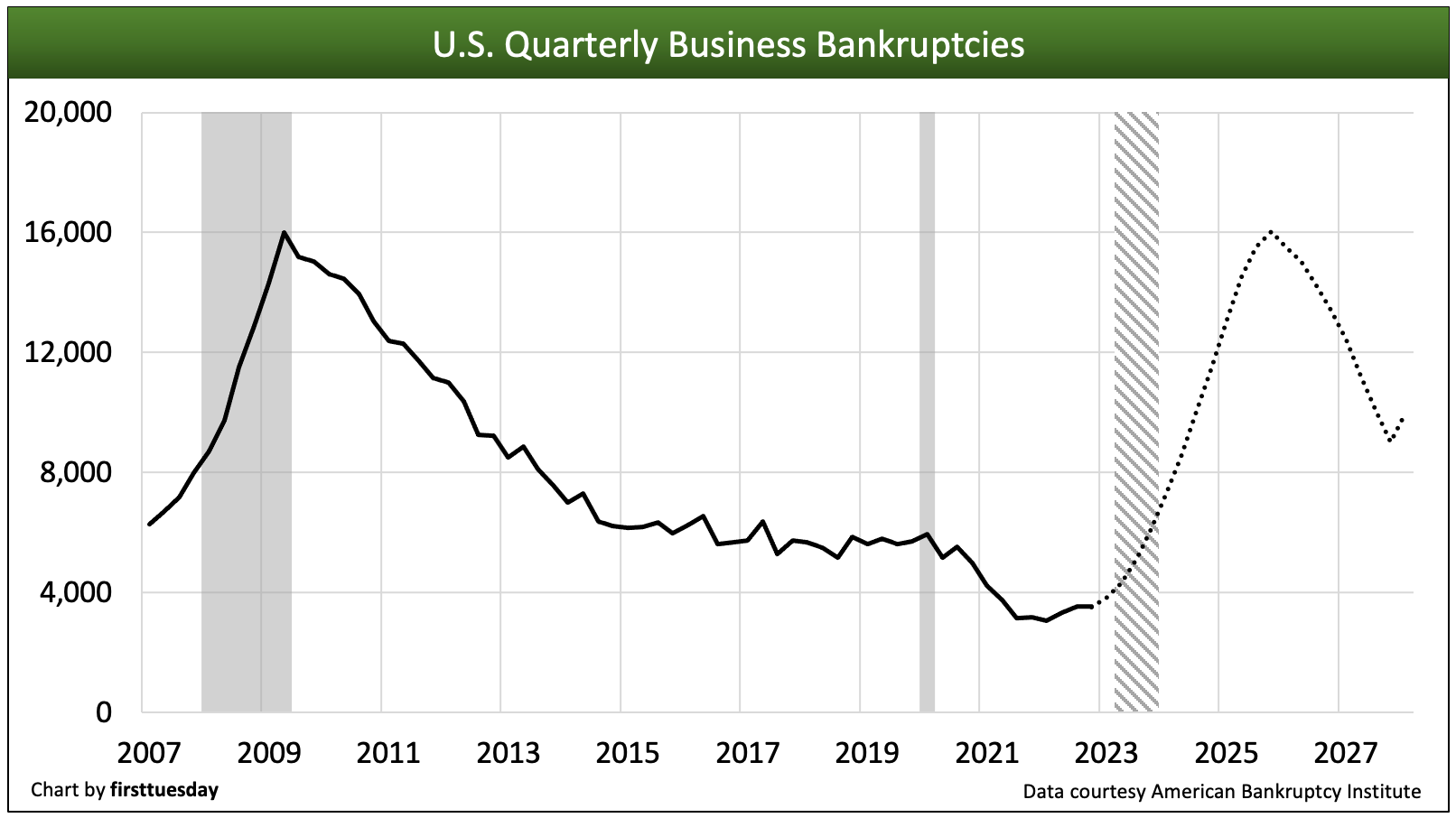

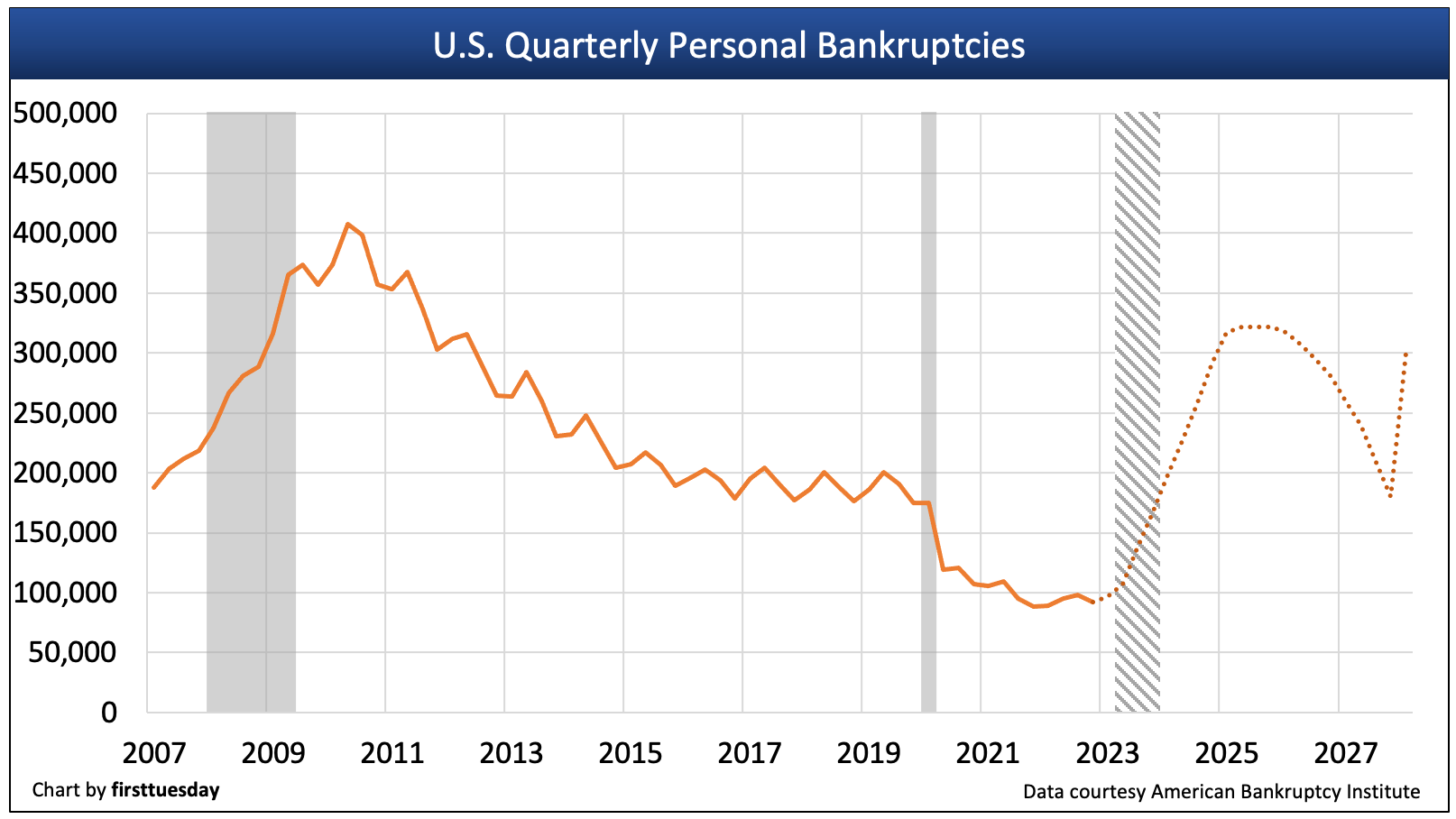

Bankruptcy filings began to inch higher during 2022, with 91,900 personal bankruptcies and 3,500 business bankruptcies filed nationwide in Q4 2022. Further, bankruptcies continue to increase in the first half of 2022, currently up 17% from a year earlier when filings were near a decades’ low.

With a below average filing share, California represents approximately 9% of the national filings versus 13% of the population.

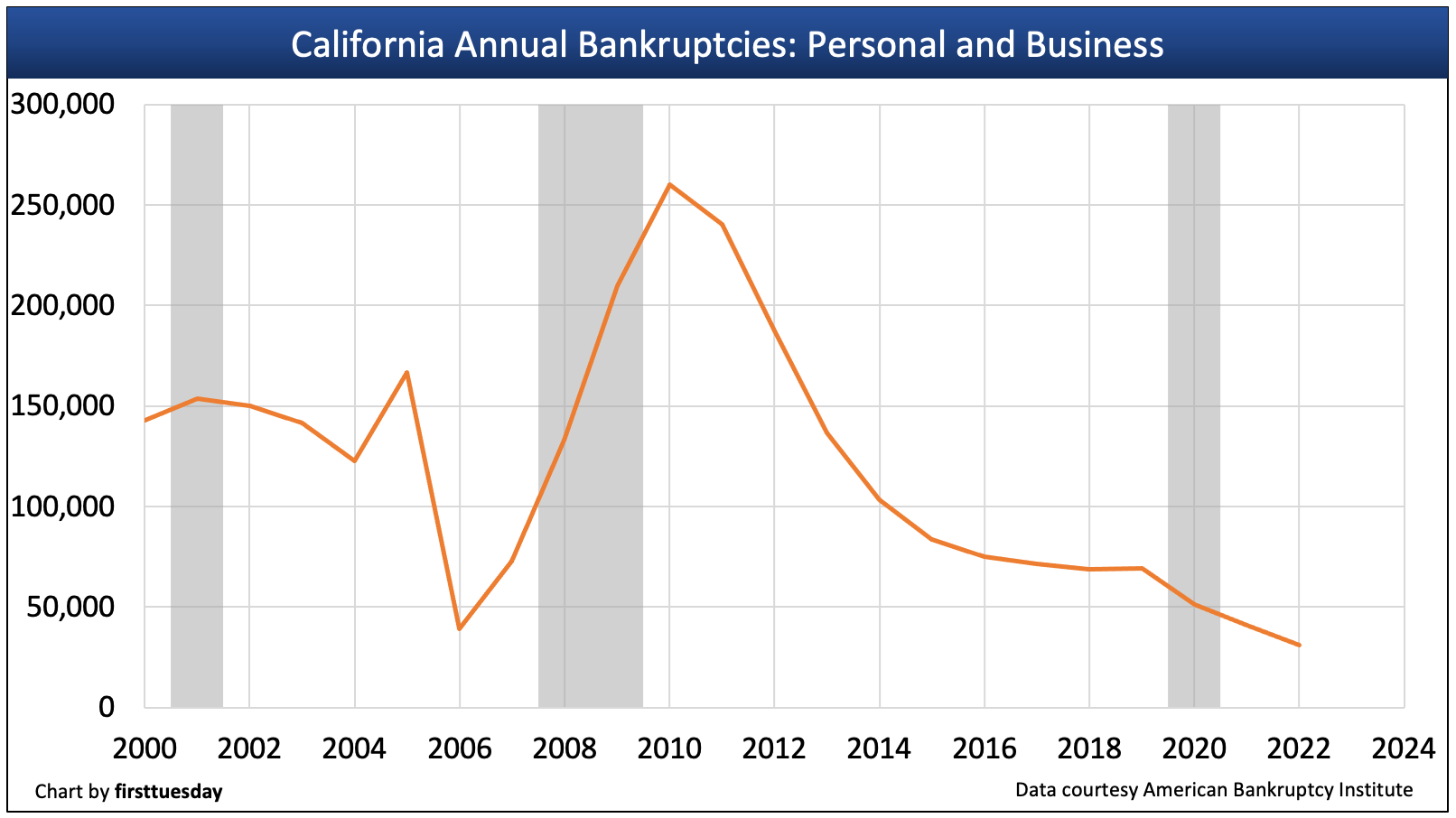

Bankruptcies plummeted during the 2020-2021 pandemic period, despite the onset of the 2020 recession. Without pandemic interference, bankruptcies would have risen significantly, as in any recession. Businesses which otherwise would have folded found fuel in economic stimulus and rising inflation generated by the pandemic. Just 6,100 business bankruptcies were filed in California during 2021, a fraction of the 63,200 filings that were recorded during the 2011 peak of the 2008 recession. In 2022, this number increased to 6,800 business bankruptcies.

When it comes to recessions, bankruptcy numbers tend to be a lagging indicator. That is, many businesses hold on until they run out of cash, bleeding off market share as disruptors to a recovery while they exist as zombie businesses. Eventually they give in to market forces and throw in the towel. Compared to businesses, bankruptcy offers few benefits for individuals, though bankruptcy proceedings extend the foreclosure process by several months.

In 2023, the economy is rapidly contracting as the curtain opens on the second act of the 2020 recession. In 2020-2021, government stimulus bridged the pandemic gap for most individuals and businesses lacking the financial foundation to weather a recession — hence the artificially low bankruptcy numbers resulting in a buildup of bankruptcy candidates. But with the effects of stimulus now in the rearview, the recession — expected to officially arrive in the second half of 2023 — will deliver the killing blow for those lacking sufficient cash reserves or equity. The result will be a cyclically disproportionate rise in bankruptcy filings in the next three years.

For the housing market, the reduction in home sales volume which began dramatically in 2022 paced by rapidly doubling interest rates will see home values fall to wipe out the past four+ years of home price increases. Homeowners who see their home values diminish are more likely to go bankrupt when household financial stress occurs. As the struggle for ascertaining home values takes root and buyers simply wait for prices to bottom and hold, expect more personal and business bankruptcies to occur, expected to peak around 2026.

Updated May 3, 2023. Original copy released January 2010.

Chart update 05/03/23

Chart update 05/03/23

| Q4 2022 | Q4 2021 | Q4 2020 | |

| Personal Bankruptcies | 91,900 | 88,300 | 107,400 |

| Business Bankruptcies | 3,500 | 3,200 | 5,000 |

Dashed lines are firsttuesday’s forecast. The number of bankruptcy filings has decreased each year since the end of the Great Recession. By the end of 2014, personal bankruptcy levels had fallen below the average levels seen during the 1990s and early 2000s, where they remain today. California districts with the highest number of bankruptcy filings in 2021 were:

- Central California, with 20,300 personal bankruptcies and 2,800 business filings;

- Los Angeles, with 8,500 personal bankruptcies and 3,300 business filings; and

- Riverside, with 6,000 personal bankruptcies and 700 business filings.

The majority of these personal bankruptcy filings were completed through Chapter 7.

Chart update 05/03/23

Chart update 05/03/23

Two forms of bankruptcy

Two separate bankruptcy procedures exist, both governed by federal law.

Chapter 7 bankruptcy requires the insolvent homeowner in bankruptcy to repay their debt from whatever assets they possess, unless those assets are lower than state-allowed levels of assets and income. In Chapter 7 bankruptcy, a home without equity is counted among these assets, and foreclosed upon.

Chapter 13 bankruptcy, on the other hand, requires the homeowner to repay their delinquent debts over a longer period of time than contracted for, after deducting reasonable living expenses.

The Chapter 13 repayment plan can include the homesteaded sale of the owner’s home, if the home has any equity in the home. Bankruptcy law no longer permits a homeowner’s mortgage to be reduced by a bankruptcy court (a cramdown, or principal reduction). However, Chapter 7 bankruptcy voids any deficiency obligations on recourse mortgage refinancing, just as it voids all unsecured debt with a value exceeding the amount of the homeowner’s nonexempt assets.

In addition to putting an immediate stop to lender collection efforts, the process of filing bankruptcy allows a homeowner to pay delinquent mortgage payments over a three-to-five year period. Troubled homeowners often choose to file Chapter 13 Bankruptcy to discharge their non-mortgage (unsecured) personal debts, and then use the newly freed funds to make future payments on their mortgages.

Homestead exemption protections

Bankruptcy laws do enforce California homesteads. For positive equity homeowners, this exemption acts as an incentive to file bankruptcy to avoid unsecured debts and free up cash by making it available under the homestead.

On the other hand, the homestead exemption has no effect on the priority or payment of an owner’s mortgage. The bankruptcy process adversely affects lenders who have obtained involuntary liens (judgment liens) against the homeowner’s title.

In 2021, California homeowners qualify for a net equity homestead protection of:

- up to $300,000; or

- the median sale price for a single family residence (SFR) in the homeowner’s county in the calendar year prior to the year in which they claim the exemption, not to exceed $600,000 (adjusted annually for inflation). [CCP §704.730]

Related article:

California’s homestead exemption falls short of full protection for homeowners

Bankruptcy and foreclosure

The most important aspect of bankruptcy, from the point of view of mortgage lenders, is the “automatic stay” provision. This provision of bankruptcy law also delivers the most direct and immediate results for troubled homeowners. Any owner who files bankruptcy immediately places an automatic stay on all collection efforts, including foreclosure sales.

Lenders prefer to quickly move to a foreclosure sale, take title to the property or what proceeds they can and cut their losses, and are thus hamstrung by the automatic stay provision. They are forced to wait until a bankruptcy court allows them to proceed. The stay provision increases the lender’s costs of dealing with a homeowner who does not maintain their mortgage payments while in bankruptcy.

On average, filing Chapter 7 bankruptcy extends the foreclosure process from six months to a year. Chapter 13 delays the foreclosure sale even longer, often drawing it out to a year and a half. A homeowner who files bankruptcy without the ability to make payments on their mortgage merely extends the time before the eventual foreclosure sale. For the lender, the bankruptcy process increases the risk the home will be damaged or otherwise devalued before the sale takes place, increasing the lender’s eventual loss.

Lenders thus have a vested interest in government regulations that make it difficult for homeowners to obtain relief on their mortgages in bankruptcy, and they intend to keep their hard fought gain of a cramdown-free bankruptcy law intact. Lenders don’t want the threat of a bankruptcy judge endowed with the power to reset the loan balance at exactly the amount the security for the loan is worth (which, of course, is all the lender can expect to get from foreclosure anyway).

When bankruptcy is unavoidable, lenders want to get out of bankruptcy court as quickly as possible. Often they can be persuaded to agree to a short sale in order to hasten the process and cut their losses. Bankruptcy can thus be an effective way for homeowners to force the lender’s hand.

Costs and benefits of bankruptcy

So does filing bankruptcy, and thereby discharging unsecured debt and putting off a potential foreclosure sale, actually help homeowners pay their mortgages, or do the other costs of bankruptcy cancel out the benefits?

Evidence is mixed, but homeowners and their attorneys certainly seem to believe that bankruptcy can be beneficial. Troubled homeowners already make up the majority of those who file for Chapter 13 bankruptcy (studies in other states found that over 80% of filers were paying for homes with a loan to value ratio (LTV) over 90%).

Of the total number of homeowners who file bankruptcy, only about 33% successfully kept their homes, according to the Federal Reserve Bank of Philadelphia. It is certain that bankruptcy does, at least on occasion, have a positive effect for those desperate homeowners who turn to it as a last resort, and it is also sure that bankruptcy will almost always have a negative effect for lenders.

Equally important, homeowners who file for bankruptcy will find later that their past bankruptcy interferes with their future ability to qualify for mortgage financing.

{kind=link}

The information is very useful. I have a reseach relate to.

It’s interesting that you mention that filing for Chapter 13 bankruptcy can help you save your house from foreclosure. I have been falling behind on my mortgage payments for several months due to an injury that prevents me from working, so I’m considering seeking the services of a bankruptcy attorney. I’m going to search for a good bankruptcy attorney in my area to use.

“Over the past few decades, Prop 13 has accomplished this — and more — at the expense of new homeowners and renters.

Some of the negative effects spread by Prop 13 include:

• reduced sales volume, as current homeowners are incentivized to stay in their current home to keep their low tax rate;

• * new homebuyers — typically young families with less wealth than their more established neighbors — pay higher tax rates than their neighbors, who benefit from the same government services their property taxes support.”

*New homebuyers may be paying higher property taxes than their neighbors, but they too are protected from spiraling out control property tax increases. This seems to be a poor argument.

“Of the total number of homeowners who file bankruptcy, only about 33% successfully kept their homes. It is certain that bankruptcy does, at least on occasion, have a positive effect” One out od three keep their homes! That’s not “On Occasion”, it’s pretty good odds! Get a grip!