Listing agreement as an employment contract

A listing agreement is an employment contract entered into by a broker and a client, evidence of the fiduciary relationship of agency. In contrast, mortgage lenders do not have clients, just customers called consumers. Thus, lenders do not enter into written employment agreements with borrowers, but do make offers and take applications.

As discussed in the context of this agreement, the broker’s client may be:

- a borrower seeking a mortgage or a mortgage-backed loan (MBL); or

- a noteholder seeking to sell a note directly or collaterally secured by a trust deed.

Listing agreements are used by brokers when a client, typically a buyer or individual owner of real estate or holder of a trust deed note, wants to:

- obtain a mortgage or a loan collaterally secured by an existing trust deed note such as a seller carryback note [See RPI Form 104]; or

- sell an existing note or a note collaterally secured by a trust deed. [See RPI Form 112]

Here, the listing agreement obligates the client to pay the broker an agreed-to fee when the broker arranges a loan or sale of a TD note as arranged or agreed in the listing agreement.

Written fee agreement

A broker and their agents use a loan broker listing agreement when agreeing to provide services for a fee to:

- arrange mortgage financing to fund the purchase of real estate;

- refinance an existing mortgage;

- sell an existing trust deed note; or

- further encumber a property to obtain cash. [See RPI Form 104]

On entering into an exclusive right-to-borrow listing agreement, the client employs the broker to act on their behalf to locate a lender and arrange a mortgage to be secured by:

- a property to be purchased; or

- a property currently owned by the client. [See RPI Form 104]

The right-to-borrow listing agreement grants the broker sole authority to solicit mortgage lenders and locate one who will originate a mortgage on terms sought by the client.

Critically, it states the fee amount the client agrees the broker is to receive and the conditions to be met for the broker to be entitled to collect the fee they earn.

Formal documentation of an obligation to pay a fee — a written agreement signed by the client — is the mandated requisite to the right to enforce collection of a brokerage fee from the client.

Related video:

Analyzing the loan broker listing agreement

An agent uses the Loan Broker Listing Agreement — Exclusive Right to Borrow published by Realty Publications, Inc. (RPI) when agreeing to be employed by a buyer or an owner of a property as their sole agent for a fixed period of time. The form authorizes the agent to arrange a mortgage to be secured by the property. [See RPI Form 104]

The Loan Broker Listing Agreement — Exclusive Right to Borrow contains:

- Retainer commitments: the listing period, broker objectives and client’s trust funds deposit for costs [See RPI Form 1041];

- Addenda: a credit application, loan purpose statement, acknowledgement of changing conditions, and other addenda to be added to the checklist [See RPI Form 1042];

- Brokerage fee: the amount of the fee the broker is to receive for their services [See RPI Form 1043];

- Loan terms: loan terms sought by the client [See RPI Form 1044];

- Real estate securing the loan: the type, address, recorded encumbrances, improvements, fair market value (FMV), property taxes and rental information [See RPI Form 1045];

- Personal property included as collateral: a description, value, amount of encumbrance and lender [See RPI Form 1046];

- General provisions: Broker and owner authorizations and warranties, and a mediation provision [See RPI Form 1047]; and

- Signatures of the broker and buyer or owner. [See RPI Form 104]

Related article:

Disclosure of second fees

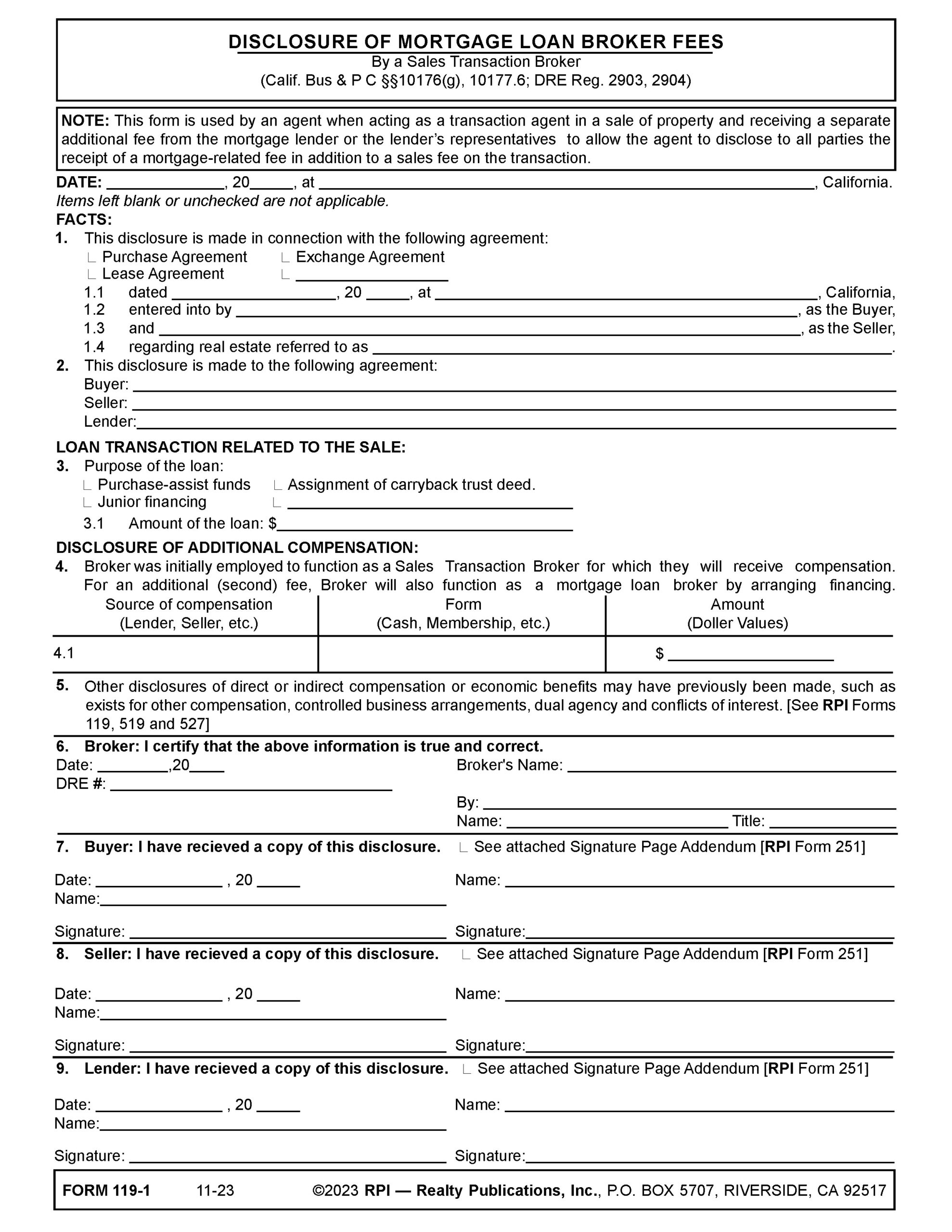

Any broker participating as an agent in a sales transaction who expects to receive a fee other than the sales fee, such as loan broker fee or any other fee evolving out of the related mortgage origination, uses a Disclosure of Mortgage Loan Broker Fees form to advise the client of the additional earnings. [See RPI Form 119-1]

Consider an agent representing a buyer in a sales transaction. In addition to performing the regular agency duties owed to the buyer, such as using due diligence and coupling information known to the agent with specific advice to the buyer, the agent intends to receive an additional fee in connection with the buyer’s loan.

To concurrently act as a sales transaction agent and, by necessity, perform mortgage related activity in expectation of an additional fee, the agent and their broker needs to comply with two tiers of law.

The first tier is the federal Real Estate Settlement Procedures Act (RESPA), also known as Regulation X. RESPA establishes a no-service, no second-fee restriction on real estate brokers and agents who are already acting on behalf of a buyer or seller in a one-to-four unit residential real estate sales transaction financed by a RESPA mortgage, called consumer mortgages which excludes business, investment or and agricultural mortgages.

In application, a broker already receiving a fee for participating in a sales transaction may only receive additional fees related to the origination of a mortgage to fund the sales transaction when the broker (or their agents) performs significant services to process the mortgage. Thus, the broker or their agents need to perform some meaningful activities as a mortgage loan broker (MLB) in arranging or processing the mortgage.

Thus, a broker may only receive a second fee in addition to their sales transaction fee when they or their agents render significant mortgage origination services which otherwise are performed by the lender. Mere referral of the buyer to a lender by a transaction agent does not justify the additional fee, which would then be a prohibited kickback to the broker. [12 United States Code §2607(c)]

As the second tier set by state law, the broker in a sales transaction who is to receive an additional fee related to mortgage services must, as the agent for either the seller or the buyer, disclose to their client all forms of compensation they are to receive arising out of the transaction. This, includes the dollar amount of compensation and the source of payment. [See RPI Form 119]

However, when a broker is conducting mortgage origination services on behalf of the buyer (or the lender) needed to justify collection of a second fee, the second fee needs to be acknowledged by all participants to the sale and mortgage transactions, including the buyer, seller and lender. [See RPI Form 119-1]

Brokers or their agents have 24 hours after undertaking the mortgage processing activity in expectation of a second fee to disclose the expectation of that second fee, and before proceeding to further represent the client, obtain the consent of all participants. [See RPI Form 119-1]

Related video:

Analyzing the disclosure of mortgage loan broker fees

An agent uses the Disclosure of Mortgage Loan Broker Fees – By a Sales Transaction Broker published by RPI when acting as a transaction agent in a sale of property and receiving a separate additional fee from the mortgage lender or the lender’s representatives (MLB & MLOs). The form allows the agent to disclose to all parties the receipt of a mortgage-related fee in addition to a sales fee on the transaction. [See RPI Form 119-1]

The Disclosure of Mortgage Loan Broker Fees; By a Sales Transaction Broker contains:

- Facts: the type of transaction, date of the agreement, relevant real estate, and identities of the buyer, seller and lender [See RPI Form 119-1§1 and 2];

- Loan transaction related to the sale: the purpose and amount of the mortgage loan [See RPI Form 119-13];

- Disclosure of additional compensation: the source, form and amount of the broker’s anticipated second fee [See RPI Form 119-14]; and

- Signatures of the broker, buyer, seller and lender. [See RPI Form 119-1§6 through 9]

Want to learn more about receiving and splitting broker fees? Click the image below to download the RPI book cited in this article.

{kind=link}