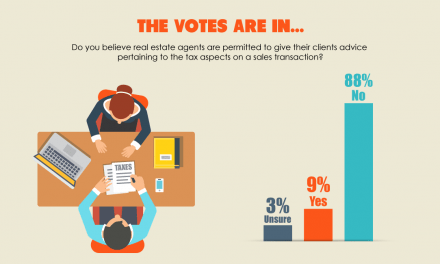

How many of your buyers ask you about the home mortgage tax deduction?

- All of them. (38%, 24 Votes)

- 10% or less. (30%, 19 Votes)

- 50% or more. (25%, 16 Votes)

- 25% (6%, 4 Votes)

Total Voters: 63

Political polarization is stunting the housing market recovery, a recent article from The Economist suggests. Drawing on similarities between the Netherlands and the U.S., the report links uncertainty about future government regulations to a retarded housing market.

In the Netherlands, the housing market has previously been heavily subsidized by its government in the form of the mortgage interest tax deduction (MID). However, growing division between political parties over housing policies has made many realize that their home financing hinges on the stance of whichever political party is currently in power.

Thus, Dutch citizens are hesitant to purchase a home until they are certain of what to expect in the form of government aid. Because Dutch buyers are stuck at this red light, so is the rest of their real estate market.

Like the Netherlands, the U.S. has experienced increased polarization between political parties. The result: uncertainty regarding future government housing policies. Because of this atmosphere, many employers and homebuyers are reluctant to make significant financial decisions until government mortgage financing policies are cemented, allowing them to conform business plans or purchases to new regulations. As in Holland, the result of all this political uncertainty in the U.S. has been an inert housing market.

first tuesday take

Buyer vacillation in the Netherlands may be the result of unpredictability in government policy, but this is not the case in the U.S. (especially California), as suggested by The Economist. There just simply isn’t a significant degree of awareness of how government housing policy works here.

For instance, a Cornell University study recently showed that only 6% of Americans understand that the MID is a government-subsidized social program. Government tax incentives for homeownership are not recognized by homeowners.

Worse, tax benefits of interest and property tax deductions are not publicized or used as marketing tools by agents in California. Many agents erroneously believe they may not address tax or legal issues when advising buyers about homeownership. However, they withhold their knowledge of tax benefits to the detriment of buyers.

Thus, these programs as understood present little motivation for buying. Unemployment and weak savings accounts currently impede home sales more than a possible government-retraction of homeowner tax deductions. As rents rise, tenants will likely figure it out for themselves. In the interim, agents lose out with fewer deals.

Related article:

The home mortgage tax deduction: inducing debt and stifling mobility

Were the MID actually cut, the event would certainly enhance activity in the real estate market. Currently, the only impact this subsidy might have on the real estate industry is to inflate prices, thus profiting lenders, builders, brokers and agents — not homebuyers, the beneficiary intended by these groups promoting retention of the tax deduction.

Were the MID cut, and home prices react as some brokers predict, the lowered prices would stimulate demand in the housing market and help shake it out of its comatose state.

Related article:

Unfortunately, the likelihood of U.S. housing programs being cut anytime soon is not great. The government’s cherished agenda to promote the American Dream via homeownership remains tightly clutched by legislators and homebuyers alike, despite the many reasons for its timely demise.

Related article:

Re: “Definite uncertainty” from The Economist

{kind=link}

We should do what Canada does. No interest deduction. It only helps the banks . Mortgage deductions encourages buyers to buy a bigger house than they can afford.