Here is the third post in our new study series — Down payment download — detailing the monthly mortgage costs and benefits a persistent buyer achieves when prepared and shopping smart for sensible mortgage financing. This series is designed to educate a buyer agent for advising a prospective homebuyer on the costs experienced when owning their residence, emphasizing the necessary financial literacy required to take out a mortgage.

Every DRE licensed agent branding themselves for a reliable practice in referral home sales must understand and communicate the financial consequences of the down payment amount to every prospective buyer-client who will use mortgage funds to purchase their home.

Read the previous installment: Down payment download: 20% has your back

Why this matters: Real estate agents and brokers aiming to attract buyer clientele, whether by offering mortgage origination services themselves or competently guiding buyer-clients through the mortgage process, are duty bound to be transparent and provide sound advice on the largest and most confusing financial decision in most people’s lives.

Mortgage strategy driven by the down payment

A prospective buyer becomes best informed on the obligations of mortgaged home ownership when they understand the context driving the upfront and ongoing costs they must pay as an owner. None of these routine ownership costs are paid by a tenant — just rent.

But somewhere in between reasonably and ruinously expensive homeownership, when subject to a mortgage, is a homebuyer’s ideal price range. For a wage-earning tenant accustomed to maintaining a monthly budget, suddenly locking into a financial commitment for a mortgage lasting three decades with surprising additional expenses will make their head spin.

Tenants with a desire to own their residence someday are eager to learn when someone is willing to teach them. Here, the instructors happen to be the gatekeepers for entry into the world of real estate ownership — the buyer agents. They are licensed and expected to do just that: inform beginners about the move to homeownership.

As explained in this article, a buyer-client on their way to homeownership must recognize and understand their relationship to:

- an ideal price range;

- personal debt obligations;

- mortgage rates as affected by the down payment;

- an amortization schedule for the mortgage principal;

- implicit rent an owner-occupant receives;

- operating costs incurred; and

- various financial cost-cutting opportunities.

After an education in the examples narrated below, a buyer-client, guided by their agent, decides on the financial arrangements most suitable for their homeownership. An empowering and supportive buyer agent emphasizes what buyers need to do to take control of their mortgage funding for owning a home.

The balancing act of down payment and mortgage debt

A buyer looking at the total amount of their cash down payment as, say, $100,000, considers the maximum amount of mortgage funds their household income allows them to borrow at current mortgage rates. The ceiling for their mortgage borrowing capacity is based on an allocation of their household income, such as:

- 31% of household income spent on housing, as either the maximum rent or ownership costs; and

- 42% of household income expended on their total debt payments as the maximum debt-to-income ratio (DTI) to maintain solvency and a durable standard of living.

A household’s total debt includes the potential mortgage, as well as money owed on credit cards, auto loans, medical bills, student loans and other installment payment obligations. All this debt stacks up to show a mortgage loan originator (MLO) how much mortgage debt a buyer has the ability to repay. When payments on all types of household debt total less than 42% of household income, then a risk-adverse MLO is assured the borrower isn’t overextended.

The homebuyer dependent on mortgage financing balances the amount of capital they need to save up for a down payment with the amount of borrowed funds needed to own a home. The alternative is a buyer who dedicates a couple of decades saving up the capital necessary to purchase a home without the need for mortgage financing.

When owning a home purchased at an ideal price range of $500,000, with a 20% down payment and a $400,000 fixed rate mortgage (FRM) at 6.6%, the owner has a monthly principal and interest (PI) payment of $2,550. Additional carrying costs of owning this mortgaged $500,000 home includes estimated:

- property taxes of $450 monthly;

- property insurance of around $150 monthly; and

- maintenance or improvements at $150 monthly for a well-kept property.

However, property taxes, insurance premiums and maintenance do not build wealth but are the price paid annually for the privilege and economics of asset ownership. In contrast, the use of a capital asset, such as renting or an owner occupying a household is consumption, not an investment in a durable capital asset.

The mortgage payment together with the additional costs of homeownership total just over $3,300 monthly.

As for the DTI ratio, assuming total payments on all the household debt other than the mortgage are equal to or lower than 11% of the household gross income, this ideal price point of $500,000 fits a household with income of $10,600 a month or more.

Staying within an ideal price range assures a homebuyer they are able to transform their initial ownership position into continuously greater wealth by:

- building equity through mortgage amortization;

- providing implicit rent received as the owner-occupants; and

- avoiding excess mortgage fees with a 20% down payment.

Related article:

What’s amortization and what’s amortized?

Amortization is the monthly reduction in principal owed on the mortgage. Principal amortization is the result of the MLO’s accounting for each monthly payment by:

- first paying the interest accrued on the mortgage balance in the prior month; and then

- paying the remainder of the payment reducing the principal balance owed on the mortgage.

The amount of the monthly principal payoff increases with each following monthly payment. After, say, 30 years, the mortgage principal is fully paid with the final monthly payment, leaving the home free and clear of any mortgage debt.

On the other hand, the amount of interest in each payment decreases from month to month. Because the monthly mortgage payment stays the same, the amount applied monthly to principal reduction increases.

The monthly amount of principal amortization – payoff – is a benefit of ownership subject to a mortgage debt, second only to the benefit of implicit rent an owner-occupant receives. Monthly FRM payments store wealth in the property by constantly reducing the mortgage debt and simultaneously increasing the owner’s equity in the property, acting as a type of savings plan.

An amortization schedule for a 30-year fixed rate mortgage (FRM) displays each monthly payment as split up, allocated first to accrued interest with the remainder to principal reduction.

Amortization calculators allow a prospective buyer to compare the difference in the amount of monthly principal reduction between a 97% loan-to-value (LTV) FRM and an 80% LTV FRM on a $500,000 property price. Compare the principal reduction figures for the mortgages based on the different amounts of down payment for both the first and through the fifth year to see the pace of principal payoff.

An amortization example for the first five years

Consider the amortization schedule on our example $500,000 home with a 20% down payment of $100,000. A $400,000 mortgage is taken out to fund the balance of the price. While a minimum down payment of only 3% equals $15,000, the contrasting $100,000 down payment example adds $85,000 sourced from accumulated savings to achieve the 20% down payment.

The $400,000 mortgage is a fixed rate mortgage (FRM) amortized over 30 years at a 6.6% interest rate. The monthly payment is $2,550 — including interest and principal (PI) — a total annual sum of $30,600. The amortization schedule accounts for the first year of mortgage payments by applying $26,600 towards accrued interest and $4,000 towards principal reduction.

After five years of principal amortization, the buyer’s stake built up in the property is almost $25,000 plus the initial investment of their down payment. During that same five years, the buyer paid around $125,000 in interest.

Mortgage costs incurred for lacking 20% down

When a homebuyer with less than 20% down borrows funds totaling more than 80% of the price for the property, they pay not only significantly more interest every year but also pay at least a 0.6% default insurance premium on the entire amount of mortgage principal. Putting down 3% instead of 20% on a half-million-dollar home costs a buyer over $35,000 in extra interest and default insurance over first five years of the mortgage.

During the years of homeownership, the typical household experiences an increase in disposable cash. Whether the additional cash is achieved by reduced personal debt or decreased personal expenditures or increased household income, a wise financial decision is to voluntarily use excess savings to pay down the expensive mortgage principal. Here, the reduction in mortgage principal shortens the remaining amortization period — but the mortgage payments do not change.

Borrowed mortgage funds cost a very high interest rate to carry, a far greater cost than earnings of 3% on money stored in a savings account. Here, an initial large down payment and smart use of accumulated savings helps the buyer add to the cost-reduction advantage of amortization by making additional voluntary payments to the mortgage principal, thus reducing debt and building equity in the property faster. The rule here is “put your money towards the highest interest rate,” which prioritizes the mortgage rate against a smaller bank rate.

A down payment in hand is worth how much?

For the dual income household used in our example, to rent the property the new homeowners are buying would cost around $2,500 a month, the same as any tenant. This is about the same amount as their mortgage payment. However, the total amount of their expenses to maintain their homeownership of the $500,000 property exceeds their previous cost of housing without providing a higher level of amenities.

However, by choosing to own a home, the lump sum of a 20% down payment is best understood as an owner-occupant buying a 1/5 stake in the property. As a 1/5th stakeholder “partnering” with the MLO to raise capital needed to fund the price of the property, the owner-occupant is receiving implicit rent for their use of the property.

Again, implicit rent is the same amount as the market rental value of the property. As for the MLO’s stake in the property, the household use of the property as shelter is a benefit received in exchange for payment of interest and principal on the mortgage.

However, the MLO has priority for its claim of interest charges of around $26,600 the first year against the implicit rent the owner receives. The owner’s benefit of $30,000 annually in implicit rent for their occupancy leaves under $4,000 as earning on their 20% down payment — a 4% return on $100,000. This $4,000 share of the implicit rent is about equal to and in addition to the annual principal payoff on the mortgage debt which becomes stored in the equity of the property.

The homeowner’s receipt of the benefit of the property’s $2,500 rental value as the occupant, together with the mortgage principal reduction, is offset by all the operating costs of ownership. In addition to the mortgage payment, ownership expenses are incurred which a tenant does not pay (but the owner does), such as property taxes, insurance premiums, maintenance and more.

These costs total some $750 more than either the implicit rental value the owner-occupant receives or the mortgage payment. Most critically, the homeowner-occupant is:

- reducing principal debt each month which increases their wealth as equity built up in the property;

- shielding the value of their home as an asset which gradually increases in value over the decades due to consumer inflation;

- covering their home investment through ownership insurance from total loss to fire and weather; and

- providing the household with a stable and consistent standard of living that won’t become more costly beyond set FRM payments.

Related article:

A choice to save hangs in the mortgage balance

When delivering 20% down, a buyer avoids paying interest on additional borrowed capital and avoids premiums on default insurance charged as a percent of the mortgage principal balance as:

- mortgage insurance premiums (MIP) when taking out an FHA-insured mortgage; or

- private mortgage insurance (PMI) for a conventional mortgage.

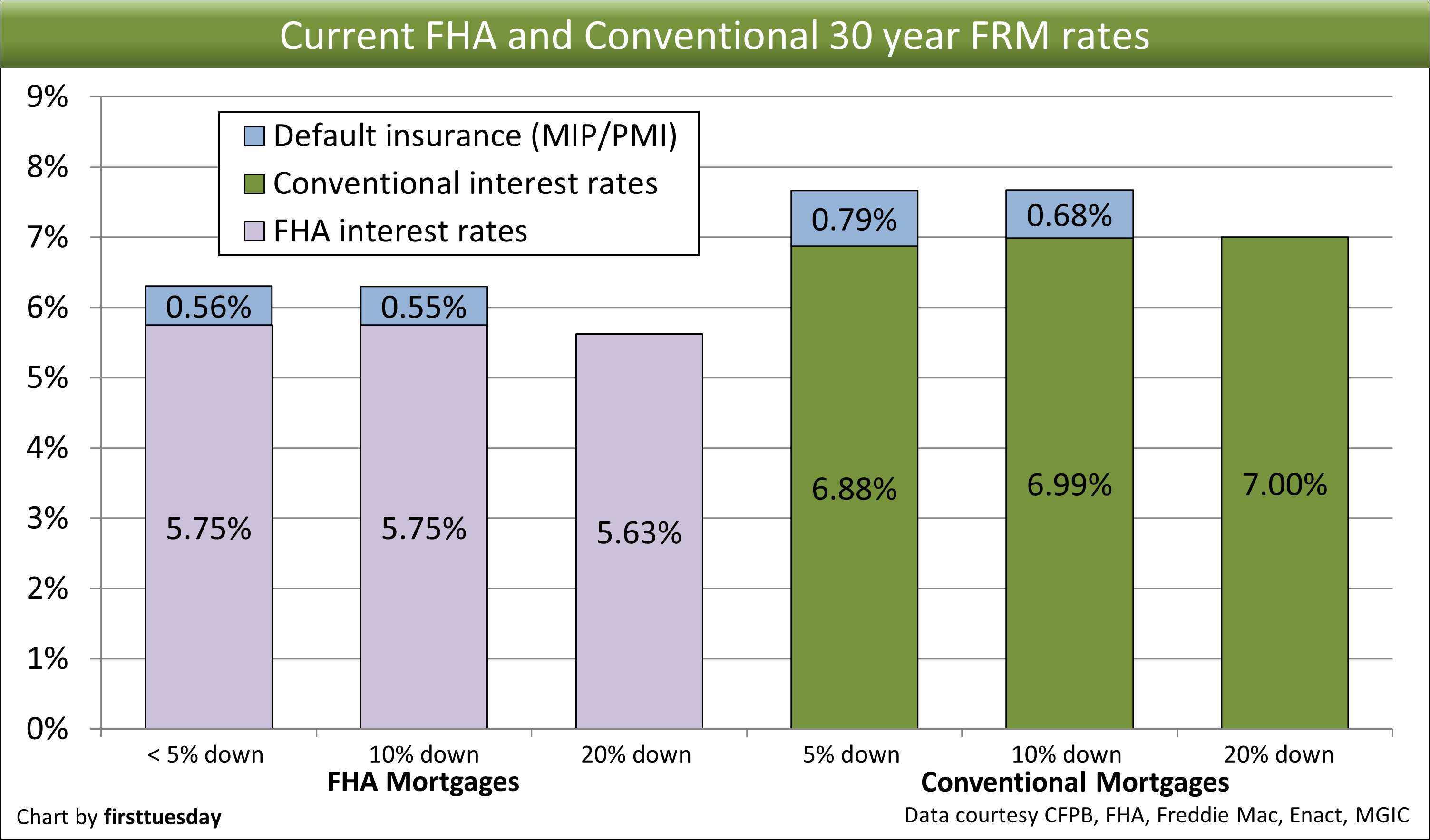

A buyer of a $500,000 single family residence with an average credit score of 700 can expect favorable interest rates from most lenders in the range shown in the chart below, according the most recent release from the Consumer Financial Protection Bureau.

Contrary to historical wisdom, a higher down payment only nets a lower interest rate when a buyer goes with an FHA-insured mortgage. A conventional mortgage does not benefit from a better rate when a buyer has saved up a 20% down payment. However, they do avoid the larger insurance premium MLOs require for smaller down payments, paid on the entire principal balance on the mortgage.

Chart 1  Chart 1 shows a snapshot as of April 2025 comparing the different loan-to-value ratios as interest rates remain basically the same with different LTV percentages.

Chart 1 shows a snapshot as of April 2025 comparing the different loan-to-value ratios as interest rates remain basically the same with different LTV percentages.

When the real estate market has a rise in for-sale inventory and buyers wait out the resulting drop in asking prices, the mortgage rates on new originations are usually lower, except for the added default insurance premiums. MIP and PMI rates do not change day to day like mortgage rates. Thus, again, mortgage originations of lower than 80% loan-to-value (LTV) are far more financially rewarding for buyers with a 20% down payment.

Mortgage points “buy down” the rate you want

Beyond seeing what competitive rates MLOs offer, ask your MLO whether the loan estimate already includes mortgage points — prepaid interest that a buyer provides (or the lender advances) at closing in exchange for a discounted, below par interest rate.

Lower monthly payments can be arranged on a mortgage origination by paying the MLO mortgage points upfront, also known as discount points.

The discount points buy down the rate of interest offered, by around 0.25% for every “point” paid to the MLO. A $400,000 mortgage originated when paying one point – one percent of the mortgage amount – reduces the interest rate charged from 7% to 6.75%, costing $4,000 paid to the MLO at closing in cash or added to the mortgage balance. This saves around $24,000 over the life of a 30-year mortgage.

One purpose for paying points is to allow the homebuyer to qualify to borrow more money. Often, the seller pays this charge to sell a property, effectively lowering the actual price of the property by the amount of this kickback from the seller.

A buyer putting down the bare minimum of 5% and taking out a 7% mortgage while passing on any mortgage points is losing even more when they intend to own the property long-term, the homebuyer paying around $28,500 in extra interest over the life of the mortgage.

However, mortgage points are beneficial even when borrowing less capital by making a larger down payment. Additionally, unlike other fees associated with buying a home, mortgage points are tax deductible in the year paid. They are, in fact, prepaid interest accruing over 30 years.

Mortgage points make no financial sense when buyers anticipate moving or selling before the interest saved recoups the cost of the point for a mortgage rate buy down. Use a mortgage points calculator to see your points stack up over the years, and how long before they break even. For the example above, starting at a 6.6% mortgage rate, one mortgage point begins saving the homeowner money after seven years in the home.

New homeowners determine the timeline for full recovery of the points paid by dividing the dollar amount of the points paid by the monthly savings in each mortgage payment at the reduced interest rate to see the number of months a buyer needs to retain ownership to break even.

Editor’s note – The last article in the Down payment download series covers a detailed, monthly cost comparison of homeownership with and without a 20% down payment.

Related article:

Tax Benefits of Ownership: the principal residence profit exclusion

{kind=link}