MLO Mentor is an ongoing series covering compliance best practices for mortgage loan originators (MLOs). This article discusses abuse, theft, and fraud schemes related to Home Equity Conversion Mortgages (HECMs). Enroll in firsttuesday’s 8-Hour NMLS CE to renew your California MLO license and learn more about fraud and abuse prevention in your practice.

Home Equity Conversion Mortgages Exploited to Defraud Senior Citizens

In 2009, the Federal Bureau of Investigation (FBI) and the U.S. Department of Housing and Urban Development Office of Inspector General (HUD-OIG) released a report showing widespread Home Equity Conversion Mortgage (HECM) abuses. The FBI and the HUD-OIG found loan officers, mortgage companies, investors, loan counselors, appraisers, builders, developers and real estate agents were exploiting HECMs to defraud senior citizens.

Investigators found scammers used local churches, investment seminars and television, radio, billboard and mailer advertisements to target seniors. Protect your clients by familiarizing yourself with some common HECM scams.

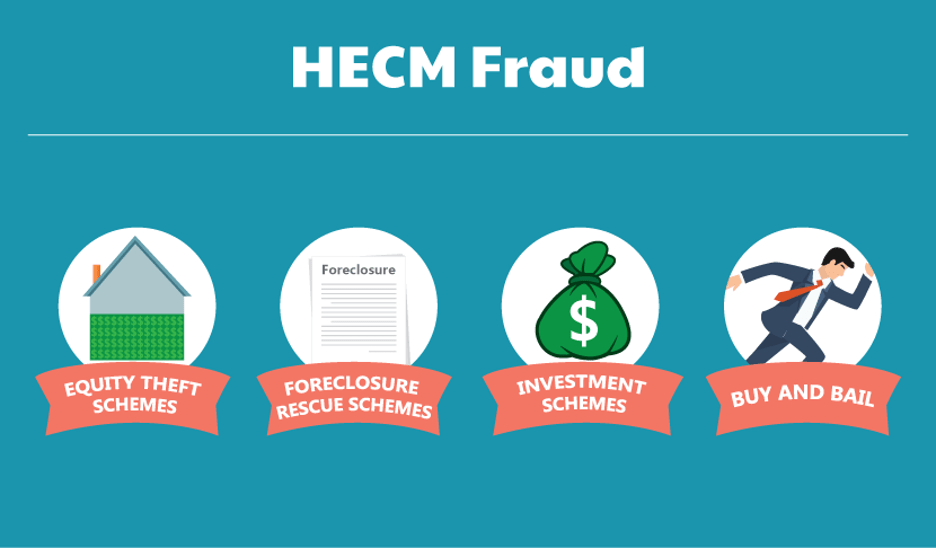

Equity theft schemes

The number one abuse found by investigators was the equity theft scheme. Scammers in equity theft schemes identified foreclosed, distressed or abandoned properties (or buyers) using information contained within county deed records. They then purchased the properties using straw buyers. The straw buyers would commit occupancy fraud by stating their intentions to use the property as their primary residence.

The scammers then recruited seniors to “purchase” the properties from the straw buyers by transferring the property deeds to the seniors with no exchange of money. After the seniors met the 60-day occupancy period, the scammers arranged for the seniors to obtain HECMS, using inflated appraisals. Then, the seniors were encouraged to pull out a large lump sum of the equity. The scammers then took the equity, and absconded.

Foreclosure rescue schemes

In foreclosure rescue schemes, scammers target seniors who are in jeopardy of losing their homes to foreclosure. The scammers offer reverse mortgage programs with a promise that these programs will prevent foreclosure.

Once the seniors are ready to enter into a loan agreement, the scammers inform the seniors they don’t qualify for a reverse mortgage at all. Instead, the scammers persuade seniors to take out a different type of loan offered by the scammer.

The scammers then locate a straw buyer, order fraudulent home repairs, complete an inflated appraisal and obtain a mortgage which transfers the property away from the seniors. The scammers then pocket the equity. The seniors are often notified by the new owner to either repurchase the home at a higher price or find alternative living arrangements.

Some senior citizens are recruited through advertisements for “free homes” and willingly participate in these schemes. The appraisals are generally inflated. The seniors get to live in the homes as long as they pay taxes, insurance and upkeep.

Lenders do not realize a problem exists until the seniors die or move out. At this time, any lender losses resulting from the false equity is passed from the lenders to the FHA, which pays the shortfall.

Investment schemes

Investment schemes are similar to equity theft schemes and are used by scammers to steal the HECM loan proceeds under the guise of investing it in an annuity, real estate or other investment product. The perpetrators of this scheme are often affiliated with the originator of the HECM loan and cross-sell the investment product to the victim.

Remember that the mortgage broker and lender involved in a reverse mortgage are prohibited from:

- participating in or otherwise associating with any party that participates in or is associated with any other financial or insurance activity;

- accepting any incentive for providing the borrower with any other financial or insurance product; or

- directly or indirectly requiring the purchase any other financial or insurance product as a condition of arranging or making the reverse mortgage. [12 USC §1715z-20(n)-(o)]

Buy and bail

This scam is perpetrated directly by the senior borrower in connection with a HECM purchase loan. In this scam, the borrower purchases a more affordable dwelling with the intention of no longer making payments on the previous mortgage.

Additional schemes associated with reverse mortgages include sales of unsuitable financial products, broker conversion, misrepresentation of the borrower’s permanent residence, age and competency, identity theft, inflated collateralized value, land record/deed forgery, forged payoffs of pre-existing liens and mortgages, loans arranged by children or other third parties without the consent of the senior borrower, forged power of attorney, settlement agent fraud and scams charging excessive fees for otherwise free reverse mortgage information.

When this report came out in 2009, the rising number of seniors falling victim to these scams — who were collectively worth over $4 trillion in home equity –– was coupled with program vulnerabilities, such as the lack of income credit, or employment qualifications. This type of risk layering created significant opportunities for fraud perpetrators.

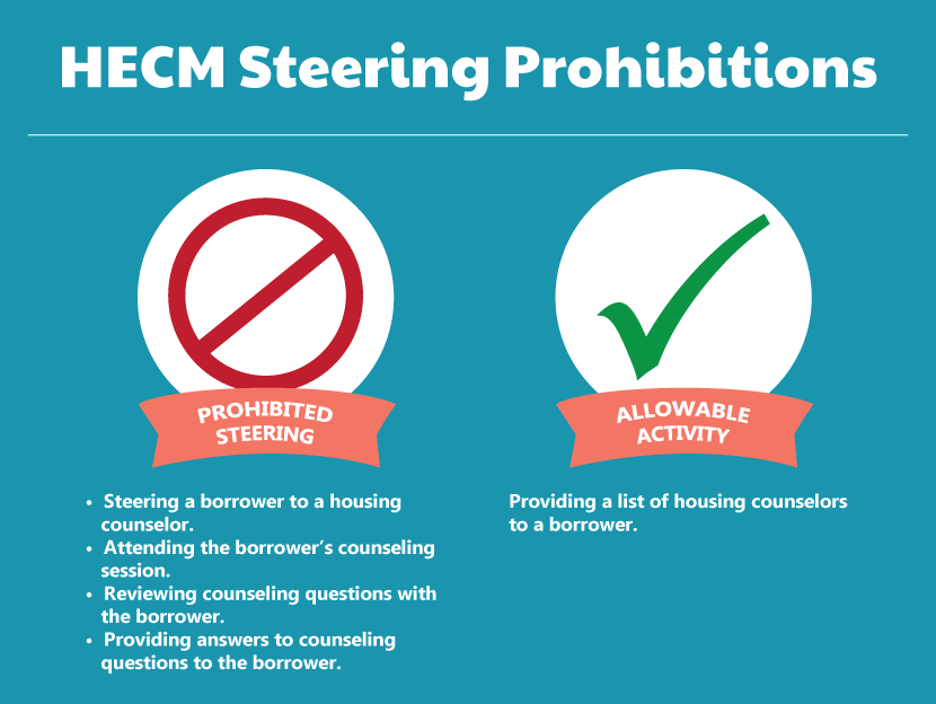

Prohibitions against steering

In early 2013, HUD issued a warning to reverse mortgage lenders to avoid steering potential borrowers to specific HECM counseling agencies. In some cases, lender representatives were present or even participating in counseling sessions. Some lenders provided advance copies of borrower review questions used by HECM counselors.

Recall that while lenders are required to provide a list of acceptable HECM counselors for the purpose of fulfilling reverse mortgage counseling requirements, lenders are prohibited from steering borrowers to specific counselors. The prohibition specifically states:

“The lender may not steer, direct, recommend or otherwise encourage a client to seek the services of any one particular counselor or counseling agency. Lenders are required to give every client a list of HECM counseling providers that includes the national intermediaries providing telephone counseling and five agencies in the local area and/or state of the client with at least one of the local agencies located within a reasonable driving distance for face-to-face counseling.” [HUD Handbook 7610.1 Chapter 4-11]

Further, lenders are prohibited from attending or participating in the counseling session. While the HUD Handbook allows interested parties with an advocacy interest in the reverse mortgage, such as relatives and attorneys, to attend the session with the borrower, the HUD guidelines specifically forbid a lender’s representative from attending the session with the borrower.

Lenders are also prohibited from reviewing the questions or providing the counseling questions to the borrower. This interferes with the counselor’s role in providing information to the borrower. Additionally, information provided by the lender is not guaranteed to be correct, or current.

Failure to adhere to the requirements outlined in HUD handbooks and mortgagee letters may result in a referral to the Mortgagee Review Board for appropriate sanctions including but not limited to civil money penalties, suspension and withdrawal of approval to participate in FHA programs.

Other consumer protection concerns

Not all consumer protection concerns about reverse mortgages stem from fraudsters and scam artists. Similar to many nontraditional mortgage products, some of the most important consumer protection issues arise from asymmetry of information. In other words: reverse mortgages are complicated, and borrowers don’t understand their terms.

In its 2012 report to Congress, the CFPB identified three main deficiencies regarding the transparency of reverse mortgages:

- the rising balance and falling equity nature of reverse mortgages is difficult for reverse mortgage borrowers to understand;

- innovation and policy changes regarding reverse mortgages were not being adequately explained, and were creating confusion for consumers; and

- the federal disclosures required on reverse mortgages were providing inadequate guidance on the benefits and drawbacks of reverse mortgages.

Additionally, the relatively low barrier to obtaining a reverse mortgage resulted in seniors taking out reverse mortgage at younger ages — sometimes even before retirement. This added to the risk that they would deplete their equity before being able to plan for future healthcare or moving costs.

The CFPB found that, instead of using the proceeds of the reverse mortgage pay for everyday expenses in retirement, most reverse mortgage recipients (73% in 2011) were pulling out all or nearly all of their equity to invest or save elsewhere. Oftentimes, the investments did not pay out as much as the borrower was accruing in interest on the reverse mortgage!

Another increasingly common practice is for borrowers to take out a reverse mortgage to refinance a traditional mortgage and avoid monthly mortgage payments. While this did undoubtedly eliminate the borrower’s mortgage payments, the easy liquidity also threatened the borrower’s ability to plan for future costs. In some cases, the reverse mortgage proceeds were used to prolong unsustainable financial situations.

Reverse mortgage borrowers who pulled out all the equity from their homes were at greater risk of becoming delinquent on taxes and insurance, and therefore more vulnerable to foreclosure.

{kind=link}