As mortgage rates jump, are homebuyers beginning to cancel escrows based on increased interest rates?

- No, transactions are not being canceled. (66%, 46 Votes)

- Yes, transactions are being canceled. (34%, 24 Votes)

Total Voters: 70

After years of stimulus injections and Federal Reserve (Fed) support, the government is taking off the training wheels in 2022 — and market participants are getting ready by demanding higher interest rates on their investments.

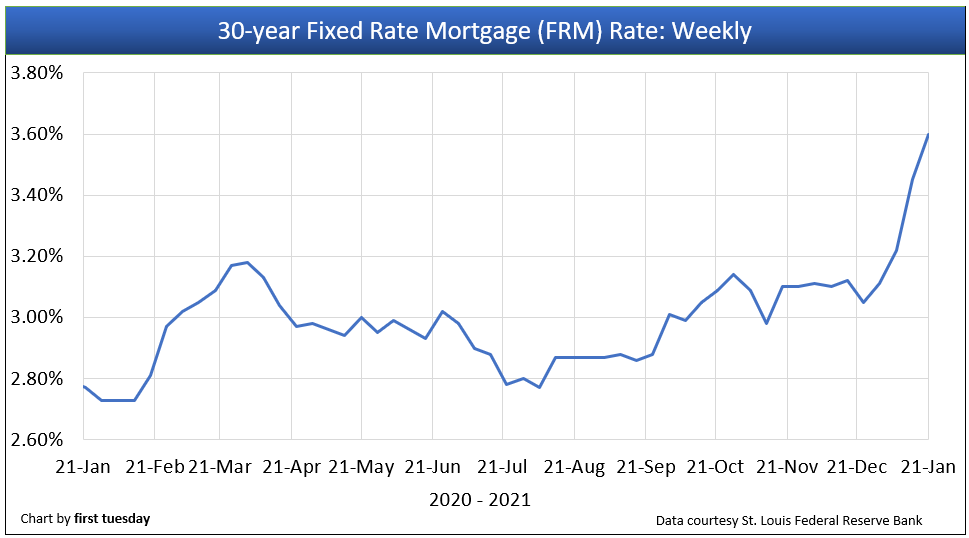

Mortgage interest rates hit bottom a year ago, in January 2021. Since then, rates have remained near historical lows — until their recent leap in January 2022. This increase has occurred in anticipation of the Fed’s bump to their benchmark rate, expected to happen in March 2022, according to the most recent Federal Open Market Committee (FOMC) statement.

This chart shows the average weekly interest rate on a 30-year fixed rate mortgage (FRM) over the past 12 months. The 30-year FRM rate recently peaked at 3.56% in the last week of January 2022. This is nearly a full percentage point higher than the bottom reached in January 2021, when the 30-year FRM averaged just 2.65%.

This interest rate leap translates directly to decreased money available to homebuyers and refinancers. Termed buyer purchasing power, the average amount of money available to homebuyers has fallen a whopping 13.5% over the past year due to interest rate increases alone. Absent an increase in pay or savings, this declining buyer purchasing power figure means homebuyers qualify for 13.5% less mortgage money today than they did a year ago.

The impact on home prices and sales volume is imminent. With less mortgage money available, and without sacrificing on their home search, buyers reliant on financing are able to pay less money for the same house. Those unwilling to settle for less will simply delay their homebuying plans while they wait for prices to fall in-line with their finances. Others will shoot their shot, offering less and less as interest rates continue to rise in the coming months.

Lacking the support of falling interest rates, additional stimulus or income boosts, California home prices are expected to fall back in 2022. Home prices will be further checked by the additional inventory anticipated to arrive in 2022 following the 2021 expiration of the foreclosure moratorium and rise in forbearance exits.

Related article:

Press Release: Q4 2021 Buyer Purchasing Power goes negative with rising interest rates

Those already under a purchase contract are finding today’s rate jump even more problematic. Unless they signed a rate lock with a lender, financed homebuyers are finding themselves unable to qualify to purchase at today’s higher rates.

Competing in today’s tight inventory/high demand market, homebuyers are already stretched to their limits. However, buyers unable to qualify at today’s higher rates due to exceeding debt-to-income (DTI) ratio limits may be able to “buy down” or reduce the interest rate — when they have extra cash on hand.

In financing situations where a rate lock is not present and buyers lack the ability to buy down the rate, sellers will find themselves suddenly absent a homebuyer — unless they are willing to compromise on price to save the deal. This leaves sellers with less cash on hand following the sale, and the domino effect for future sales continues as rates rise and prices decline.

The long-term outlook for buyer purchasing power is a decades’ long period of descent as mortgage rates continue to rise with the economic recovery, likely to gain strength around 2024. Rising rates will also bring downward pressure on the broader economy, slowing growth and wage increases across the board, leaving the economy more susceptible to frequent recessions — though not of the monster variety experienced in 2008 when rates were declining.

Thus, sellers can expect downward pressure on home prices to continue in the years ahead. Without the support of a full jobs recovery, home prices will remain tenuous in 2022-2023.

{kind=link}

Page and would appreciate it if you could provide me with the most recent news. Additionally, please upload the most recent articles for our continuous reading.

Thank you for being willing to tell us what you know. Because I know you care about us, we will always be grateful for everything you’ve done here.

Thanks for the article. Another summer is coming and I reopened your article to read

I learned a lot from your blog, and you can learn more about older video games to have more engaging experiences. I look forward to playing with you in the past!