Special provisions for a note

Real estate professionals and their clients are closely watching interest rates as we head into 2024. When mortgage credit tightens and buyers look back wistfully at the low fixed rate mortgage (FRM) rates experienced in recent years, a seller hoping to locate a buyer amenable to the seller’s asking price needs to consider seller financing.

Buyer willingness immediately becomes apparent when the interest rate on the carryback mortgage is equal to or below the rates competitive lenders are charging on new purchase-assist loans. The lower the interest rate, the higher the price may be.

A note, sometimes called a promissory note, contains a borrower’s promise to pay the lender or carryback seller — the mortgage holder — the principal amount of the debt entered into, plus any interest. The note is a document and not the debt itself, but is evidence of the existence of a debt created in an underlying transaction.

In contrast, provisions in a trust deed, besides referencing the note and describing the real estate liened to secure payment of the debt, primarily address the maintenance and preservation of the mortgage holder’s security interest in the real estate. Together, the note and trust deed document is commonly called a mortgage. [See RPI e-book Real Estate Finance, Chapter 5]

Special provisions added to a note serve to:

- protect the mortgage holder against risk of loss resulting from late payments, early payoff or other defaults on repayment of the debt;

- comply with mortgage loan origination (MLO) rules for consumer mortgage transactions; and

- give the property owner payoff flexibility and limited liability.

Special provisions to be considered for inclusion in a note include:

- a prepayment penalty, when allowed [See RPI Form 418-2 §2.1];

- a due date extension [See RPI Form 418-3 §2.2];

- compounding on default [See RPI Form 418-1 §2.6];

- a final/balloon payment notice, when a balloon payment is included [See RPI Form 418-3];

- a grace period for payment and late charges [See RPI Form 418-1 §2.4];

- a payoff discount option [See RPI Form 418-2 §2.4];

- a right of first refusal on the sale of the note [See RPI Form 418-4];

- reference to a guarantee agreement [See RPI Form 418-5 §2.1];

- an exculpatory clause [See RPI Form 418-5 §2.2]; and

- governing law. [See RPI Form 418-5 §2.3]

Related article:

Guarantee agreement with a third party

To further protect the mortgage holder from risk of loss due to a default on the trust deed note, the mortgage holder may require a third-party guarantor to become liable on a call, by the mortgage holder, for payment of all amounts due under the mortgage, called a put option.

By guaranteeing the mortgage debt, a guarantor agrees to buy the note from the mortgage holder in the event of default, a legal process called subrogation or equitable assignment.

The mortgage holder has three types of third-party assurances:

- a co-owner’s signature on the note and trust deed;

- a co-signer’s signature on the note only; or

- a personal guarantee of the note by someone other than the borrower.

When a third party signs the note, the third party becomes liable for repayment of the note, greatly limited by anti-deficiency rules protecting:

- co-owners on any type of property or method of foreclosure; and

- non-owner co-signers on a trustee’s foreclosure. [Calif. Code of Civil Procedure §580(b)]

When the mortgage is guaranteed, a provision is included in the note to reference the separate guarantee agreement. [See RPI Form 418-5 §2.1; see RPI Form 439]

By referencing the separate guarantee agreement in the note, everyone involved is on notice of any additional security for the mortgage as described in the guarantee agreement.

Related article:

Form-of-the-Week: Guarantee Agreement for Rental or Lease — Form 553-1

Exculpatory clause

An exculpatory clause in a note converts a mortgage holder’s recourse debt into nonrecourse debt. [See RPI e-book Real Estate Finance, Chapter 41]

When the carryback mortgage is either separately or additionally secured by property other than the property sold, the debt evidence by the note automatically becomes recourse debt. Thus, the buyer providing other security needs to consider negotiating for inclusion of an exculpatory clause as a provision in the note. [See RPI Form 418-5 §2.2]

When an exculpatory clause is included in a note, the mortgage holder may not obtain a money judgment for any deficiency in satisfaction of the debt on a judicial foreclosure of the mortgaged properties. Thus, the exculpatory clause in the note provides the buyer with anti-deficiency protection in a judicial collection effort. [See RPI e-book Real Estate Finance, Chapter 40]

Related article:

Governing law

A lender or carryback seller involved in negotiating a mortgage with an out-of-state buyer needs to include a choice-of-law provision to assure judgments arising from disputes on the mortgage will be based on California law. [See RPI Form 418-5 §2.3]

When the state law to be applied is not agreed to, the state law applied will be based on the state with the greater interest in the result.

Editor’s note — The governing law provision has no impact on federal laws and regulations which pre-empt state laws.

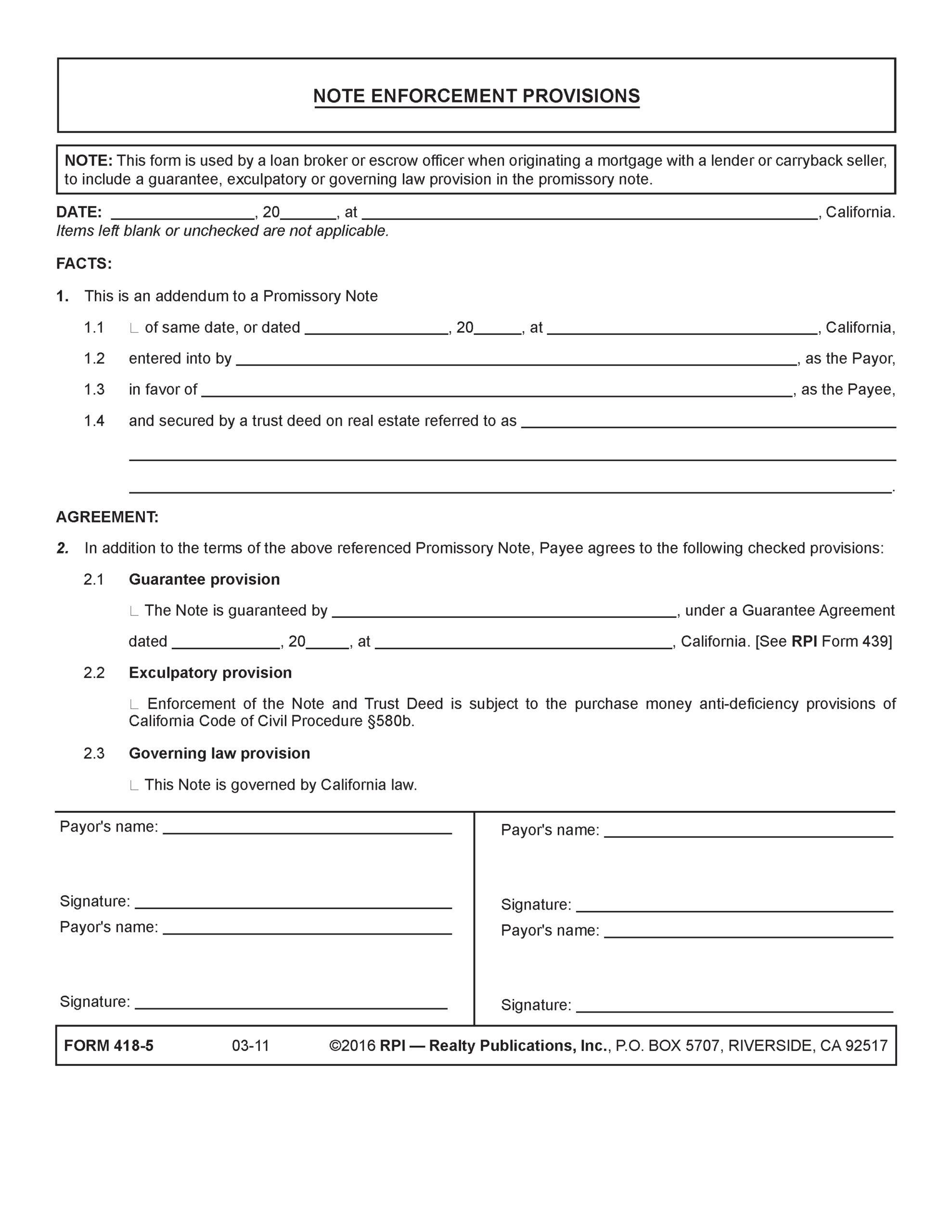

Analyzing the Note Enforcement Provisions

A broker or escrow officer uses the Note Enforcement Provisions form published by Realty Publications, Inc. (RPI) when originating a mortgage with a lender or carryback seller. The form allows the broker or escrow officer to include a guarantee, exculpatory or governing law provision in the promissory note. [See RPI Form 418-5]

The Note Enforcement Provisions includes:

- a guarantee provision [See RPI Form 418-5 §2.1];

- an exculpatory provision [See RPI Form 418-5 §2.2]; and

- a governing law provision. [See RPI Form 418-5 §2.3]

The form is attached as an addendum to a promissory note.

Related article:

The due-on waiver

A typical carryback sales transaction involving an existing mortgage is structured as either:

- a regular second mortgage carried back by the seller when the existing mortgage holder consents to the conveyance of an interest in the property and the recording of a carryback second mortgage by waiving the lender’s due-on clause in exchange for an assumption fee and modification of the note by the buyer, called a formal assumption; or

- an all-inclusive trust deed (AITD) and note, or another wraparound security device such as a land sales contract, with the underlying mortgage holder consenting to the conveyance to the buyer and the carryback AITD by waiving their due-on clause in exchange for a modification of the note and payment of fees by the seller — all in lieu of the buyer’s assumption of the mortgage, an activity labeled a reverse assumption.

After the mortgage holder consents to the carryback sale and escrow closes, future events beyond the carryback seller’s control can again trigger the due-on clause.

Without the mortgage holder’s prior written waiver of their due-on enforcement rights triggered by future transfers after closing a carryback sale transaction, the mortgage holder can call their mortgage due on a later transfer of the buyer’s interest in the property. [See RPI e-book Real Estate Finance, Chapter 26]

Related video:

With some exceptions for a principal residence, a transfer subject to due-on enforcement rights include a:

- resale;

- further encumbrance;

- lease for a term greater than three years;

- court ordered transfer;

- foreclosure; or

Related video:

A written waiver of the mortgage holder’s future enforcement of the due-on clause bars the mortgage holder from calling the mortgage due so long as the carryback mortgage remains without a reconveyance. Thus, the waiver protects the carryback seller as long as the seller has any interest in the property.

The waiver agreement assures the carryback seller they can protect their security interest in the property without interference from the underlying mortgage holder, which will otherwise take place when FRM rates trend higher. [See RPI Form 410]

To best protect the seller’s security interest created by the carryback trust deed, the seller needs to have the mortgage holder waive their right to call the mortgage:

- on the conveyance and further encumbrance of the property on the close of the carryback sale;

- for as long a period as the carryback mortgage remains of record; and

- on the carryback seller’s reacquisition of title to the property when the seller completes a foreclosure on the property or accepts a deed-in-lieu of foreclosure.

To be enforceable against the mortgage holder, the waiver agreement needs to be in writing as do any other commitments or promises made by a lender. [12 Code of Federal Regulations §591.5(b)(4)]

Related video:

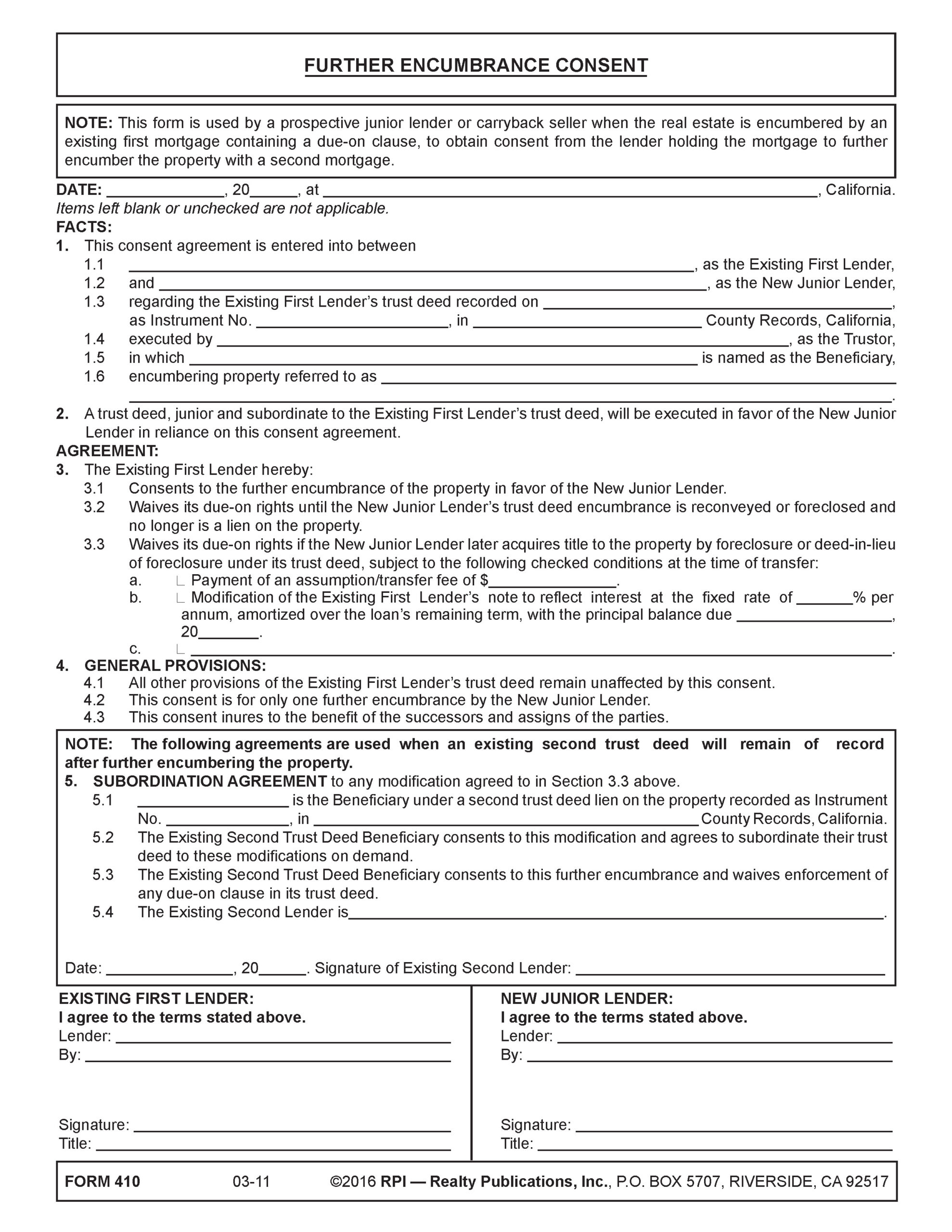

Analyzing the Further Encumbrance Consent

A prospective junior lender or carryback seller uses the Further Encumbrance Consent published by RPI when the real estate is encumbered by an existing first mortgage containing a due-on clause. The form allows the junior lender or carryback seller to obtain consent from the lender holding the mortgage to further encumber the property with a second mortgage. [See RPI Form 410]

The Further Encumbrance Consent includes:

- facts covering the identity of the existing first lender, the new junior lender, the lender’s trust deed and its trustor, beneficiary and property address [See RPI Form 4101];

- the existing first lender’s consent in the agreement to the further encumbrance of the property in favor of the new junior lender, waiving the lender’s due-on rights in exchange of their exaction of a negotiated assumption fee [See RPI Form 410§3.1-3.2];

- general provisions stating the existing first lender’s provisions remain unaffected, that the consent is for only the one identified further encumbrance by the junior lender and that successors and assigns of the parties are controlled by the consent [See RPI Form 410 §4];

- subordinating language [See RPI Form 410 §5]; and

- signatures of the existing first lender and new junior lender. [See RPI Form 410]

Editor’s note – Expect stonewalling by the lender when negotiating a waiver agreement, as it is in to their financial benefit to stall when others are eager to close a deal. Some mortgage holders may simply call when the owner has entered into an agreement to sell or grant an option to buy since the buyer then has an equitable ownership interest in the property.

Related Client Q&A:

Want to learn more about receiving and splitting broker fees? Click the image below to download the RPI book cited in this article.

{kind=link}

Very informative. Understanding the details of consent and enforcement provisions is essential for managing risk and avoiding disputes in complex financing transactions.