Swapping properties, equities and mortgage debt

An exchange of properties is a multi-property “sales” transaction structured as a barter — a swap — entered into by the respective owners of two or more parcels of real estate, each having value in their equity.

By an agreement, ownership of the properties is transferred between owners by the concurrent conveyancing of the properties, the value of the equity in one property being part or all the consideration given for the equity in the other property.

The exchange transaction, often called a trade, is in fact separate sales of two properties each owned by different persons, which are acquired — purchased — by the other person.

Exchanges occur most frequently during the recessionary phase of a business cycle when cash becomes scarce — king. During recessions, property owners frequently are unable (or unwilling) to part with cash and the supply of properties whose owners need to sell are plentiful.

Financial adjustments are arranged for the difference in the dollar value of equity in each property based on the dollar amount given each in the exchange agreement. The dollar values set for pricing and equity do not affect income tax reporting, but cash and mortgage balances are part of the tax reporting on the transaction. [See RPI e-book Tax Benefits of Ownership, Chapter 23]

Thus, an owner of real estate, on entering into a written exchange agreement, agrees to sell and convey their property to the other owner who agrees to purchase and acquire it — take it in trade.

However, unlike a sale under a purchase agreement, the down payment on the agreed price is not in the form of cash. Rather, the down payment on the property acquired is the equity in a property the owner wants to dispose of.

Unlike a sale calling for a cash down payment and assumption of an existing mortgage or new financing, any balance of the price remaining to be paid on the price in an exchange is often deferred, evidenced by a carryback note and trust deed.

Exchanges frequently have little to no cash involved beyond transactional costs, a side effect of the times when exchanges are more prevalent at marketing sessions.

Related article:

The concept of an exchange transaction

The hallmarks of an exchange transaction, in contrast to the common features of a typical sales transaction, include:

- the exchange of equities in real estate in lieu of a cash down payment, though some cash might be involved, casually referred to as a sweetener;

- no good-faith deposit since cash is infrequently used in an exchange of equities. The consideration needed to contractually bind the two owners on entering into the exchange agreement is the signature of each owner. As in any real estate purchase agreement, no cash deposit is required to form a binding contract;

- a takeover of existing financing with or without a formal assumption of the mortgages, rather than refinancing and incurring expenses which greatly increase the cost of acquiring real estate;

- adjustments brought about by the difference in the value of the equities exchanged, a “balancing of the equities,” in which the owner with the lesser-valued equity covers the dollar difference, typically by a trust deed note calling for installment payments;

- joint or tandem escrows, interconnected for the concurrent conveyance of properties, similar in effect to a buyer purchasing property when their closing is contingent on their selling other property to fund their purchase price. This contingency occurs in §1031 reinvestment plans when agreeing to buy a property as the replacement property before selling the property to be disposed of;

- two sets of broker fees, one for each property involved in the exchange and classically shared equally between the brokers involved, rather than the receipt of a single fee as occurs in a cash-out sale of property; and

- each owner is simultaneously involved in both selling and buying, a coupling of two transactions, one consisting of their sale of a property and the other being their purchase of a different property.

Related article:

Locating properties for exchange

When searching for replacement properties, the owner’s agent first locates suitable properties owned by someone interested in acquiring the client’s property.

The agent contacts agents who have listed suitable property to determine whether their client is interested in acquiring property in exchange. If so, whether they are willing to acquire the type of property owned by the agent’s client.

A prudent agent will not prepare or submit an offer to exchange before obtaining an understanding that the other owner has a willingness to consider an exchange of properties.

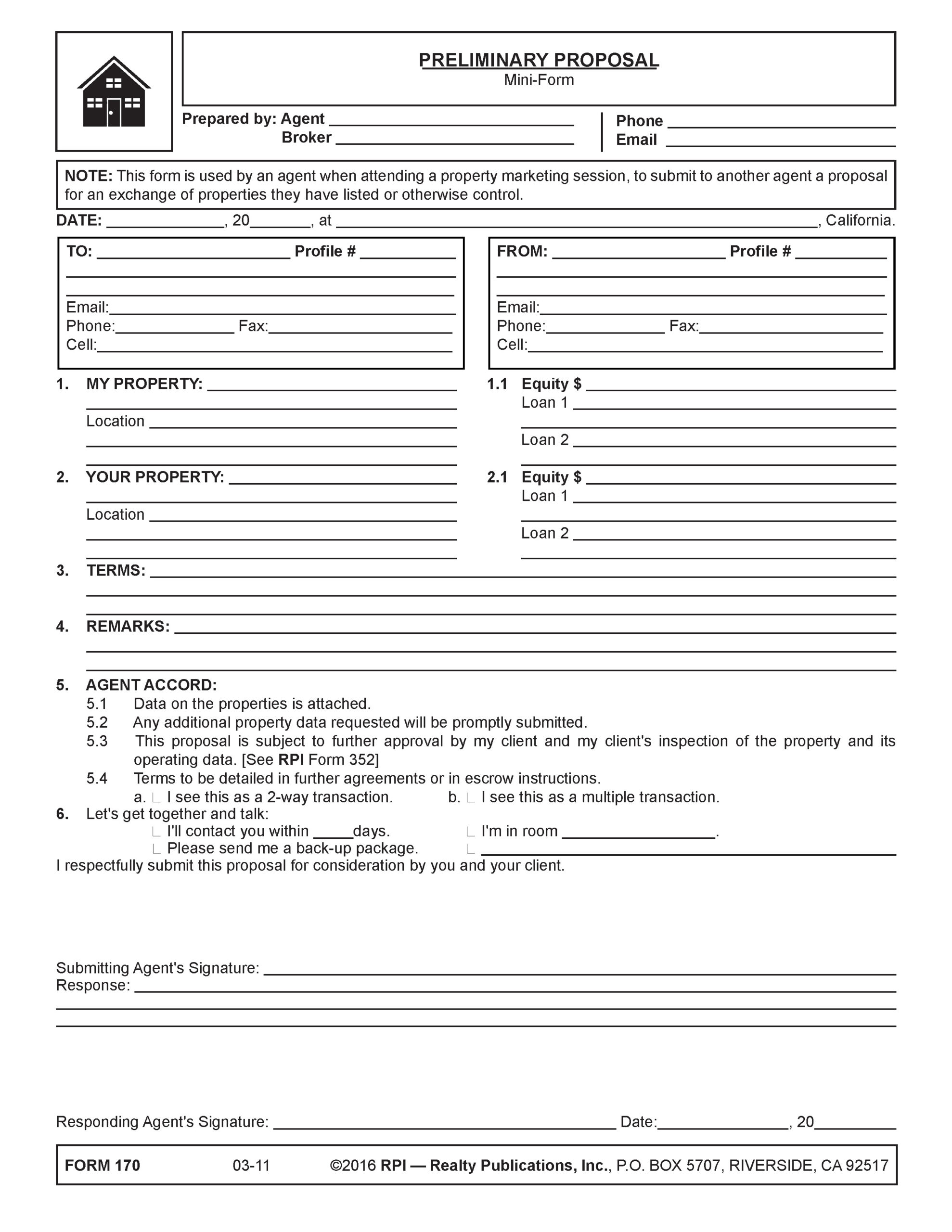

To look into the possibility of an exchange for a property of the type a client will accept, and to document the inquiry for later follow up, an agent will often prepare a preliminary proposal form. It is delivered to the other agent to encourage discussions — the catalyst needed to explore the probability of an exchange. [See RPI Form 170]

The proposal form notes the type of properties involved, the amount of equity and debt, and arranges for the exchange of property information for a discussion between the agents before preparing an exchange agreement. [See RPI Form 170]

The agent retains a copy of the prepared form in the client file as evidence of the agent’s duty owed to the client to diligently locate property. [See RPI Form 170]

The preliminary proposal is not an offer. As a proposal, it does not contain intent-to-contract wording. The clients are not directly involved in the proposal, only the agents who are looking for a possible match.

On determining the probability of the other owner to enter into an exchange, the agent prepares an exchange agreement, gathers signatures, and submits it for consideration. [See RPI Form 171]

Analyzing the preliminary proposal

An agent uses the Preliminary Proposal — Mini-Form published by Realty Publications, Inc. (RPI) when attending a live or online property marketing session. The form allows the agent to hand deliver or email their proposal for an exchange of properties to the agent who has listed or otherwise controls a target property. [See RPI Form 170]

The Preliminary Proposal contains:

- the date;

- the responding agent’s information;

- the submitting agent’s information;

- the submitting agent’s property, location, and equity amounts;

- the responding agent’s property, location and equity amounts;

- terms of the intended sale;

- any special remarks from either party;

- whether the agent sees this as a two-way transaction or a multiple transaction;

- additional contact details;

- the submitting agent’s signature; and

- the responding agent’s signature. [See RPI Form 170]

Related FARM letter:

Structuring the transaction

As in all real estate transactions, a written form is used to prepare the offer and commence effective written negotiations. The objective of a written agreement is to provide a comprehensive checklist of boilerplate provisions a client is to consider in their offer, an acceptance, or counteroffer negotiations.

Once the owner’s agent locates a suitable like-kind replacement property, owned by a person whose agent indicates is willing to consider an exchange of the properties, the agent prepares an exchange agreement. [See RPI Form 171]

The agent reviews the terms of the exchange agreement with the owner, they both sign it, and the agreement is submitted to the agent for the owner of the replacement property for acceptance, counteroffer, or rejection. [See RPI Form 171]

Analyzing the exchange agreement

An agent uses the Exchange Agreement — Other than One-to-Four Residential Units published by RPI when negotiating the exchange of properties — other than a one-to-four unit residential property. The form allows the agent to prepare an offer to exchange the ownership of properties. [See RPI Form 171]

The Exchange Agreement includes:

- Facts: the agent enters the date of preparation for referencing the agreement, the names of the owners, the description of the properties to be exchanged and each property’s fair market value, equity valuation and mortgage encumbrances [See RPI Form 171 §§1 and 2];

- Terms of exchange: the agent sets forth the total consideration each owner is to deliver to the other owner, such as the transfer of their equity and adjustments in the form of cash, carryback note, mortgage assumptions or value in additional property, and any new financing required to generate the cash needed to acquire the replacement property [See RPI Form 171 §3];

- Acceptance and performance: the agent includes provisions, such as excuses for nonperformance and termination of the agreement, the time period for acceptance of the offer, the broker’s control over enforcement of performance dates, the financing of the price as a closing contingency, procedures for cancellation of the agreement, cooperation to effect a §1031 transaction and limitations on monetary liability for breach of contract [See RPI Form 171 §4];

- Property conditions: each owner confirms the physical condition of the property received is as disclosed prior to acceptance [See RPI Form 171 §§5 and 6];

- Closing conditions: the agent establishes the escrow holder, escrow instruction arrangements, date of closing, title conditions, title insurance, hazard insurance, prorates and mortgage adjustments [See RPI Form 171 §7];

- Brokerage fees: the agent sets the brokerage fee, confirms the delivery of the agency law disclosure to both parties, and confirms the agency undertaken by the brokers and their agents on behalf of one or both parties to the agreement [See RPI Form 171 §8];

- Signatures: both parties bind each other to perform as agreed in the exchange agreement by signing and dating their signatures to establish the date of offer and acceptance. [See RPI Form 171]

Related article:

Want to learn more about property exchanges? Click the image below to download the RPI book cited in this article.

{kind=link}