Why this matters: Declining DFPI licensee numbers, and the fees they charge, means the remaining individuals need to pick up the slack — with their wallets. DFPI licensees conducting mortgage-related activity will need to earmark $15,000 in their annual budget for DFPI assessments going forward.

Annual assessment increase

Mortgage lender and servicer licensees overseen by the California Department of Financial Protection & Innovation (DFPI) are required to pay an annual assessment to the Department, which is mailed on or before September 30 each year.

The DFPI issues California Residential Mortgage Lender and Servicer (CRMLA) licenses.

In 2025, the state increased the annual assessment. Previously, the assessment was a minimum $1,000, with higher amounts based on the number of loans originated, brokered and serviced.

Now, the annual assessment on CRMLA licenses is $3,000 for licensees with no lending, brokering or servicing activity, and $15,000 for licensees who conduct lending, brokering or servicing activity during the year. [Calif. Financial Code §50401(a)]

Licensees need to pay the assessment within 20 calendar days of the date the assessment is issued. Licensees who do not pay the assessment pay an additional fee equal to 1% of the assessment for each month or partial month the payment is delayed. [Fin C §50401(c)]

When a licensee fails to pay the assessment within 30 calendar days of the assessment’s due date, the DFPI may suspend or revoke their license. [Fin C §50401(d)]

The assessment is based on the mortgage activity report each licensee submits to the DFPI in March of each year.

Related article:

DFPI licensees jump ship

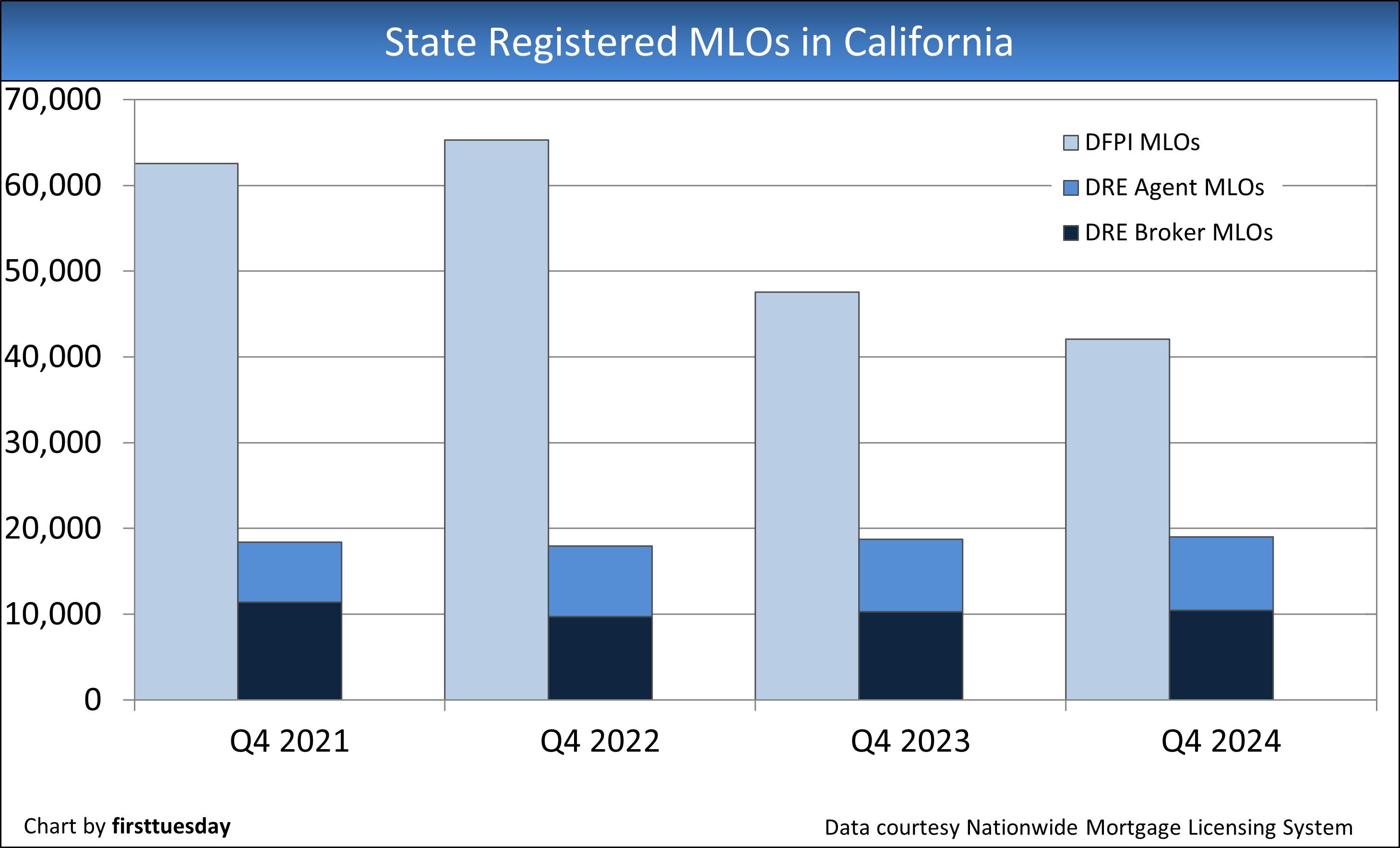

This sizeable assessment increase is no surprise, given the plunging number of DFPI licensees and the DFPI’s rather consistent operating costs. While the number of mortgage loan originators (MLOs) endorsed by the Department of Real Estate (DRE) has remained steady, DFPI licensee numbers have sunk by over a third since 2022:

The two paths to MLO endorsement under the DRE and DFPI are structured similarly. Both agencies’ applicants need to:

- complete 20 hours of NMLS-approved pre-licensing education;

- pass the nationwide SAFE Mortgage Licensing Act Exam provided by the NMLS with a 75% or higher;

- agree to a criminal background check; and

- complete eight hours of NMLS-approved continuing education (CE) annually.

Why would an individual choose to be licensed under the DFPI when they need to pay a stiff annual assessment?

The DRE endorsement is significantly more difficult to obtain than a DFPI license. DRE MLOs must maintain either a sales agent or broker license along with renewing their MLO license endorsement with the DRE. This higher standard empowers DRE MLOs with numerous other opportunities to offer fee generating real estate services not permitted by a DFPI license.

DFPI licensees work as a mortgage representative under either the:

- California Residential Mortgage Lending Act (CRMLA) [Fin C §§50000 et seq.]; or

- California Financing Law (CFL). [Fin C §§22000 et seq.]

In contrast, a DRE licensed individual with an MLO endorsement is authorized to also work for a CRMLA or CFL company and can make or arrange all types of mortgages. The reverse is not true. For example, a DFPI MLO licensed to service consumer mortgages applications representing a CFL company cannot negotiate business purpose mortgages under a CRMLA licensed company and cannot be employed by a DRE licensed broker to deal with members of the public without first being DRE licensed.

The more adaptable DRE licensee endorsed as an MLO also derives income for services as a real estate agent or broker. Thus, a DRE licensee endorsed as an MLO has a cushion of income available from other types of real estate services when a recession puts pressure on the state-licensed MLO population to seek additional income.

Related article:

{kind=link}