This article examines how long-term property investors will use 10-year Treasury Note trends to determine a suitable cap rate.

Climbing interest rates turn the market on its head

The word on the streets in 2022 is interest rates, and specifically, long-term rates

After hitting a record low in 2021, mortgage interest rates have rebounded at a startling speed, sending the purchasing power of property buyers into the basement. Sellers are getting the message.

In terms of purchase-assist funding, the jump in mortgage interest rates alone has slashed the amount of mortgage money available to a typical homebuyer by 31% compared to a year earlier as of Q3 2022.

Today’s rising mortgage rate environment reflects a consistently worsening home values situation for sellers of property in markets dependent on prices paid by highly leveraged homebuyers and investors.

Homebuyers qualify for a maximum mortgage amount based on their savings for a down payment and incomes available for mortgage payments — which shift gradually over years — and interest rates — which shift rapidly on a daily basis.

Thus, any rise in mortgage rates instantly cuts the amount leveraged buyers can borrow. Thus, the price they can pay for a home — and the price a seller can expect — is reduced.

Related article:

Press Release: Buyer Purchasing Power Index plummets in Q3 2022

In a cyclical reversal, California home prices began to decline on a monthly basis in July 2022. Still, as of August 2022, average California home prices are 11%-to-16% higher than one year earlier. But this annual spread is narrowing rapidly, on course to turn negative by 2023.

Rising rates in 2022 have forced a reconsideration on homebuyers. In the pivot, property prices started falling back in June 2022 as sellers reacted to their reversal in fortunes by reducing asking prices to attract the few remaining buyers. It’s a repositioning buyers and sellers (and real estate professionals) will need to get used to.

The rate cycle resumes its upward course

Judging from a historical perspective, interest rates of all types — short- and long-term — display a decades-long rate cycle lasting roughly 60 years.

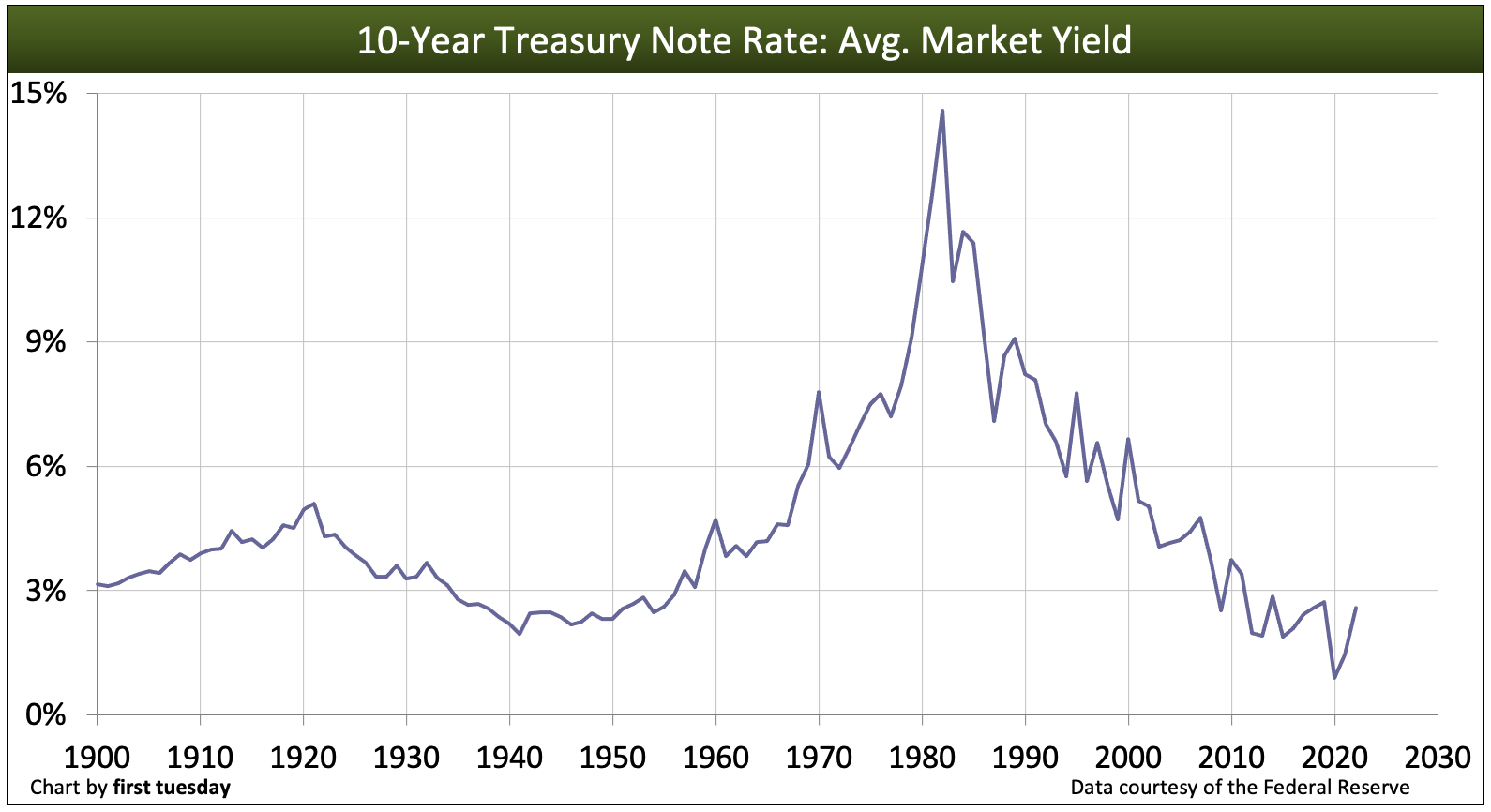

Here, we see the annual average 10-year Treasury (T-) Note rate going back to 1900. This rate is important for real estate, as mortgage rates move in tandem with the 10-year T-Note rate at a stable rate spread.

These long-term interest rates first peaked in 1921, falling into the late-1940s and rising again to a peak in 1979. Interest rates then dropped until bottoming in 2012.

Editor’s note — While mortgage rates hit new lows in 2020-2021, this was a momentary divergence from the broader interest rate cycle, influenced solely by the disruptive Pandemic Economy. In 2022, interest rates reset and resumed their upward course.

While the regularity of this pattern of 30-year half cycles is coincidental (they very easily might have been forty years, or twenty), precedent establishes that bond market rate changes are much slower and more gradual than, say, changes in the casino-style stock market arena.

Going forward, the overall trend for the next couple of decades will be up, though rates will continue to bump along from month-to-month. Because we know how interest rates impact prices, we know future property prices will be dampened by these higher rates.

Savvy investors acquiring income property will also use knowledge of the upward passage of future interest rates as they set the value of prospective real estate investments under consideration.

Cap rates adjust, too, in trend

In sympathy with rising long-term interest rates, investors need to alter their forward strategies for valuing income property. Contrast this with the lethargic valuation analysis employed during the past three decades of declining interest rates, which ended with a long-term interest rate pivot in 2012.

Today’s need for a change in valuation strategy employed by an investor is complicated by the near total loss of expertise in the brokerage and investment communities for using an income property profit and loss statement (P&L) and selecting a capitalization (cap) rate to set the price paid.

A property’s P&L is the source of the property’s net operating income (NOI). Seller’s agents use the P&L to divine a “seller’s cap rate” based on the seller’s asking price. Conversely, a buyer’s agent and buyer select an appropriate cap rate to calculate the property’s market value based on a due diligence NOI.

In the past half cycle of declining interest rates, the primary source of earnings for ownership turned out to be profits taken on a resale or further encumbrance of the income property (refinancing) — not the property’s annual NOI. The reason: declining interest rates (and cap rates) drove prices up to culminate in windfall profits for assets owners, called the “Fed Put” which has now been retracted.

Today, the primary source of earnings on income property has been repositioned with the pivot into the current half cycle of rising interest rates. Thus, the primary source of earnings from owning income property has moved from expecting future price increases to focusing on the NOI generated during ownership.

As a result, profits to be taken on a sale are smothered by the present decades-long trend in rising interest rates now underway, likely to continue into the 2040s.

This reset is reminiscent of the intense refinement of property management required to maximize net income in the 1960s and 70s, years of rising interest rates. In those decades, a home was primarily viewed as shelter and a buildup through amortized mortgage payments of savings for retirement — not an investment capable of being flipped at an inflated price for a profit. Further, the 1990s and 2000s were the days for vagabond homeownership of fix-and-flip to avoid profit taxes from one sale after another which generated turnover, a broker’s delight.

Calculating the cap rate

When a seller’s agent initially markets an income property for sale, the cap rate is presented as the annual yield from rental operations in relation to the seller’s asking price. Conversely, the buyer’s agent applies a cap rate stated as a percentage of the capital to be invested — the annual yield on the price paid. The cap rate is exclusive of any profit the buyer might expect on a future resale at a higher price.

In practice, the lower the cap rate the, greater the buyer’s expectation of a profit on a resale or further encumbrance. That works in an environment with a future of declining long-term interest rates — but not in today’s rising rate environment.

To clarify, the cap rate is unrelated to:

- asset appreciation — due to local demographics such as personal income and population density;

- asset inflation — driven by external catalysts such as declining long-term interest rates or increased price level of construction, not consumer price movement; or

- price influencers which might coincidentally enhance value during ownership, such as the supply of comparable property, community infrastructure investment, crime and zoning.

For the seller’s agent, the cap rate is determined by dividing the property’s NOI by the asking price.

For example, consider a property with an NOI of $75,000. The seller’s asking price is $1.3 million. The property’s cap rate is 5.8% (75,000 / 1,300,000).

Related article:

California’s commercial property shortage is making investors desperate

For a buyer’s agent and their investor-buyer, a well-advised cap rate is a composite of:

- the rate of long-term consumer inflation to annually recover the lost purchasing power on the price paid for the property;

- a risk premium, set sufficiently higher than the risk-free real rate of return (which when added to the long-term rate of consumer inflation is the 10-year T-Note rate), to cover the owner’s time and effort for operational oversight and uninsurable risks unique to the property such as location, zoning, construction, cyclical tenant demographics, periodic recessionary rent levels, tenant turnover rate and vacancies; and

- a rate for cost recovery of a portion of the price allocated to improvements, based on the age and condition of the property.

An investor never wants to be caught having applied a cap rate that will be less than the interest rate for purchase-assist mortgages needed to fund a buyer on a resale of the property. In past decades when mortgage rates were trending down, investors were not concerned about mortgage rates (except to refinance and increase earnings). Downward trending rates fortuitously created windfall profits through a general increase in property prices — the put. But that is not the mortgage rate environment since 2012 (absent the temporary, pandemic-induced interest rate plunge in 2020-2021).

Stated another way, the cap rate must always be greater than the interest rate for a fixed-rate mortgage attainable on the property, now and in the future years of ownership. While the spread between the 10-year T-Note rate and the 30-year FRM rate for a single family residence is currently around 2.5%, commercial property mortgage rates general run around 1 percentage point or higher for the best purchase-assist transactions. Thus, the best mortgage rate for class A commercial property is 8%, but fast ranges upward to 10% or more for other properties.

Editor’s note — ARM rates are not a comparison for fixed rates. ARMs reflect short-term lending rates, not long-term investment rates. In the age of rising rates, an ARMs when adjusted act like a tax increase on rental income.

The price paid today using a cap rate based on past rate trends and recent historically low mortgage rates will in real terms produce a long-term loss on a resale.

The ideal cap rate spread for 2023 and beyond

Like mortgage rates, cap rates for buyers of income property are set by adding a premium rate — a spread — to the rate earned on a risk-free investment of like duration. For both the cap rate and the mortgage rate, the relevant risk-free investment is the 10-year T-Note.

Thus, the 10-year T-Note rate becomes an index figure, a base rate to which an appropriate premium rate is added to cover ownership risks foreseeable in an income property. ARM rates are also adjusted in this manner.

The calculation setting the premium rate includes the buyer’s exposure to risks inherent in a particular income producing property, which risks are not present in a coupon clipping 10-year T-Note investment.

Further, both the 10-year T-Note rate and the risk premium spread rate — which collectively set a property’s cap rate — vary; one due to expected consumer inflation and bond market conditions —and the other due to a property’s conditions which affect the NOI it generates.

Viewing the historical 10-year T-Note chart above, you can expect this index figure as a base for structuring a buyer’s cap rate to rise gradually over the next decade from today’s rate of 4% to a higher level by the late-2030’s.

The premium spread portion of the cap rate structure covering risks to income, property value and ownership endemic to the property starts at a minimum of 5%, ranging higher for most properties. This calculation is comprised of:

- a real estate asset risk recovery premium of 4%-to-7%; and

- 1%-to-2% as a return of the investment needed to recover the portion of the price allocated to the improvements on the property which, over time, will need to be replaced either component by component, or as a renovation or by demolition and replacement — the age and obsolescence issue.

Thus, today’s long-term property investor needs to consider a cap rate of at least 9% for a well-maintained, code compliant Class A structure in a stable and enduring market location which is and will experience increasing population density.

As 10-year T note and mortgage rates rise, sellers of income property will no longer get away with pricing at low cap rates. For these years now and following, an income property buyer’s motivation will shift from expecting earnings from profit on resale to looking more acutely into the annual flow of earnings from rental income.

Investors who continue to evaluate income property based on yesterday’s compromised low cap rates will in real terms produce a long-term loss in property value when they refinance or sell.

Related article:

The lull before the storm: 16 factors set to rise with interest rates

{kind=link}

Mr. Flip is a fun acrobatic game where you control a character performing jumps, spins, and precise landings to overcome challenges. The gameplay is simple but extremely addictive!

For players who want a faster way to improve their setup, buy blade ball fits naturally into marketplace content that focuses on convenience and quick access. On StarPets, the idea is to keep the buying process simple, clear, and useful for people who do not want to waste time searching across multiple places. This kind of wording works well because it feels direct and matches real purchase intent. It also supports content that aims to be practical, game-focused, and easy to understand.

Depuis quelque temps, je pense à une meilleure machine à café, mais ça n’avance pas vraiment. Un collègue a récemment mentionné. Après quelques tours plus calmes, j’ai augmenté ma mise et j’ai eu un bon gain. Il a apporté une jolie contribution à la machine à café. Le site fait une impression solide, la navigation est claire, et l’accent mis sur les paiements mobiles locaux est intéressant. C’est bien qu’il y ait des conditions spéciales.

Je viens de la région Grand Est et j’apprécie les services numériques bien conçus. spinmama m’a agréablement surpris par son fonctionnement fluide et sa navigation facile. Je m’y rends lorsque j’ai envie de changer de rythme et d’ajouter un peu de dynamisme à ma soirée. Je l’utilise régulièrement, car cette plateforme allie commodité, stabilité et format de loisirs intéressant.

Your blog has garnered considerable genuine interest. I understand why, as you did an excellent job making it engaging. I sincerely appreciate your efforts.

Good analogy. Thanks to your article, I understand the fundamentals of two concepts.