While high inflation has been making headlines in 2021, coverage of today’s rapidly rising home prices is humdrum in comparison. When did such significant home price increases become acceptable to homebuyers and everyone else?

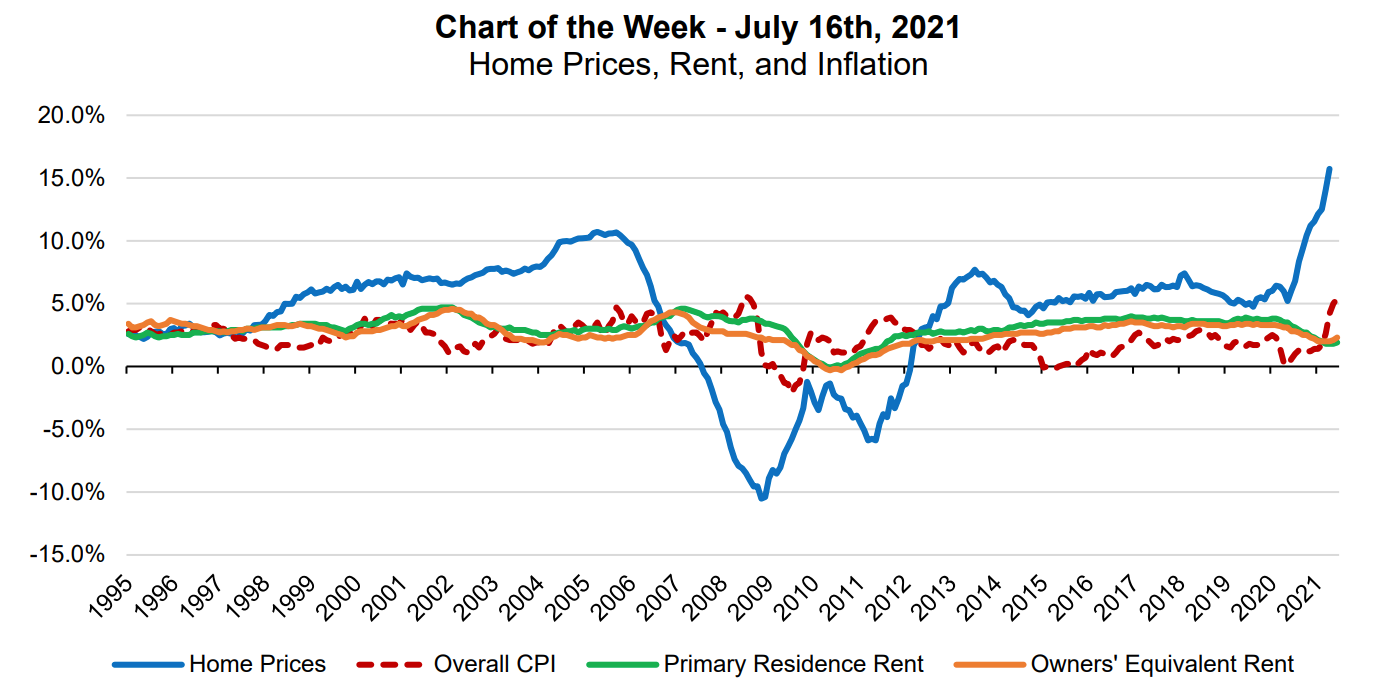

Source: Mortgage Bankers Association (MBA)

The MBA chart above shows the U.S. average annual percent change in home prices, the consumer price index (CPI) and rents.

Nationally, home prices were 15.7% higher than a year earlier as of April 2021. Here in California, home prices were a more significant 17% higher than a year earlier for high-tier prices and 18% higher for low- and mid-tier prices.

There are two types of inflation at work here:

- consumer price inflation, including the price level of all goods and services in the economy; and

- asset price inflation, inclusive of the price of assets like stocks and real estate.

Consumer prices have increased over the past year, due to consumer behavior following the pandemic closures. Now that travel is picking up and stores are opening fully, consumer demand is rising. At the same time, supply disruptions and fewer workers willing to work low-income jobs in the service, retail and restaurant industries, mean supply for these desirable goods and services remains low.

The result is higher prices, and higher inflation.

True, June 2021’s CPI of 5.4% was the highest since 2008, and monthly core inflation was higher than at any point since the 1980s. But, following the blue home price line, the MBA’s chart shows how today’s steep home price increases are even more significant than in the volatile years of the Millennium Boom.

Today’s high home prices are also thanks to a supply-and-demand imbalance. Along with increased purchasing power due to low interest rates, in the face of low inventory, eager homebuyers have pushed home prices to their historic levels in 2021.

Related article:

The problem with high inflation — and home prices

A healthy level of inflation — typically around 2%-3% — is necessary to stimulate economic growth. But what happens when inflation runs too high?

Brief periods of high inflation are momentary distortions, and may not be worth worrying too much about. But when high inflation persists, the harmful impacts include:

- lower consumer savings rates;

- reduced consumer purchasing; and

- a lower quality of life for residents.

A similar impact occurs when home prices increase beyond the pace of incomes. These volatile home price increases have put homeownership beyond the reach of many would-be homebuyers who are otherwise qualified to purchase. Without access to adequate housing for low- and moderate-income residents, regular residents fall behind in terms of wealth creation.

For real estate professionals, when home sales are available to only the most wealthy individuals, transaction potential decreases. Then, brokers, agents and mortgage professionals are reliant on a dwindling number of transactions for their living. California real estate professionals already have a taste of what this feels like, as the Golden State is consistently home to the second-lowest homeownership rate in the nation.

To increase homeownership, today’s rapid home price increase will need to subside. To accomplish this, inventory will need to rise to meet homebuyer demand, and this will happen only when sufficient residential construction returns to California.

{kind=link}

Thank you for your post. I have read through several similar topics! However, your article gave me a very special impression, unlike other articles. I hope you continue to have valuable articles like this or more to share with everyone!

I appreciate the effort you took to write it. Please make more posts like this I will continue to support you. Thank you for sharing this article.

Absent is any reference to the fact that if no one can afford a home, no one will. It is a self-correcting system. The comment about only the most wealthy being able to afford a home, assuming yo have a free market, is erroneous. Of course, having investors like BlackRock scooping up homes doesn’t help, not does government interference.

I don’t know how much of a factor BlackRock is, but prices will flatten and start coming down when individual buyers get a brain and some self control

The author needs to re-visit Econ 101 as to the root cause of inflation. It is not due to pent-up Covid demand but rather due to the trillions of dollars the Fed’s have injected into the economy over the course of the last year or so.

If there ire more dollars in the system, your dollars are worth less. My question is what is BlackRock up to? Just simply making a good investment, or part of a coordinated attempt to manipulate the market?