This form is used by a loan broker when processing a mortgage application to be prepared by the borrower for the loan broker, to determine the borrower’s sources and amounts of income, personal expenses and net income and set the borrower’s debt-to-income (DTI) ratios.

A life preserver for underwater homeowners

Home prices in early 2023 are nosediving in California at a pace of 1 ½% monthly. That monthly rate is likely to continue, except for a modest mid-2023 buyer demand bump and into 2024, hitting a bottom price level in 2025. This pricing activity heralds the start of a new business cycle in our economy.

Homebuyers who purchased in the past few years funded mostly by a mortgage face the risk of insolvency. Month by month and in the reverse order of acquisition, increasing numbers of these mortgaged homeowners will fall underwater — continuing until property prices develop a bottom level.

As these events occur, the pernicious presence of negative equity will become inescapably more common. How can proactive licensees best pivot to service this evolving market?

A lens on equity

Two breeds of negative equity homeowners exist:

- those who are fully aware of their financial plight but do not know how to correct it; and

- those who aren’t aware or are in willful disregard of their precarious financial footing.

For compelling insight into a family’s household equity position, look no further than a balance sheet. [See RPI Form 209-3]

As a worksheet, the homeowner lists on a balance sheet with dollar amounts all the homeowner’s:

- assets; and

- liabilities (debts). [See RPI Form 209-3]

The balance sheet is a tool adopted to break down a homeowner’s financial status into its component parts. The use of the balance sheet, also called a statement of financial position, is a simple, clear-voiced exercise in financial planning. The entries are like those found in the homeowner’s mortgage application.

For the greatest understanding of debt, the balance sheet analysis needs to be conducted by every household (and investor and businessperson) at least once each year.

Preparation of a balance sheet is especially instructive to families who purchased or refinanced during the rapid price escalation from mid-2020 to mid-2022, since they are most likely to be underwater or will soon reach that status.

For the majority of homeowners, their greatest asset (or obverse position of liability) is their home.

By completing a balance sheet, a homeowner can develop a firm mental grasp on the family’s accumulated wealth. In turn, prudent long-term financial decisions are enhanced.

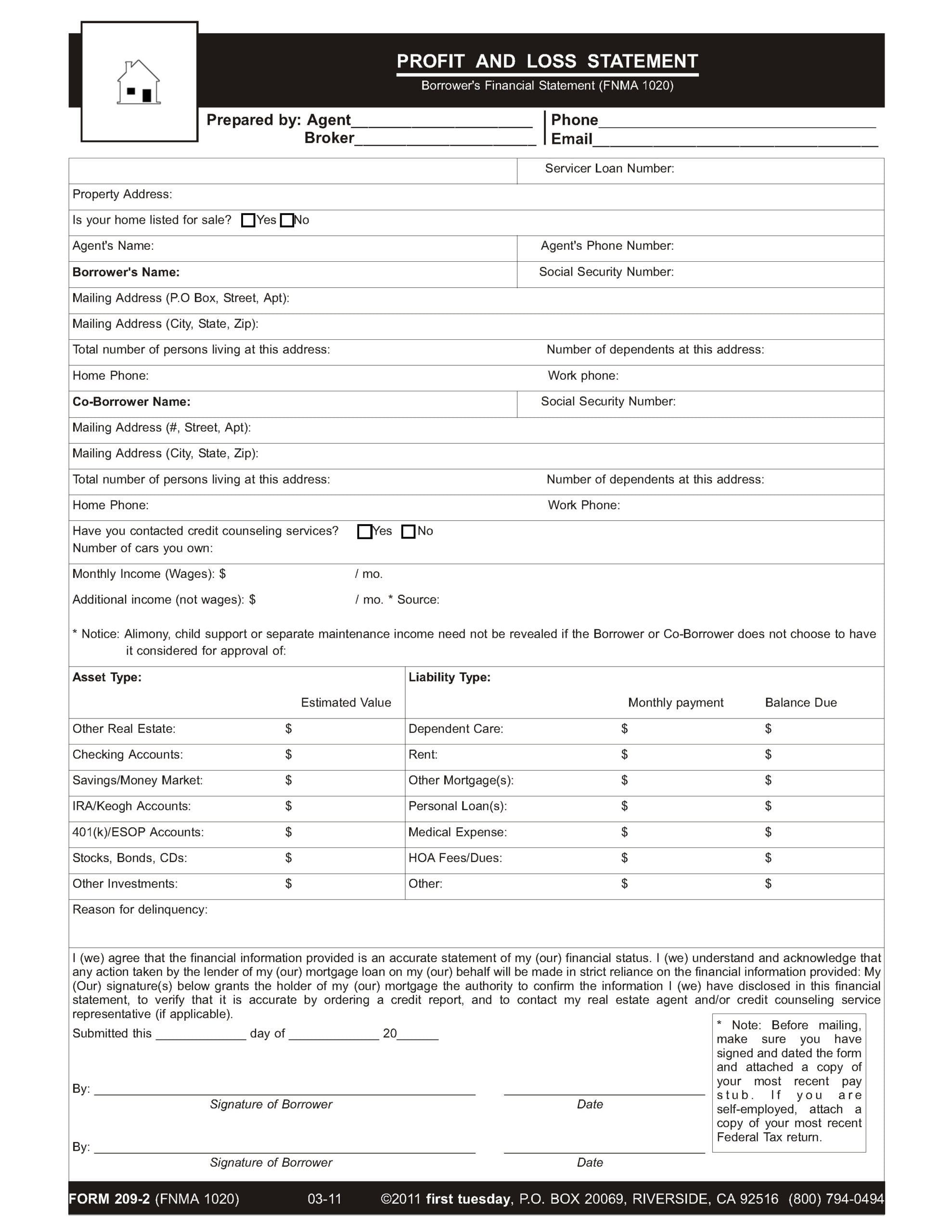

The profit and loss worksheet

In contrast, a profit and loss (P&L) worksheet is a separate but tandem financial statement serving a different and proactive purpose. It is the basis for a critical budgetary review for adjustments to be made in the homeowner’s ongoing monthly income and expenditures. [See RPI Form 209-2]

A P&L does not deal with the value of the home — an asset — or the mortgage debt — a liability.

Instead, a P&L lists the homeowner’s monthly ebb and flow of cash, consisting of:

- personal income;

- monthly expenses; and

- long-term obligations, including mortgage payments.

A balance sheet is about gold bricks stashed in the basement, not budgeting for expenditures of the household income. For budgeting, a P&L is the preferable tool. [See RPI Form 209-2 and 209-3]

A mortgage broker uses the Profit and Loss Statement — Borrower’s Financial Statement published by RPI when processing a mortgage application. It is prepared by the borrower and delivered to the mortgage broker. The form discloses the borrower’s sources and amounts of income, personal expenses and resulting net income available for savings as an economic cushion. With this information, the mortgage broker calculates the borrower’s debt-to-income (DTI) ratios.

The P&L is also used by an agent assisting a homeowner in their household budgeting. [See RPI Form 209-2]

The Profit and Loss Statement — Borrower’s Financial Statement contains the following information:

- monthly income (wages) and additional income (not wages);

- the estimated value of assets by type, including:

- other real estate;

- checking accounts;

- savings;

- IRA accounts;

- 401(k) accounts;

- stocks, bonds, securities and CDs; and

- other investments; and

- the monthly payment and balance due on liabilities, including:

- dependent care;

- rent;

- other mortgages;

- personal loans;

- medical expenses;

- homeowners’ association (HOA) fees; and

- other debts. [See RPI Form 209-2]

For delivery to a mortgage broker, the borrower signs and dates the form and attaches a copy of their most recent pay stub or, when self-employed, a copy of their most recent federal tax return.

Form navigation page published 03-2023. Updated 01-2026.

Form last revised 2011.