Today’s volatile relationship between incomes and home prices is ripe for a correction.

The median income of households headed by married couples in California rose 4.2% in 2016, according to recently released Census data. However, home prices continue to rise at a much faster pace.

In 2017, average California home prices rose 8.5% over a year earlier, higher than the 6.6% annual rise in 2016.

Home prices are intrinsically tied to homebuyer incomes. After years of excessive price increases, home prices are set to fall back in line with incomes, and soon. The pull of slow sales volume, rising interest rates and talk of a coming recession are expected to cause home prices to fall in 2019.

[infogram id=”married-household-income-vs-prices-1h7j4d1r8ryd4nr” prefix=”gXB”]Chart update 07-30-18

| 2016 | 2015 | Annual change | |

| CA median married household income | $93,776 | $90,031 | +4.2% |

| CA tri-city home price index | 245.2 | 230.1 | +6.6% |

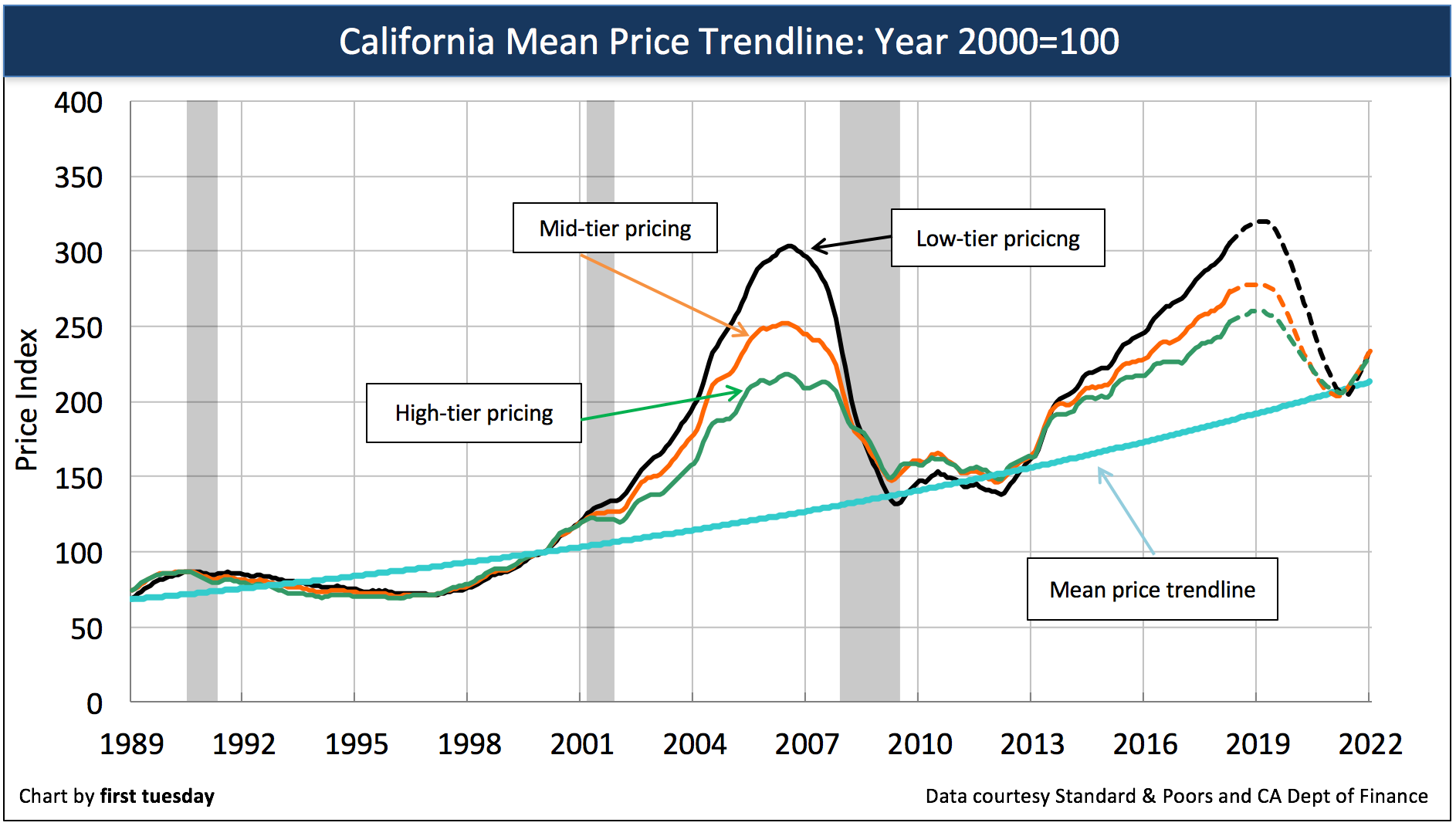

The chart above is a snapshot of the real estate cycle.

This most recent cycle we are emerging from in 2018 has its roots in the early 2000s, when home values began outpacing incomes at a rapid pace.

In 2006, home prices peaked in step with the Millennium Boom. By that time, home sales volume was already falling as buyers sensed prices were too high to continue during the inevitable recession, which arrived in 2008. From 2006 to 2007, prices dropped 16%, followed by a further 26% in the following year.

All in all, California home prices fell 44% from their 2006 peak to their bottom in 2009.

In some ways, this steep fall was a correction to all the excess experienced in the housing market during the early- and mid-2000s. In another sense, the fall was simply the market’s way of bringing home prices back in line with incomes.

There is a name for this reliable force that pulls home prices toward incomes: the mean price trendline.

The mean price trendline for real estate

Through the volatility of housing booms and busts, price increases continue to return to the same rate of annual income change, related to the consumer price inflation (CPI), which is typically 2%-3% per year. In California, this mean price change is closer to 3.5% annually over the past several decades.

How does income impact home prices?

Quite simply, home values can only go as high as incomes allow.

Homebuyers reliant on financing are limited to a maximum mortgage payment of 31% of their monthly income. This translates to the ability to purchase a home costing roughly five times their annual income.

Still, there is some wiggle room in the equation. After incomes, interest rates have the next biggest impact on home prices. When interest rates are falling — as occurred in the 2000s — buyer purchasing power is extended, as homebuyers’ mortgage payments go further. When interest rates rise — as is occurring in 2018 — buyer purchasing power falls and homebuyers are limited to paying less with the same income.

During housing bubbles, home prices become temporarily untethered from this rule and the mean price trendline. During the bust that follows the boom, prices fall, returning once again to the trendline.

2018 is primed for the next downturn

Here’s how the situation stands in mid-2018:

- home prices are roughly 9% above a year earlier;

- home sales volume is 1% above a year earlier (basically flat);

- interest rates are nearly a full percentage point higher than a year earlier, translating to a 7% reduction in purchasing power for the average California homebuyer.

Further, the Federal Reserve (the Fed) plans to continue their efforts to increase interest rates in an effort to cool down the economy and induce a moderate business recession by 2020. Not only do higher interest rates discourage potential homebuyers from entering the market, but they cause homebuyers to offer less when they make an offer to purchase.

Related article:

In response, first tuesday expects home prices to fall by mid-2019, bottoming once they hit the mean price trendline around 2020. Meanwhile, incomes will continue along at their current measured pace, pausing briefly in 2020-2021 in response to the recession.

{kind=link}

I have to wonder how many people will do their taxes in 2019 and realize their home is not giving them any tax incentive to remain an owner. The new tax law standard deduction will have an affect, the question is how much of an affect? Just one piece of the puzzle but if someone bought a house thinking that one of the reasons to buy (versus rent) was to save $$ on taxes then they are going to have to reevaluate. If they have equity and they lose one of the reasons they bought the property they may decide it is time to cash in. A large amount of properties for sale may hit the market spring 2019