Why this matters: The slow moving 10-year Treasury note rate is the base for setting the 30-year FRM rate and capitalization rate which control what a homebuyer can pay to purchase a home and an investor will pay to acquire an income property. A buyer agent with an awareness of the long-term rise and fall of the 10-year treasury note rate and its inverse consequence on property values is best able to guide buyer-clients with data-driven advice in uncertain times.

Up, up and away

The 10-year Treasury note held at 4.11% the week of October 3, 2025. A steady pace of decline in the 10-year T-Note rate took place in 2025 beginning at 4.63%. The 10-year T-Note rate averaged an anomalous rock-bottom 0.89% during the 2020-2021 pandemic period as the T-Note became the ultimate safe haven until investment opportunities returned.

The rise and fall of long-term interest rates follow a different life cycle than the typical business cycle and patterns of short-term interest rate movement.

Currently we are experiencing a rising trend in the long-term rate cycle which began when rates bottomed in January 2013 (interrupted briefly by 2020’s pandemic interference). We are now in a half cycle of rising long-term rates. So, expect around 20 more years of rising 10-year T-Note rates, broken up by transitory recessions.

Rising long-term rates tend to dampen home price growth until rate increases end. As long-term rates trend upward producing a sequential rise in FRM rates, buyer purchasing power is continually reduced while capitalization rates for evaluating income property increase. Both cause property prices to stagnate or decline.

Critically for ubiquitous 30-year FRM originations, MLOs use the 10-year T-Note rate plus a default risk factor to determine a homebuyer’s rate for the FRMs they originate. The difference between a mortgage note rate and the 10-year T-Note rate represents the lender’s risk premium.

The purpose for this risk premium is to cover potential losses due to mortgage defaults. Further, a greater risk of loss exists with LTV ratios for less than a 20% down payment. Here, government and private mortgage insurance (MIP and PMI) cover the added risk presented by a low down payment at an additional hefty cost to the homebuyer.

Historically, the risk premium spread between the 10-year T-Note rate and the 30-year FRM rate is 1.5%. However, this spread has widened to nearly 2.5% in 2025, significantly above the historic risk premium. Mortgage investors perceive additional losses in the coming recession due to job losses, declining home prices and an increased pace of foreclosures. Today’s generous spread indicates lenders are also padding their risk premiums in anticipation of future rate increases.

Updated October 7, 2025.

Chart updated 10/7/25

Chart updated 10/7/25

| January 2025 | January 2020 | January 2012 | |

| 10-Year Treasury Note Rate Average | 4.63% | 1.76% | 1.97% |

Bond market cycles

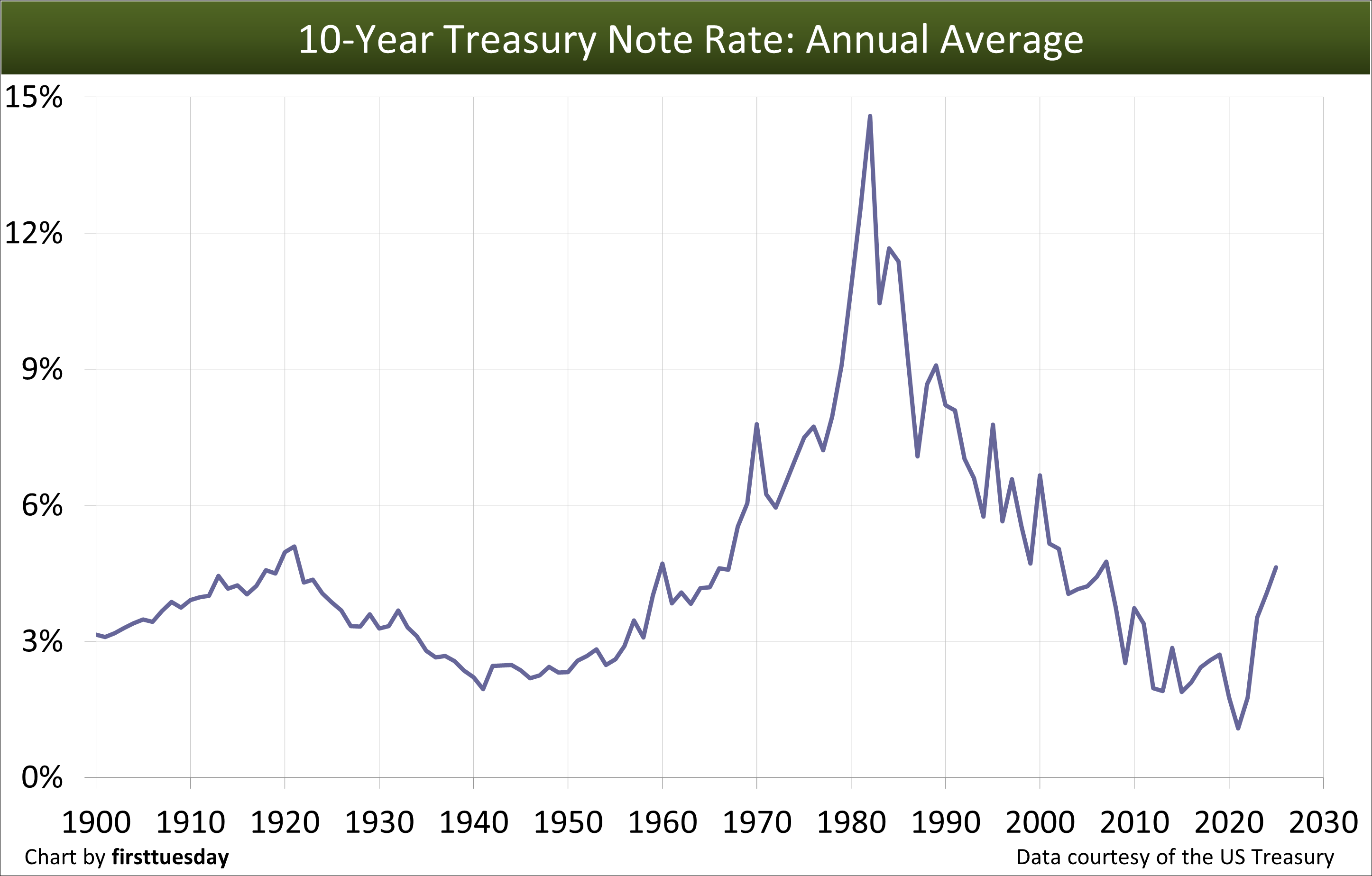

The average annual 10-Year Treasury note (T-Note) yield since 1900 is shown on the chart above. As demonstrated, interest rates on the 10-Year T-Note have shown an overall decline since 1980. Now, the T-Note rate is steadily picking up after the low point in 2013, with the economic tsunami of 2020 and 2021 being a pandemic aberration now gone.

We now see that 1950 marked the beginning of what became a 60-year rates cycle ending in 2013, comprising approximately 30 years of rising rates followed by 30 years of falling rates. This cycle roughly mirrors the 60-year period prior to 1950, during which interest rates peaked in 1921.

As we make our way through the current iteration of the 60-year rate cycle, firsttuesday expects another slow upward run in rates for 25-30 years following the bottoming of rates in 2013 before a reversal into rate declines, as happened in the 1983 rate pivot. In 2020, the interest rate on the 10-Year T-Note dropped as low as 0.89%. But this dramatic dip quickly returned to the long-term rising trend by 2022.

Consider also that 30-year FRM rates historically moved in tandem with the 10-year T-Note at a 1.5% spread. However, this 1.5% spread, a risk premium not needed for T-Notes, was elevated following 2012. Mortgage loan originators (MLOs), cautious about the future economic outlook, padded their risk premiums. In October 2025, this spread was up to nearly 2.2%, indicating lenders are nervous about the years ahead.

Looking ahead to 2026 and the years beyond, 10-year T-Notes will continue their long-term rise, with periods of slight downturns during business recessions. The last three half-cycles in bond market rates have been extremely regular, as confirmed by Longview Economics. A 27-year downtrend in rates (1922-1949), was followed by a 32-year uptrend (1949-1982) and another 31-year downtrend lasting to 2013. And now, an uptrend path beginning in 2013 for the current 30-year half-cycle.

While the regularity of the pattern for 30-year half cycles is considered coincidental (they easily might have been forty years, or twenty), precedent establishes that bond market rate changes are gradual and more persistent than, say, changes in the stock market or commodities. Again, real estate pricing tracks with mortgage rates, but in a reverse direction.

Related article: Current market rates

Interest rates and asset pricing

During the half cycle of rising long-term interest rates from 1949 to 1982, the wealth of investors increased even as interest rates rose. Housing construction and employment were strong with individual standards of living increasing as well. This prosperity was due in part to a burgeoning military-industrial complex and massive interstate highway construction as well as the GI bill for free higher education of veterans. The American Dream of jobs, cars and homes for all was in full bloom during this period.

For the housing market today, rising mortgage rates — or even static but high mortgage rates — mean short-term profits in real estate through price increases are unlikely without adding value from improvements. Rental income over the long term will take priority in the financial management of capital assets.

To perk up consumer spending in the 1990s, the notorious “Greenspan Puts,” in Federal Reserve monetary policy simply dropped interest rates further following each downturn in the economy. This cannot be repeated during a trend of rising interest rates to artificially generate profits in any asset market — commodities, stocks, bonds or real estate. Again, mortgage rates are inextricably tied to bond market rates, not the federal reserve short-term inflation-fighting rate.

The pandemic was an exception outside of the normal business cycle. Then, the bond market for funding mortgages collapsed and the Federal Reserve as the lender of last resort funded all residential mortgage origination during the 2020-2021 pandemic period. Every increase in bond and mortgage rates meant a decrease in a homebuyer’s purchasing power — payments for setting the amount they can borrow are limited to 31% of household income — and an increase to the earnings of the rentier class.

Thus, a buyer experiences a decrease in the amount they can pay for a home. Less money borrowed by homebuyers means sellers receive lower prices for their properties when they need to sell.

Of course, this annual decline in buyer purchasing power is offset in actual (nominal) dollar terms from year to year by the Fed’s monetary policy goal to maintain annual consumer inflation around 2%. Consumer inflation is the driving force increasing wages from year to year to catch up with rising prices.

Related article:

Using the yield spread to forecast recession and recovery conditions

Interest rates in the modern day

While FRM rates hit historic lows in 2020, FRM rates fully recovered by the end of 2021 and will continue to rise for around two more decades. As the consequences of long-term interest rate increasing becomes understood by buyers, agents will quickly learn to cope with an unfamiliar set of investment and pricing challenges, such as reversals:

- in the direction of income property multipliers and capitalization rates;

- requiring confirmation of actual rents and expenses;

- in the length of holding periods necessary for profits to develop; and

- by use of due-on provisions to adjust mortgage rates.

The key lesson for acquiring real estate in the upcoming years is to price property for its inherent rental value, not relying on profits from a resale as a return on investment. Those who buy property for speculative gain, not rental income, will see as little success in gains from a flip as those who invested in the real estate market from 1950 to 1980, when mortgage rates moved slowly, steadily upward until they exceeded 18%.

Related article:

Changing dynamics in the years ahead

In the decades before 2020, it was possible to purchase a parcel of real estate, vacant or improved, and take a profit much greater than the rate of consumer inflation, merely by owning that parcel for a short period of time. The financial conditions for this option no longer exist.

Going forward, prices may rise abnormally in narrowly defined locations enjoying a population density explosion. Normally, pricing is dampened by constantly rising mortgage rates which keep prices from rising faster than the rate of consumer inflation, including increases in rental income.

The negative pricing effects of increasing mortgage rates are, in part, counterbalanced by demographic conditions requiring more permissive zoning. When a community’s attractiveness causes property prices to rise beyond the rate of consumer inflation, it is the local government which must permit the density of their population to increase, best achieved by reduced restrictions on residential construction. When they do not, buyers suffer the consequences of an asset-inflation bubble-price distortion.

In the present renewed paradigm of rising 10-year T-Note rates, the buyer’s plan for success includes:

- patience in property selection;

- aggressive due diligence research;

- forward-looking capitalization rates; and

- a long-term commitment to real estate ownership as a collectible.

Related article:

{kind=link}

Insightful commentary on a topic that affects virtually every portfolio. The diversification benefits you outline are supported by decades of empirical evidence. More investors should be paying attention to this.

“But this cycle’s days of steadily decreasing interest rates, accompanied by steadily falling rents, producing ever increasing prices and profits (and §1031 hysteria) have run their course to the bitter end.”

Steadily falling rents? Really! You need to proofread your articles.

Jack,

Thank you for pointing out this potentially confusing sentence. We have clarified, referring to this last cycle rather than the one we are currently in during 2019, in the copy above.

Best,

Editorial Staff

12-13 From the observation data above, it was seen that the longer synthesis time generated aurantiol with greater refractive index, density, and specific gravity. This was due to the increasing quantity of methyl anthranilate in the aurantiol product, in which methyl anthranilate had the biggest density. So it can be concluded that the duration of synthesis time was directly proportional to the refractive index, density and specific gravity of the aurantiol product.

This article leaves out several issues. For example, the article does not take into consideration the fact that the world today, thanks to the internet is now based on a world economy and does not include the current economies of China, Russia, Japan and all of Europe. Plus, the article also leaves out discussing inflation and the national deficit. When the current administration is no longer in office the national deficit is predicted to be over $20, TRILLION and climbing. The current inflation rate is actually 11.5% and when the Carter administration left office inflation was 14% and 30 year interest rates were at 18%. Plus, prior to the Clinton administration, the 30 year loan was tied to the 15 and 30 year bonds. During the Clinton administration, interest rates were changed to the short term 10 year loans.

I believe that the we are about to see interest rates rise like they did during the Carter administration and this is based upon the deficit and the rate of inflation. The only way that I believe that hyper inflation and the deficit won’t enter into this scenario is if a major war is started. According to the fact that the war on terror is once again getting out of control and our military is once again the size it was prior to World War II, and the fact that former Russian dictator Gorbachev said last week as reported on Fox News, that Putin is preparing for a nuclear war. According to defense one.com, the U.S. Department of Defense is in the process of making plans for World War III. Therefore, there is a very good probability that hyper inflation will not happen due to the possibility of war.

I would love to see the article rewritten with these issues taken into consideration with the all of these issues brought into consideration.

Interesting!