Why this matters: First-time buyer data for an historical age group is still used by real estate agents to locate clientele for fee-generating services. The effects of the Millennium homebuyer and mortgage-foreclosure debacle directly affected the children of over one million California households. This debt experience is embedded in today’s first-timer age group. Further, this group carries a full load of student debt, suggesting a far older age group sets the parameters for locating today’s first-time buyers.

Aging into ownership

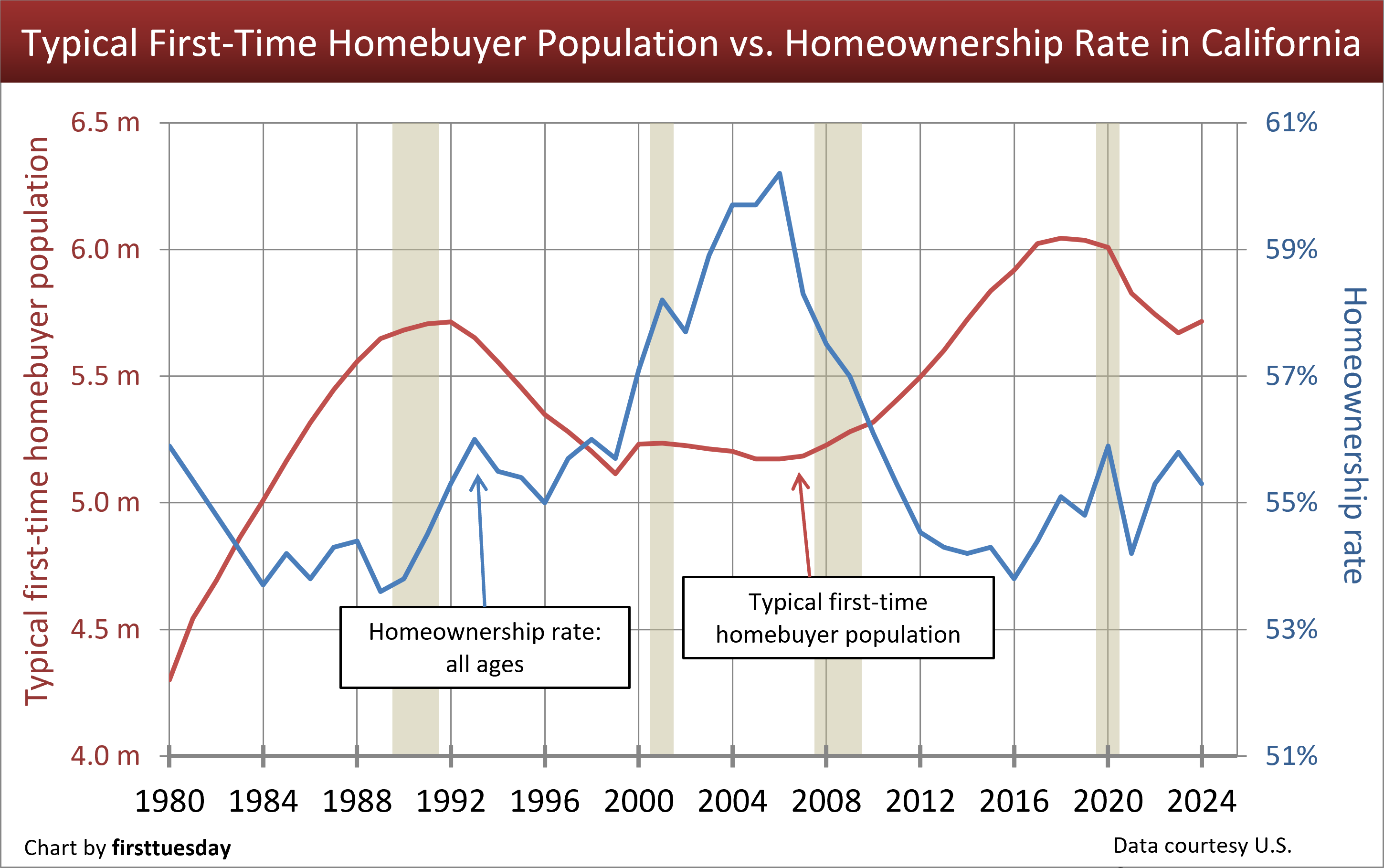

California’s historical first-time homebuyer population (aged 25-34) inched higher in 2024, just over 5.7 million. This population is up 9% from before the 2008 recession but has slipped since peaking in 2019, down 5% in 2024 from the peak.

Despite the past decade of growth in the first-time homebuyer population, the homeownership rate sank across all ages. In 2024, the state’s homeownership rate returned to 55.3%. Still, this is well below the past generation’s peak of 60.7% in 2006, which concluded with the Great Recession of 2008.

Rising levels of student debt, increased rents and low for-sale inventory have made it difficult for today’s young generation of first-time homebuyers to break into the market.

California’s homeownership rate will remain near its present level until the conclusion of the coming recessionary period. With California’s real estate recession underway since mid-2022, the next wave of current tenants will enter the market as potential homebuyers, likely around 2028, when the homeownership rate will grow gradually.

Updated July 28, 2025.

Chart update 7/28/25

| 2024 | 2023 | 2022 | |

| Potential first-time homebuyers | 5,716,100 | 5,670,629 | 5,744,450 |

| CA homeownership rate | 55.3% | 55.8% | 55.3% |

Over the past decade, first-time homebuyers have had a minimal (positive) impact on California’s homeownership rate. Homeownership dropped even as the number of 25- to 34-year-olds (the typical age of first-time homebuyers), rose. This age group, which currently consists of members of Millennials (Gen Y) and the younger Gen Z, has had little positive effect on homeownership.

Homeownership enemy #1: Unemployment and under-employment

The biggest obstacle for Millennials has been employment. Or rather, lack of employment.

Since the Great Recession ended, California finally regained all jobs lost to the crash. However, this momentum collapsed in 2020 as employment, the economy and daily life stalled at the onset of a global pandemic. Today, California employment number is around the number of Californians employed in 2019.

Members of Gen Z graduated into the Covid lockdown and faced other negative factors affecting the public —international trade chaos, volatile business conditions, rising cost of living and out-of-state attacks on California immigration.

Consequently, young would-be homebuyers have only begun to start saving for their first home purchase.

Homeownership enemy #2: Student debt

Heavy loads of student debt are a major creditworthiness problem for a first-time buyer. To become a first-time homebuyer, a purchase-assist mortgage is near mandatory. However, the amount of the mortgage is limited as the first timer’s payments on all household debt cannot exceed a standard 41% back-end debt-to-income ratio (DTI). This includes the mortgage, auto loans, credit card debt and education loans.

Most college grads need to clear their student debt before qualifying for a maximum home mortgage or settle for a home with less amenities and space than the apartment or home they rent. This process of paying back student loans typically takes twenty years, and then a thirty-year FRM remains well into their retirement.

In today’s economic climate, the 25-34 age group is simply too young and indebted to target as first-time homebuyers. Instead, 30-40 years or 35-45 are better ranges for the typical age of future first-time buyers when they have reduced their debt burden.

Millennials are going to look into the housing market following the current recession. Together with a reservoir of prior homeowners-turned-tenants, expect to see them gradually drive up the homeownership rate for the next real estate recovery.

City lights

As Baby Boomers begin to retire, those who own homes will, on the whole, remain homeowners. Their sale and repurchase or simply a reverse-mortgage retention of their home will not influence the homeownership rate.

As a consequence of the recent urban housing shift, much of the Millennial generation and Gen-Z will remain renters as before. Urban homes are more expensive due solely to their prime location and require accumulated wealth to obtain. The price spread is further influenced by zoning, which is costly as it restricts building density. As first-time homebuyers next look into buying, around 2028, the mark they make on the homeownership rate will reflect local government policy decisions.

The new normal?

California’s homeownership rate has always been low compared to the nation’s. We are a very mobile society composed of educated and skilled individuals who seek out better opportunities. As of 2024, we are the state with the second-lowest homeownership rate in the nation, at 55.3% (only above New York and Washington D.C.).

There is a reason California is the fourth largest economy on earth. It’s not early lockdown with homeownership, at least until homebuyers are financially well established.

It is clear that the high homeownership rate achieved during the Millennium Boom was an abrasive anomaly. Re-regulation of lenders and the consumer protection agency in 2010 was to ensure this won’t happen again – at least until we and Congress forget, and everyone goes through another flameout.

Expect the next wave of first-time homebuyers to arrive later and in smaller numbers than in the recent past, regardless of government handouts of incentives. Still, agents can prepare to cater to this population by focusing their efforts in urban areas. Or, for the more versatile and diligent agents, property management may be the answer as the number of renters will increase, maybe dramatically. That’s California.

{kind=link}

California is on a 8-12 year cycle since WW2. When the high school & college grads buy with EMOTIONS, they become the 1st time “consumers” not “investors”. If they buy at the bottoms of the market, they are REAL FRUGAL INVESTORS AND IF THEY SELL AT THE TOP, WHICH IS TOUGH AND EMOTIONALLY DRAINING, THEY will make a BRUTAL SCARY KILLING. Some will make as much as 1000 to 3000% on their down payments…. Yes, that much if they buy @ the low and sell @ the top. But most, sorry to say, learn from mistake, and not from GRAPHS & CHARTS…. This Real Estate Cycle, then burns the 1st home buyers (if they sell wrong or hold too long) and then the 2nd time they experience this LOW to HIGH, they will buy & then sell @ the top if their “significant other” agrees to sell too @ the top without EMOTIONS…. I have done this buy low and sell high since 1976 and if your EMOTIONAL, this is a TOUGH DECISION (almost as tough as divorcing) your wife or girlfriends to make HUGE IRR RETURNS. I have averaged 27.12% net net net per month from 1999 to 2008 on 198 sale escrows, and this is with RAW MATH ANALYSIS & ZERO EMOTIONAL INPUT!