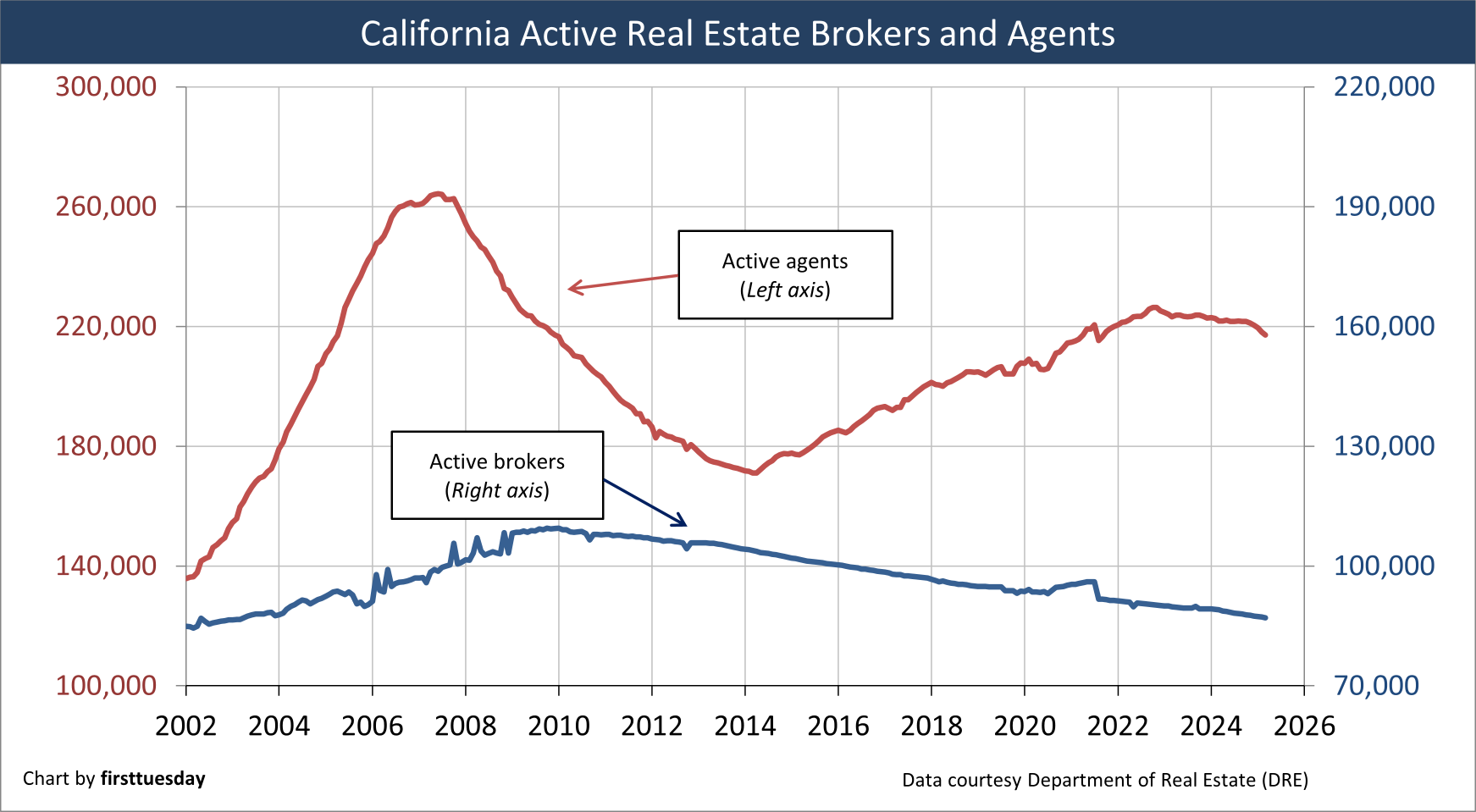

In March 2025, California had 87,062 active real estate brokers, about 2,000 fewer than one year earlier. Today, the number of active brokers continues to decrease, in search of a bottom since declining from the January 2010 peak of 109,500.

Conversely, the number of active sales agents steadily climbed from a 2014 low of 171,100 to a November 2022 peak of 226,300. As of March 2025, active agent numbers tapered to 217,400.

firsttuesday forecasts a dramatic fallback in sales agent licensing and renewals in 2025-2026. The decline is the result of the 2021 pandemic surge in new licensees and reduced present and future sales and leasing activity and branch office operations by employing brokers.

Watch for the next big wave of licensees — first with the return of speculators, then end-user homebuyers — to propel the housing market into its next expansion, beginning around 2028.

Updated May 5, 2025.

Chart update 05/05/25

| Mar 2025 | Mar 2024 | Annual change | |

| Active Agents | 217,125 | 221,857 | 2.13% |

| Active Brokers | 87,062 | 89,023 | -2.2% |

Today’s inflated agent-to-broker ratio

In a stable market, a natural equilibrium develops between active real estate agents and brokers. This ratio has historically found balance at the level achieved in 2002: approximately 1.5 active agents for every active broker.

As real estate transactions entered the recovery phase of a market cycle in the early-2000s, new agents arrived en masse for the Millennium Boom. The greatly inflated agent population grew to as high as 2.7 agents per broker as big brokers filled their cubbies. These individuals obtained a license with the optimistic belief that extra money was to be had working real estate.

The agent-to-broker ratio fell in the Great Recession 2008 aftermath of the Millennium Boom, and in seven years reversed direction in 2014 to begin rising again.

Currently, the ratio hovers around 2.5 active agents per active broker. In Q2 2025, we are three years into lowered sales and leasing volume as we trudge our way through the temporary but wildly disruptive pandemic economy.

Expect the current ratio to decrease through 2029, following the downward path of home sales volume to its bottom, not rising for another three or so years. The public is fast to respond and run with boom times, but very pessimistic and unwilling to leap before a rise in sales prices becomes media headlines.

Agents speculate on the market

The real depth of agent inactivity is obscured by active licensee figures. Many “employed” agents simply do not report to work – at least not as a real estate agent. Their license is left “to hang” with a broker. They are underemployed, working as part-timers when deals pop up, while they gear up in a different occupation.

29% of all 307,350 sales agent licensees report to the DRE as “inactive” – around 90,000 licensed individuals who are not employed by a broker. Many inactive licensees do speculate in property as principals or negotiate purchases for family members, often presenting themselves as holding a license.

Related article:

Related article:

https://journal.firsttuesday.us/home-sales-volume-and-price-peaks/692/

Licensing in an economic recovery

Will the ideal 1.5:1 agent-to-broker ratio return when a trough develops in licensee population in the late-2020s?

Probably. A deep recession appears likely unless another pandemic-level monetary and fiscal stimulus is again initiated as occurred in 2020, and again as infrastructure upgrading in 2023.

With the pandemic stimulus well-implemented to pump up the economy, new sales agent and broker licensing jumped in 2021 as greater numbers of new licensees arrived and an increased percentage of existing agents renewed their licenses. Real estate sales volume peaked by mid-2022. The following downward trend saw enthusiasm to become an agent rapidly wane, which continues in 2025 – and likely into 2027.

Related article:

Brokerage Reminder: CAR membership NOT required for MLS access

Boomtime distractions, consumer protection and DRE licensing

Mortgage rates do tend to decline in a recessionary period. Less costly money becomes extra mortgage funds for buyers of property. However, the better borrowing power at lower mortgage rates is very quickly absorbed by sellers raising prices rather than buyers acquiring property with greater amenities. When news media reports the rapid increase in pricing, the appearance of profits generates increased numbers of new DRE-licensed agents. Most become employed by larger brokerage operations and franchised brands.

The next boomtime is likely to take place in the years following 2028 causing newly-minted agents to rapidly multiply.

With any boom, the standards applied by real estate service providers diminish in quality and quantity, temporarily set aside to cash in on the increased sales and leasing.

The DRE alone is tasked with actively protecting our consumer society from adverse licensee conduct. To do so, the DRE needs to become more aggressively involved during business recoveries. Initially, during the boom times, a tightening up of the agent licensing exam is needed to limit the licensing of new agents to the most qualified, persevering and committed individuals.

Whether the DRE is politically able to do this is questionable. The DRE faces opposition from big brokerage offices and their entrenched trade group. Large brokerage operations require a constant high number of agents-for-hire to blanket the market to capture rising fees when sales momentum takes hold.

Related article:

Market variables are changing

For the next years into 2028, fewer brokers and agents will be needed by sellers and users (aka buyers and tenants) to service the sale and leasing of real estate. It is simply licensee adjustment to:

- the current cyclical multi-decade increase in long-term interest rates now underway, and

- the return of a focus on owning real estate to occupy it or for income over the long haul, not one-shot profits on a sale.

In the past period of 1983 to 2013, ownership risks were covered by rising property values allowing owners to refinance and pull created wealth out of the property or sell and take it in profits. Increases in property value was generated primarily by the pre-2013 decades of declining mortgage rates, not by real estate fundamentals or astute investment decisions.

Related article:

Agent and broker population, past and future

2021 saw home sales volume leap as a result of historically low interest rates, individual stimulus checks and a fierce fear-of-missing-out (FOMO). However, the pandemic stimulus fuel was quickly spent, and sales volume in early 2022 began to quickly collapse which continues in 2025 and will likely continue at least into 2027.

Sales agent numbers accelerated rapidly during 2021, and through mid-2022, with an influx of “quick-buck” real estate agents. Expect to see these new-career agents drop out — as has already begun — and prices decline through 2026-2027.

Easy money, all the time, does not exist in any industry due to inevitable recurring business cycles.

Related article:

Industry behavior

Large single family residence (SFR) brokerage operations with branch offices have always depended on a constant flood of newly-licensed agents to fill their cubicles. These brokerage operations generate a high turnover rate for agents. Freshly-minted agents burn through their family members and social contacts without personal marketing to brand themselves and develop a viable client base.

The big brokers and their office managers have been able to mitigate the eventual loss of sales production experienced by client-exhausted agents through aggressively soliciting new licensees as replacements (and all the personal contacts who come with them).

These “list-and-run” agents also disappear from the ranks of new agents when the total annual number of new agents drops dramatically. The last such drop was in 2007-2014 before the commencement of the recovery in the mid-2010s. Previously, during the peak activity years of 2004-2007, new agents were licensed at the unsustainable rate of 5,000 monthly – triple the 2024 pace.

Despite this history, the number of new hit-and-run agents crept higher in the pandemic years of 2020-2021. And again, brokers spent little time training and supervising new agents and more time mining them for prospects.

Related article:

Pivot to find profits during a recession: Focus on homebuyers

Facing economic reality

firsttuesday forecasts an ongoing fallback in sales agent licensing in 2025-2026, the result of reduced buyer, leasing and MLO activity. Watch for the next wave of licensees to arrive, first upon the return of speculators, then end-user homebuyers, to propel the housing market into the next virtuous expansion period, likely to get a foothold around 2028.

When viewed in terms of disappearing short-term agents, rather than vanishing homebuyers — the rate of homeownership statewide was stuck at 55% at end of 2024 — what appears is an economic reality which forces employing brokers to:

- shutter their least productive branch offices;

- release the weakest office managers and under-performing agents;

- attempt to locate licensed agents who actually generate business;

- upgrade office locations and cut rent expenses by taking advantage of office and retail vacancies offering ever lower rent;

- develop new profit centers with service divisions for escrow, finance, homeowner/tenant insurance, appraisal/broker price opinions (BPOs), property management, investor syndication and other brokerage services; and

- require agents to “get back on the street” to engage in the community, gather property information in greater detail from local agencies, and smoke out new leads which generate transactions.

Related article:

Fee splitting problems

Gradually, the younger and more aggressive agents employed by large brokerage offices will look for new opportunities. They may become brokers or team up with other brokers and agents, transitioning into smaller flexible operations. Others with a long-term client base will join “rent-a-desk” operations to reduce the fee percentage extracted by the broker, and expect to take home more net earnings.

To be cautionary, agents jumping out on their own too often do not have the business acumen to set up and operate a broker office, whether they employ agents or operate independently. Their motivation to do so is based solely on the belief, right or wrong, that their current broker is taking too large a share of the fees.

Survival and success

Brokerage offices at present collectively need far fewer agents to effectively service the real estate needs of the public – until the return of willing buyers starts to take hold, likely in 2028. Blasphemous talk? Not at all; a pivot toward efficiency is necessary to steer a brokerage operation into full recovery mode.

During short-lived bursts of speculative fervor, discussion of a stable, disciplined office environment sounds like nonsense to brokers and agents with a short-term outlook. However, real estate is not a business where you can “fake it until you make it.” Misrepresentations by non-disclosure (or otherwise) and carelessness due to inexperience will undo you quickly, every time the market turns into a lengthy decline – a cyclical recession.

Brokers who learn to cut overhead and eliminate operating inefficiencies on early entry into a recessionary period, while beefing up their staff with competent agents and broker-associates are in the best position for the following long-term uptick in annual transaction numbers, likely to begin in 2028.

Employing brokers operating successfully through 2025 and 2026 will be defined by their ability to plan ahead for their needs.

A look ahead to reduced size of brokerage operations

Brokerage offices with fewer than 16 agents will probably continue to recruit agents in the manner they always have. Single-office brokerages traditionally recruit by local word-of-mouth referrals.

Large brokerages typically use mail-blitzing campaigns and seminars to entice both seasoned agents and newly-licensed and prospective agents into their branch offices. Franchised offices rely on brand name recognition to attract new agents.

Brokers maintaining a single office with a staff of agents and broker-associates tend to have several different types of business clientele. They do not focus on the numbers game of market share to drive property owners, buyers and tenants to their office for representation.

These smaller brokerage offices are the most likely to attract the more thoughtful agents who enter into the real estate industry. These entrants seek a long-term advantage of diverse training by teaming up with agents and broker-associates who work income property, land and property management as well as SFR and MLO transactions.

The broker takes charge

To operate a successful brokerage office, the broker needs to employ viable agents, those with talent and skill.

It is the maturity of the agents in a brokerage business model that produces the end result sought by successful employing brokers, i.e., broker fees. As in all service businesses, the linchpin for achieving success is the ability of management to orchestrate the efforts of agents to act and earn as permitted by DRE regulations and real estate law.

Brokers are best served when employing agents who practice beyond the small and limited circle of friends and family. Of course, some brokers dismiss the duty to provide training while supervising their agents. Brokers who do not dedicate sufficient time and energy to their agents will spend time and energy seeking replacement agents, a formula which weakens their market position.

Brokers need to be more than distant observers limited to providing remote oversight for the agents and sharing fees. They or their administrative assistants and managers are required to supervise and police the business-related activities and conduct of the agents they employ.

Related video:

Policing of business-related conduct

Further, the broker needs to be actively involved in the agent’s fulfillment of the duties the broker owes to clients the agent has contact with. Thus, the agent knows from the beginning just what level of production their broker expects of them to remain with the office. Also, the broker’s conduct demonstrates what their agents must do to maintain a competitive environment, producing representation agreements with property owners, buyers and tenants who are ready, willing and able to deal.

Accordingly, an office environment needs to nurture a greater probability of producing closings based on written client commitments to representation, purchase agreements, leasing agreements and mortgage originations, which collectively spell financial success for all involved.

Read more:

See RPI ebook Real Estate Matters: Chapter 2

{kind=link}

The market definitely got way too crowded during the pandemic boom. Most of these new agents are gonna get wiped out once they realize how dead the transaction volume actually is.

The 2021 surge was honestly just people looking for a side hustle during lockdowns. Most of these new agents are going to get washed out once the 2026 data drops.