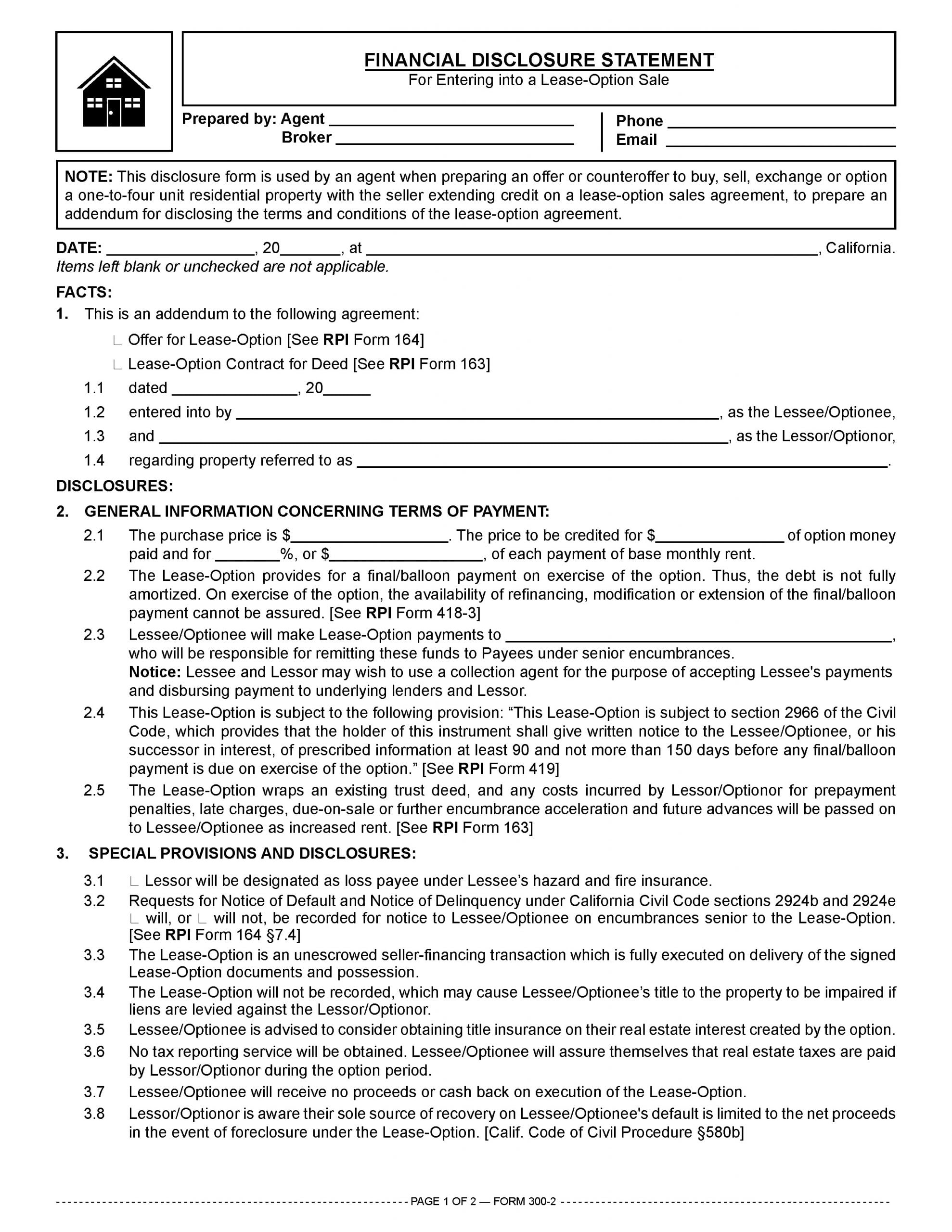

This disclosure form is used by an agent when preparing an offer or counteroffer to buy, sell, exchange or option a one-to-four unit residential property with the seller extending credit on a lease-option sales agreement, to prepare an addendum for disclosing the terms and conditions of the lease-option agreement.

Carryback financing

Seller financing, also known as carryback financing, occurs when a seller carries back a note and trust deed executed by the buyer to evidence a debt owed for purchase of the seller’s property.

A seller who offers a convenient and flexible financing package to prospective buyers makes their property aggressively more marketable and defers the tax bite on their profits.

For buyers, seller carryback financing offers:

- a moderate down payment;

- competitive interest rates;

- less stringent terms for qualification than those imposed by lenders; and

- no origination costs.

Seller financing is documented in a variety of ways, including:

- land sales contracts;

- lease-option sales;

- sale-leasebacks; and

- trust deed notes.

A carryback seller assumes the role of a lender at the close of the sales escrow. This includes all the risks and obligations of a lender holding a secured position in real estate.

The secured property described in the trust deed serves as collateral for the debt. The property itself is the seller’s sole source of recovery to mitigate the risk of loss on a default by the buyer.

Lease-option sales

A lease-option sale is a sales transaction characterized by a purchase agreement containing a provision for the transfer of possession on a lease and buildup of equity in ownership by the tenant over the term of the lease before closing the sale by crediting the purchase price with a portion of the buyer’s lease payments.

For example, consider a buyer and seller who sign a standard purchase agreement. [See RPI Form 150]

Escrow is opened, and a grant deed, a carryback note, a trust deed and the down payment are deposited into escrow. However, the closing and disbursement of funds are delayed until after one to three years of timely performance by the buyer.

During the extended escrow period, payments are made by the buyer to the seller which include credit of a portion of the payment toward the down payment called for in the purchase agreement.

Since the buyer wants to take possession of the property prior to the close of escrow, they enter into an interim occupancy (lease) agreement with the seller.

Buyers and sellers of real estate need to understand that a sale structured as a lease-option is still a sale under California law. The form used to structure the sale does not change a buyer’s or seller’s rights and obligations under mortgage and contract law. [See RPI Form 300-2]

The lease-option sale usually is not documented through an escrow, nor is there delivery of a grant deed or a note and trust deed.

Instead, the buyer will lease the property and hold an option to purchase the property at a predetermined price, not a price based on market value at the time of exercising the option. Thus, any increase in value accrues to the buyer, not the seller.

Except for the absence of documentation in the form of a grant deed, note and trust deed, the terms of the lease-option sale have all the economic characteristics of a credit sale. Under a lease-option sale, there is:

- an agreed-to price;

- a down payment;

- monthly rent payments which apply in whole or in part toward principal (the balance being interest); and

- a final/balloon payment for the balance of the unpaid purchase price.

A lease-option agreement structured on terms economically consistent with a credit sale is neither a lease between a tenant and a landlord nor an option to buy. The lease-option sales agreement is a disguised security device for credit financing on a sale arranged by a buyer and a carryback seller. [Oesterreich v. Commissioner of Internal Revenue (9th Cir. 1955) 266 F2d 798]

An agent uses the Financial Disclosure Statement for Entering into a Lease-Option Sale form published by RPI when preparing an offer or counteroffer to buy, sell, exchange or option a one-to-four unit residential property with the seller extending credit on a lease-option sales agreement. It allows the agent to prepare an addendum for disclosing the terms and conditions of the lease-option agreement. [See RPI Form 300-2]

Form navigation page published 09-2021. Updated 01-2026.

Form last revised 2016.

Article: Disclosures on seller carrybacks

Article: Land sales contracts and lease-option sales

Client Q&A: What is seller carryback financing and what are its benefits?

FARM: Attention Note Holders and Carryback Sellers!

Brokerage Reminder: Carryback financing – securing alternatives for buyers and sellers

Brokerage Reminder: Carryback financing – the creditworthy buyer and mandated disclosures

Recent Case Decision: Does a contract of sale establish a buyer-seller relationship protecting the buyer from eviction upon default?