California's 2018 Tax Landscape

California's 2018 Tax Landscape

Individual Tax Brackets

Individual Tax Brackets

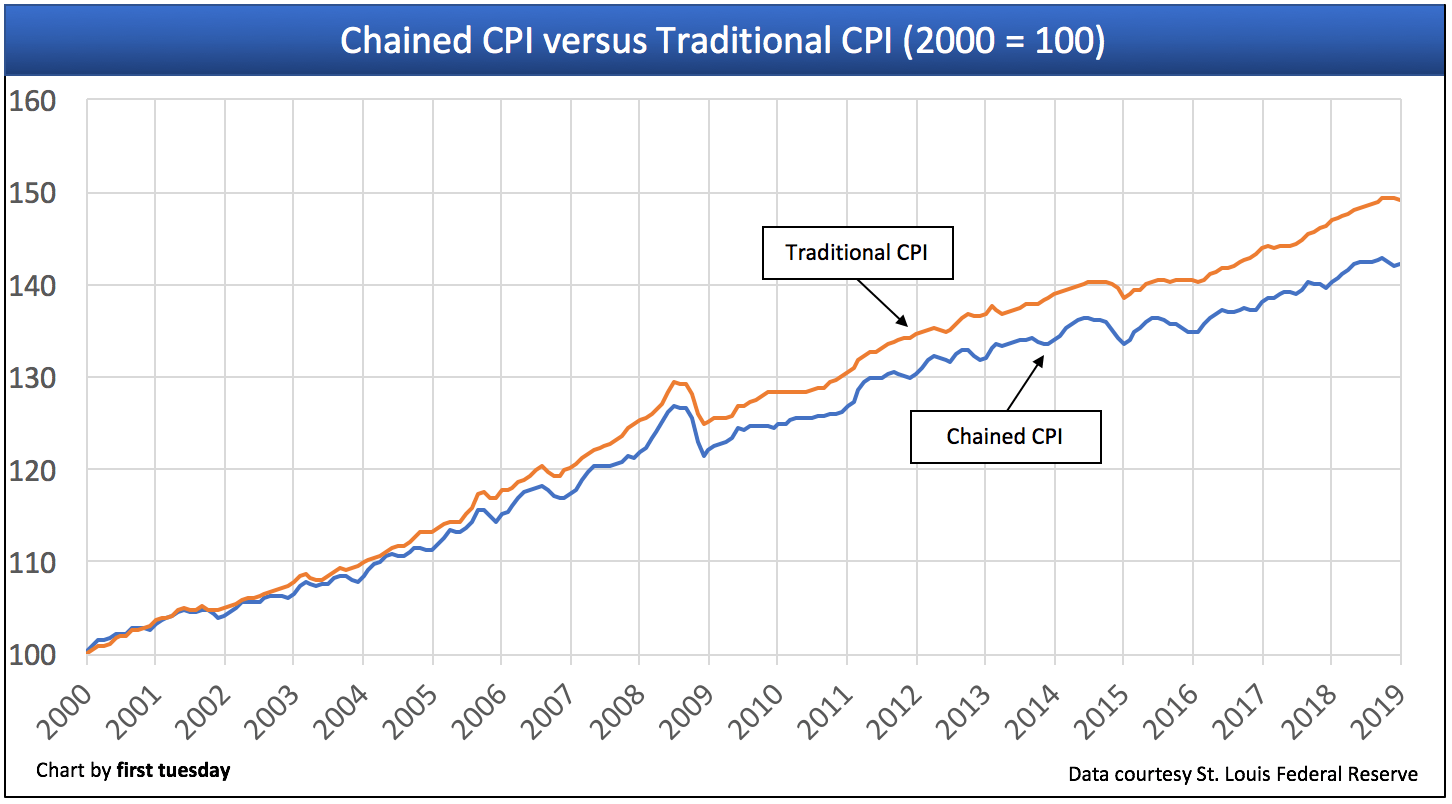

Chained CPI: why what looks like a good deal now will bite in the future.

Additional money paid by taxpayers over the next decade under new CPI measure

Income brackets have changed. More importantly, the IRS will now measure inflation differently when making adjustments to these brackets in the coming years. This essentially equals a tax increase over time, as peoples’ incomes will increase more quickly than the consumer price index (CPI) measure now included.

The new CPI measure is chained CPI. The difference between the new measure and the way inflation was previously measured is the new measure accounts for consumer substitution patterns. Consider the example used by the Bureau of Labor Statistics (BLS), which publishes the chained CPI figure. When the price of beef rises, the traditional form of CPI would use this higher price of beef to increase the CPI measure directly. But the chained CPI figure accounts for consumers who might actually substitute another meat which hasn’t experienced a price increase, say, pork.

The overall effect is for chained CPI to rise more slowly than the traditional CPI measure. This impacts tax brackets because the brackets will also rise more slowly, meaning when household income rises in the future, people will be shifted into higher tax brackets more quickly than they would have under the old measure when inflation elevated these brackets more in time with incomes.

Related stories:

FARMing: Planting new leads and cultivating prior clients

A weekly reminder to stay on top of your practice from first tuesday’s in-house broker!

For a historical example, see how chained CPI has moved more slowly than the traditional CPI measure in the past:

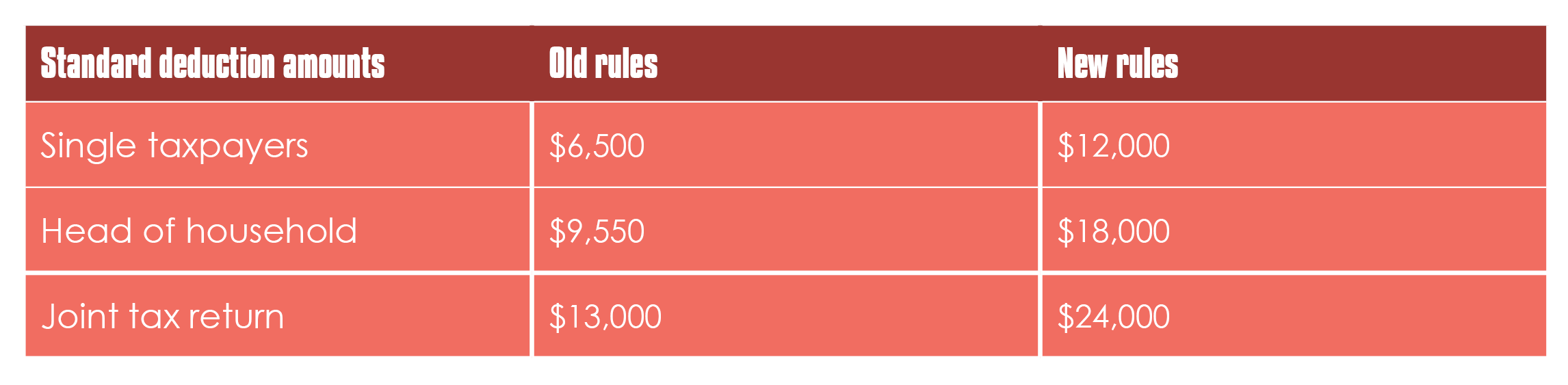

Standard Deductions

Standard Deductions

More taxpayers will be taking the standard deduction.

%

California homeowners who used to qualify for the MID

The standard deduction has almost doubled under the new tax plan. This has two results:

- Households that typically have taken the standard deduction will see a tax cut since the deduction is now much higher; and

- It will now make more financial sense for most people to take the standard deduction rather than itemize, resulting in higher taxes for about half the people who used to itemize under the old rules.

For real estate, this change is particularly important since the mortgage interest deduction (MID) can only be taken if a homeowner itemizes their taxes. Therefore, fewer homeowners will take the MID in future years.

Related stories:

FARMing: Planting new leads and cultivating prior clients

A weekly reminder to stay on top of your practice from first tuesday’s in-house broker!

Itemized Deductions

Itemized Deductions

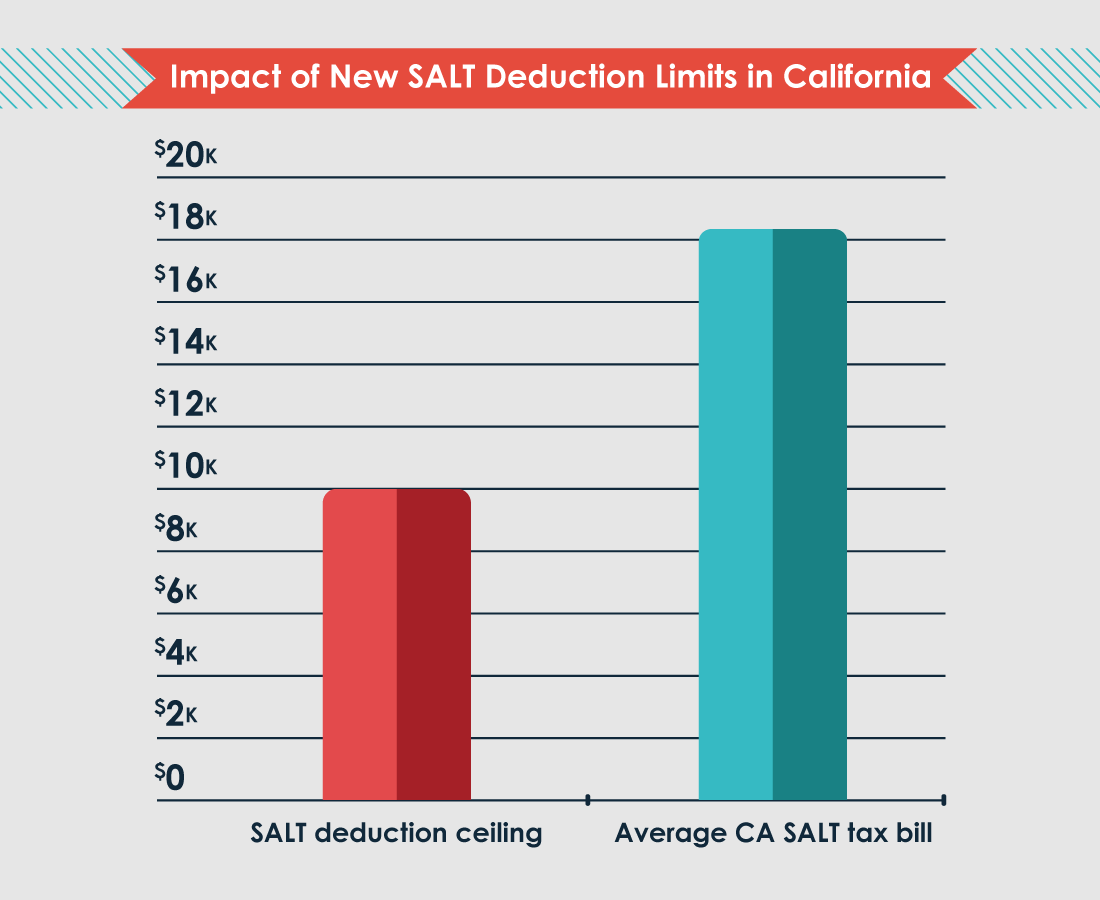

Itemizers will see more limitations, especially on SALT taxes.

Average SALT bill to exceed deductible limit

For those who itemize their deductions — and will continue to itemize under the new plan — there are some significant changes, including:

- State and local (SALT) taxes are now limited to $10,000 per tax return;

- the ceiling for the mortgage interest deduction (MID) is lowered from mortgages of up to $1 million to $750,000 — and interest on home equity loans (HELOCs) can only qualify for the MID if they fund home improvements; and

- the deduction for moving expenses is eliminated for all except for military families.

These changes will have a particular impact in states like California where SALT taxes and mortgage amounts are both higher than average. The state’s high cost of living translates to higher tax amounts for residents. But under the old tax rules, SALT taxes used to be fully deductible. Now, they will only be deductible up to $10,000. For reference, the average Californian pays $18,438 in SALT taxes.

Related stories:

FARMing: Planting new leads and cultivating prior clients

A weekly reminder to stay on top of your practice from first tuesday’s in-house broker!

The good news for California residents with high SALT bills is state legislators are working diligently on a workaround. One such workaround was introduced in Senate Bill 227 in January 2018, which would allow residents to make a charitable contribution to the state on SALT bill amounts exceeding the $10,000 deduction cap. This would allow residents to still deduct their full SALT bill through classifying their payments differently.*

*This section will be updated when the outcome on current pending legislation is final.

Estate Tax

Estate Tax

Fewer millionaires to pay the estate tax.

Total U.S. estates to be taxed in 2018 under new rules

The estate tax is a tax on gifts left to family members or other individuals upon a person’s death. These taxable items include:

Real estate |

Cash |

Personal property |

Business assets |

Insurance money |

However, the Internal Revenue Service (IRS) doesn’t normally tax an individual who receives items upon a person’s death. This is simply because most individuals don’t exceed the threshold or lifetime exclusion for being taxed, as it was quite high under the old rules and is even higher under the new rules.

Related stories:

The AI apocalypse for real estate agents

AI is smoothing the way for more sellers to take on FSBOs — should agents be worried?

Individual Mandate Repealed

Individual Mandate Repealed

Individuals will no longer face a penalty at tax-time for being uninsured.

%

Tax on investment income & profits remains

Taxpayers who don’t carry health insurance will no longer pay a penalty for being uninsured — this was called the individual mandate.

The impact of repealing the individual mandate will be twofold:

- an immediate tax break for those taxpayers who did not have health insurance and were forced to pay the tax penalty; and

- higher insurance rates for everyone who has health insurance.

The reason? The individual mandate was an effort to induce more healthy people to sign up for health insurance. This helped insurers keep their costs down. But now that healthy people don’t face a penalty for enrolling in basic health insurance plans, insurers fear they will be left with only sick people on insurance.

When more people are using their plans because of illness or other ailments, insurance will become more costly. However, the 3.8% tax on net investment income and profits added by the Affordable Care Act remains in place under the new rules.

The Affordable Care Act added a 3.8% tax on net investment income and profits (classified as unearned income) when modified adjustable gross income (AGI) exceeds a threshold of $250,000 for joint filers (or $200,000 for single filers). For real estate investors, this includes income and profit from:

- the operations and sale of rental property; and

- interest income on savings and trust deed notes, earnings on land held for profit and rents received on triple net leased property.

Related stories:

The AI apocalypse for real estate agents

AI is smoothing the way for more sellers to take on FSBOs — should agents be worried?

{kind=link}

0 Comments