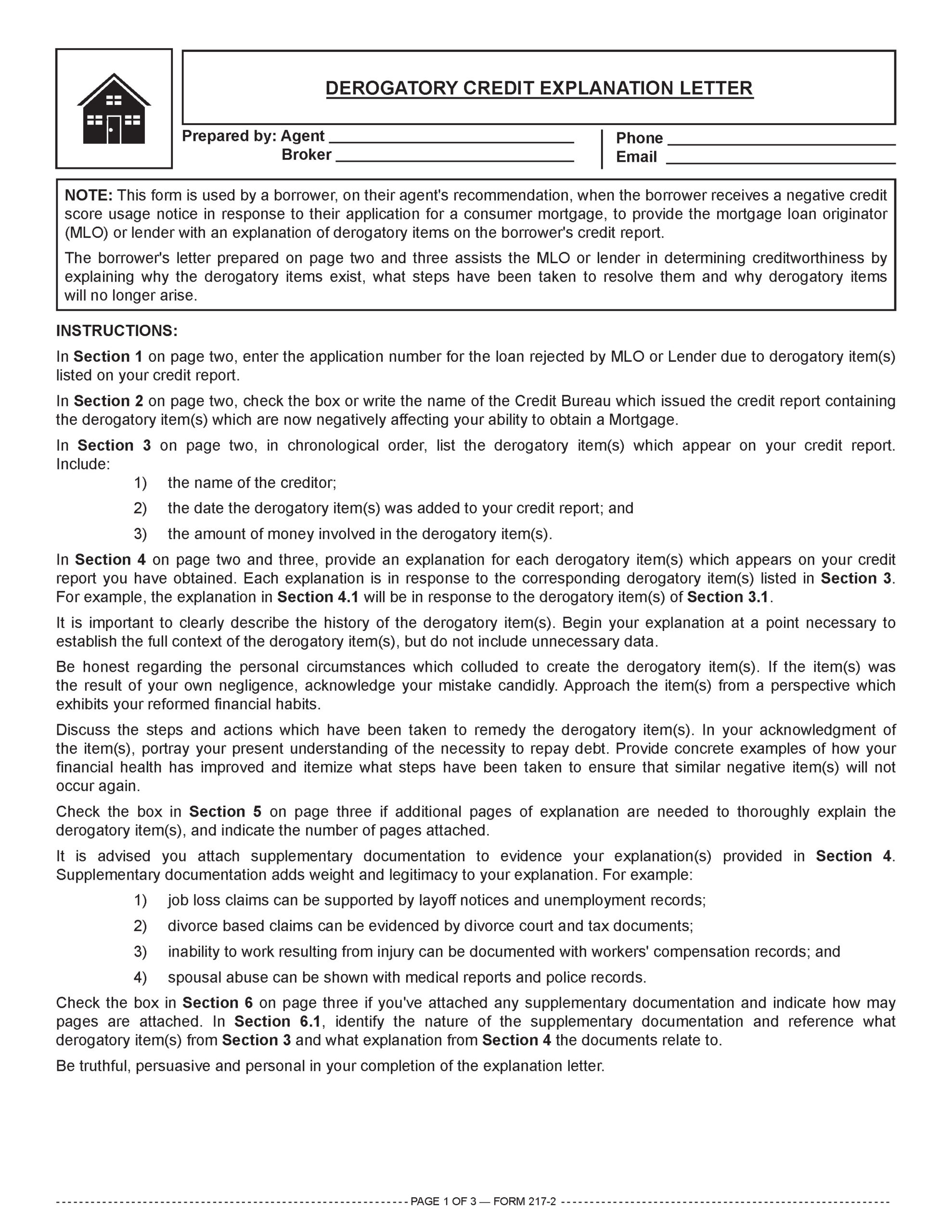

A mortgage applicant might also have negative items on their credit report which need addressing by the applicant. Here, the applicant, with the help of their agent, submits a form called a Derogatory Credit Explanation Letter to their MLO. Through the form letter, the applicant explains why the derogatory items exist and provides reasons for the hardship that interfered with payment of the items. [See RPI Form 217-2]

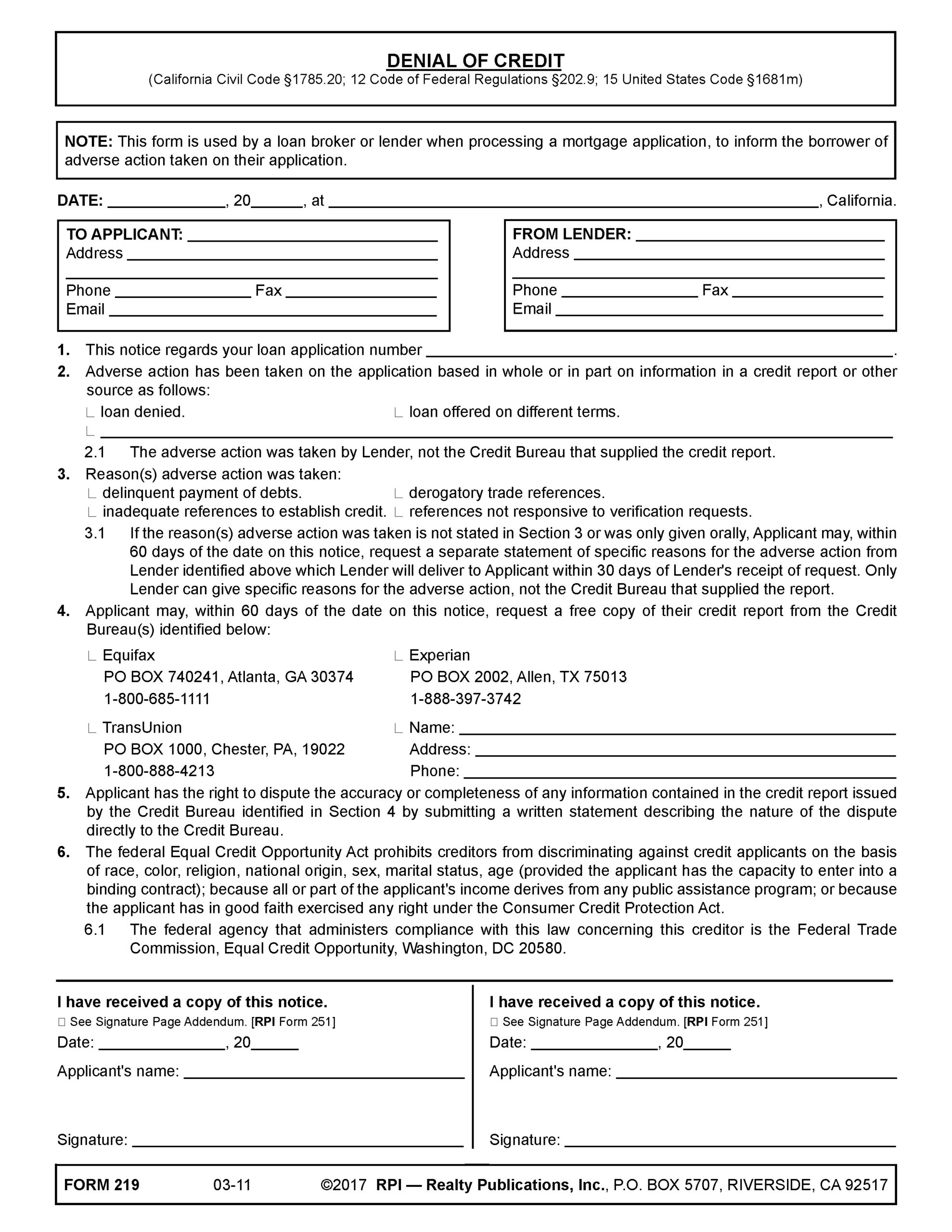

When the MLO denies the applicant’s mortgage application, or offers the mortgage on different terms, the MLO uses a form called the Denial of Credit. [See RPI Form 219]

Related article:

What buyer- and tenant-clients need to know about credit reports

Analyzing a credit application, a process

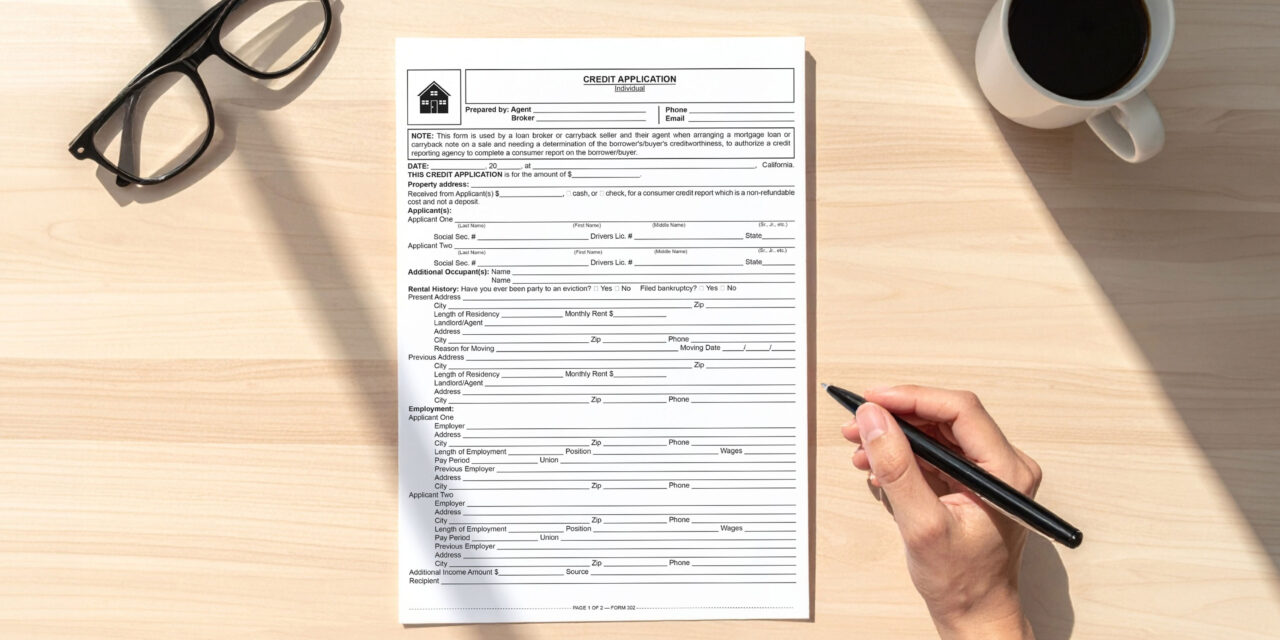

An MLO or carryback seller and their agent uses the Credit Application — Individual published by Realty Publications, Inc. (RPI) to initiate the process of arranging a mortgage loan or carryback note on a buyer’s purchase of a property. It authorizes the MLO or carryback seller to order and receive a consumer credit report on the buyer from an agency. [See RPI Form 302]

The Credit Application — Individual contains provisions addressing:

- the cost of obtaining the credit report;

- the address of the real estate securing the mortgage debt;

- the applicant(s)’ name, social security number and driver’s license number;

- additional occupants of the mortgaged real estate;

- rental history information, including evictions, bankruptcies, present and previous addresses, city and ZIP code, monthly rent amount, landlord’s name and address, reason for moving and moving date;

- the employers of the applicants, address, city, phone number, length of employment, position, wages, pay period, union, previous employer, address, and phone number;

- any additional income amount, source and of which applicant;

- automobile and bank information;

- credit and personal references and nearest relative; and

- signatures of the applicant(s) and MLO or carryback seller. [See RPI Form 302]

With this information from the applicant, the MLO determine the buyer’s ability to pay the mortgage as agreed — creditworthiness.

Analyzing disclosure of the credit score

An MLO on their receipt of an applicant’s credit report uses the Credit Score Disclosure Exception Notice published by RPI to disclose to the applicant their credit scores and the Credit Bureaus which provided them. Also, the form advises the applicant the MLO uses information in a consumer credit report to set the terms of a consumer mortgage. [See RPI Form 217]

The Credit Score Disclosure Exception Notice contains:

- the date, applicant’s information and MLO’s information;

- the loan number used for the application [See RPI Form 217 §1];

- the applicant’s credit score [See RPI Form 217 §2];

- the credit bureaus that issued the credit report [See RPI Form 217 §3];

- the date the credit report was generated [See RPI Form 217 §4];

- the lowest and highest a credit score ranges (300 to 850) [See RPI Form 217 §5];

- credit score percentile compared to U.S. consumers [See RPI Form 217 §6];

- key debt items that adversely affected the applicant’s credit score in order of significance [See RPI Form 217 §7];

- boilerplate information relating to the credit report for the applicant [See RPI Form 217 §§8 through 11]; and

- signatures of the applicant(s), confirming they received a copy. [See RPI Form 217]

The notice to home loan applicant analysis

An MLO uses the Notice to Home Loan Applicant form published by RPI as soon as practicable (ASAP) after the MLO pulls the applicant’s credit report. The form advises the applicant of the MLO’s obligation to inform the applicant of their credit scores and information, and the Credit Bureaus providing the scores and information. [See RPI Form 217-1]

The Notice to Home Loan Applicant contains:

- the date, applicant’s information and MLO information;

- boilerplate information relating to the applicant’s credit score;

- which credit bureau issued the credit report; and

- signatures of the applicant(s), confirming they received a copy of the notice. [See RPI Form 217-1]

The denial of credit form analysis

An MLO uses the Denial of Credit form published by RPI when processing a mortgage application to inform the applicant of the MLO’s adverse action taken on their application. [See RPI Form 219]

The Denial of Credit contains:

- the date, applicant’s information and MLO information;

- the loan application number involved [See RPI Form 219 §1];

- the adverse action taken by the MLO on the application, including:

- mortgage denied;

- mortgage offered on different terms; or

- other action (blank) [See RPI Form 219 §2];

- reason(s) the adverse action was taken, including:

- delinquent payment of debts;

- inadequate references to establish credit;

- derogatory trade references; or

- references not responsive to verification requests [See RPI Form 219 §3];

- advising the applicant that they may request a free copy of their credit report from the identified credit bureaus [See RPI Form 219 §4];

- boilerplate information for the applicant’s response, such as the right to dispute inaccuracies and a discrimination notice [See RPI Form 219 §§5 and 6]; and

- signatures of the applicant(s), confirming they received a copy.

The derogatory credit explanation letter analysis

An applicant, on their buyer agent’s recommendation, uses the Derogatory Credit Explanation Letter published by RPI when the applicant receives a negative credit score notice from the MLO. The form is used by the applicant to provide the MLO with an explanation of derogatory items on the applicant’s credit report. [See RPI Form 217-2]

The applicant’s letter assists the MLO in determining creditworthiness by explaining why the derogatory items exist, what steps have been taken to resolve them and why derogatory items will no longer arise. [See RPI Form 217-2]

The Derogatory Credit Explanation Letter contains:

- instructions for the applicant to fill out the form;

- MLO and applicant information;

- the MLO mortgage application number involved [See RPI Form 217-2 §1];

- the credit bureau that issued the report [See RPI Form 217-2 §2];

- derogatory item(s) listed on the credit report [See RPI Form 217-2 §3];

- explanations for the derogatory items listed on the report [See RPI Form 217-2 §4];

- additional pages that may be attached to fully explain the derogatory items [See RPI Form 217-2 §5];

- attached supplementary documentation evidencing explanations [See RPI Form 217-2 §6];

- descriptions of the supplementary documentation, and which derogatory item and explanation it relates to [See RPI Form 217-2 §6.1]; and

- signature of the applicant(s). [See RPI Form 217-2]

Related article:

The votes are in: Clients don’t pull their credit report before mortgage pre-approval

{kind=link}