Why this matters: Learn how to persuade a seller-client to order out third-party reports on a property’s condition to enhance marketability, provide a marketing package to prospective buyers and work up effective marketing plans to sell a property when employed under a seller representation agreement.

Seller’s costs to properly market their property for sale

A seller of a single family residence decides to employ an agent known to the seller to market and sell homes in the area.

The agent, after initial discussions with the seller, prepares an exclusive seller representation agreement and appropriate addendums for review with the seller.

Under the terms of employment, the seller agrees to:

- the services the broker performs to market the property;

- the fee the broker expects when earned; and

- obligations of the seller.

As an addendum to the representation agreement, the agent prepares a marketing package cost sheet. [See RPI Form 107]

The agent uses the cost sheet to advise the seller about:

- third-party investigative reports needed to market the property for sale;

- the estimated costs incurred to obtain the reports; and

- the authorization the agent needs to order out the reports.

The cost sheet addendum is the “seller’s budget” for costs they incur to support the agent’s marketing efforts with third-party documentation about the condition of the property for sale.

The marketing package cost sheet itemizes the property reports and sales activities which require cash outlays incurred exclusively for disclosing the condition of the seller’s property. The reports and activities are integral to the agent’s marketing plan to competitively attract buyers to consider acquiring the property.

Third-party reports for buyer evaluation

Third-party property reports put a face on the property enabling a prospective buyer to best evaluate its use and price. A buyer informed by reports about conditions affecting the value of a property and its location is more likely to acquire the property than a comparable property without documentation.

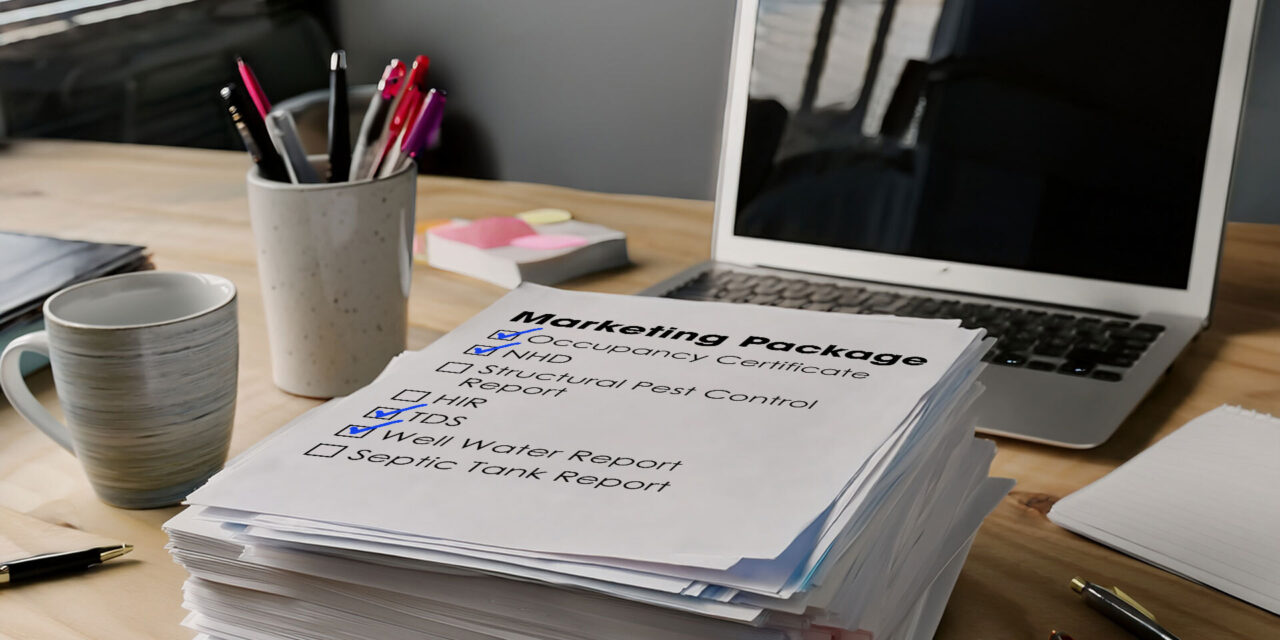

Third-party reports an agent initially considers for inclusion in a marketing package include a/an:

- occupancy (transfer) certificate to comply with local ordinance;

- natural hazard disclosure (NHD) statement;

- structural pest control report (and possible clearance);

- home inspection report and seller’s Transfer Disclosure Statement (TDS);

- well water report; and

- septic tank report. [See RPI Form 107]

On the seller’s approval and entry into an exclusive representation agreement, the agent has authority to order out specific property reports from third parties. With the authority, the agent prepares and delivers a request form to each third-party service provider to prepare and deliver their report. [See RPI Form 108]

The reports received by the agent are included in the marketing package the agent assembles and presents to prospective buyers. The agent advises the seller that upfront disclosures of property conditions avoid negotiations to resolve disputes arising over defects disclosed or discovered after the seller enters into a purchase agreement.

Related article:

Staging sets a buyer’s expectations

A buyer’s enforceable expectations about property conditions are set at the time a purchase agreement is entered into, due to:

- prior observations of the property by the buyers or their agent; and

- disclosures previously delivered to the buyer or their agent by the seller and the seller agent.

Property conditions belatedly revealed to the buyer after the buyer and seller agree to a price in a purchase agreement may differ from the buyer’s reasonable expectations about the property’s conditions and uses. Disclosures or discoveries of adverse property conditions after the buyer and seller enter into a purchase agreement were not known to the buyer when setting the price agreed to for the property. [Jue v. Smiser (1994) 23 CA4th 312]

Thus, the seller makes a choice, on the advice of their agent, about when to incur the expense of third-party reports:

- now, on employing the agent to sell the property so any purchase agreement entered into is the result of the prior delivery to the buyer of a complete set of property disclosures; or

- later, after entering into a purchase agreement when the buyer’s expectations about the property conditions may differ from later disclosures or discoveries. [Jue, supra]

When disclosures are delivered after a seller enters into a purchase agreement to sell the property, the buyer may demand that the seller eliminate the defects at the seller’s expense or adjust the price prior to closing. Alternatives to the buyer’s demand prior to closing include the buyer’s right to:

- cancel the purchase agreement; or

- close escrow and demand a refund of the overpayment in price or the cost of repairs.

A competitive sales advantage with upfront disclosures

For sellers, a seller agent ready with a complete marketing package for delivery to a buyer on a request for more information creates a competitive sales advantage over properties not marketed with property condition reports.

Further, buyer agents are attracted to properties offered with investigative third-party reports and seller disclosures delivered in a marketing package, sometimes called a backup package. With a marketing package, property disclosures provided to prospective buyers containing third-party reports reduce the:

- seller’s exposure to liability under their duty to fully disclose their knowledge of the property’s condition to a buyer [Calif. Civil Code §1102.4]; and

- seller agent’s exposure to liability under their duty to personally inspect, observe and report their findings to buyers about a property’s condition. [CC §2079]

Importantly, when property condition reports are delivered prior to the seller entering into a purchase agreement, the close of escrow is not contingent on the buyer’s further-approval of property conditions, further negotiations or cancellation.

The primary risk-mitigating advantage for the seller who invests in third-party reports for the agent’s marketing efforts is transparency at inception of negotiations with a buyer. The price agreed to in the purchase agreement is based on property conditions “as disclosed” by the reports, not altered by in-escrow disclosures.

The seller and seller agent avoid considering provisions for an undisclosed (and prohibited) “as is” sale. “As is” sales situations inevitably lead to price renegotiations, repairs, cancellation of the purchase agreement or litigation. The cause nearly always is the failure to disclose material defects known to the seller when the seller accepts the buyer’s purchase agreement offer. “As is” does not mean “as disclosed.” [CC §§1102.1, 2079]

Related video:

The seller’s motivation to sell

A seller’s reaction to their agent’s request for the seller to invest in an advantageous marketing plan offers the agent insight into the seller’s motivation for selling the property. The agent’s goal — besides employment to sell a property and earn a fee — is to encourage and receive maximum cooperation from the seller in their sales effort.

A seller may “dress up” the property to enhance its “curb appeal” by cosmetic painting, landscaping and clean up. However, it is the buyer’s knowledge of the property’s fundamentals which generates firm and uncontested offers to purchase.

Thus, the seller is asked not only to enter into a seller representation agreement with an agent to achieve the sale of the property. They are also asked to fund acquisitions of the tools unique to the property and for no other use than for the agent to use to openly disclose the property’s fundamentals to prospective buyers at the earliest opportunity — ASAP, on a request for more property information.

However, the seller’s motivation to sell might be due to a lack of sufficient cash to retain ownership such as payment of property taxes, insurance, mortgage payments and deferred maintenance. A cash-availability issue interferes with paying for reports needed to properly market the property.

A financially distressed seller unable to pay for third-party reports significantly increases the seller agent’s risks in the employment. The agent is faced with issues arising in a sale due to a buyer’s disapproval of contingencies brought on by in-escrow disclosures and discoveries.

Here, the seller agent is caught up in the sale of the property twice:

- once to find out what the property conditions are which caused the first buyer to back out; and

- again, when the agent discloses to a new buyer conditions discovered in the failed transaction.

Timely disclosure

A seller (and lazy agent) may not want to disclose the condition of the property until after the seller accepts a purchase agreement offer from a buyer. The seller may seek this sequence of events with the intent to:

- make only those concessions necessary to keep the transaction together once in escrow after the buyer is emotionally committed to the purchase; or

- remarket the property to another buyer who has been fully informed about the property’s condition.

But such conduct by a seller is deceitful. Worse, the seller agent is always viewed as part of any problem in a transaction.

A seller, as well as the seller’s agent, who knows property conditions which negatively affect the value of the property, then withholds the information until after they accept a buyer’s purchase offer, commits a type of intentional fraud.

To avoid seller misconduct and gauge the seller’s motivation, the best time for the agent to present the seller with the marketing package cost sheet is when the seller representation agreement is reviewed. A seller motivated to sell — not merely “testing their asking price” in the marketplace — responds positively to the agent’s advice, even when they do not agree to fund the reports.

A seller’s negative response to making property disclosures when marketing the property indicates the level of future cooperation the agent can expect. The deceptive nature of a seller manifests at all stages of representation to interfere with the marketing, contracting to sell and closing an escrow. This seller is not part of the team.

The seller agent who acquiesces to delayed disclosures loses control over marketing and takes on unacceptable risks from the moment they are employed to represent a seller with questionable behavior.

Related Client Q&A:

Broker fee considerations

Implicitly, the dollar amount of the fee a broker seeks for marketing a property, locating a buyer and closing a sale is related to the:

- sales price the seller will accept for their property compared to the sales price of comparable properties;

- time, effort and money spent marketing a like-type property and advising the seller; and

- probability of locating a buyer willing to acquire the property under current market conditions.

When a property appears likely to sell within the representation, an agent is in position to decide whether to enter into a representation agreement with a seller. Does a reasonable likelihood exist for producing a sufficient fee?

Consider a broker who requires agents to attach a marketing package cost sheet to all seller representation agreements entered into with sellers. By including the addendum, the seller does (or does not) authorize their agent to order out reports needed to market the property and screen prospective buyers.

The broker requires inclusion of a cost sheet addendum to increase the productivity of their agents. Property reports might add administrative tasks for a broker, but they reduce the time spent locating a buyer, negotiating a purchase agreement and closing a sale of the property.

As part of the agent’s negotiations to set the fee, the broker instructs the agent to ask for and encourage the seller to authorize the ordering of reports necessary for marketing and risk reduction.

Offsetting broker fees

As an economic inducement for full disclosure when employed by a seller, the broker and their agent may offer to offset the fee earned on a sale by the amount of the seller’s cost of the reports. Also avoided is the unsavory habit of a broker using their own funds to pay the cost of reports, or any corrective work or staging undertaken on the seller’s property to make it marketable.

Brokers render services. They are not in the business of advancing costs to finance seller-clients in an effort to “buy” an employment to sell a property. [See RPI Form 107 §3.3]

Alternatively, the broker may offer a reduction in the broker fee by, say, one-quarter of one percent to induce the seller to pay for reports ordered for marketing at inception of the employment. The reduced fee reflects the greater likelihood of a successful closing of a sale, devoid of complications before or after closing.

Thus, agreeing to a lesser fee amount may be considered an offset of:

- the reduced time and effort necessary to market the property for sale;

- the reduced risk of loss of the time, talent and money expended by the broker and their agent; and

- a more effective marketing plan, which, on average, produces more transactions annually for the broker.

Further, a transparent sales transaction rewards a broker and their agent with goodwill in current and future transactions.

Related article:

Requesting authority from the seller

A seller who refuses to pay for property reports is advised that a prudent, knowledgeable buyer or buyer agent orders out reports when the seller does not produce them. In turn, the buyer inevitably uses the reports against the seller as a “punch list” to demand completion of repairs and replacements before the buyer closes escrow.

It is worth noting that none of the items listed on the advance cost sheet are, in any way, part of the broker’s overhead for maintaining a brokerage office. All the costs listed, when incurred, are related solely to establishing the condition of the seller’s property, which then is marketed and sold by the agent.

The costs of reports on property conditions are not incurred by the seller as compensation for the agent’s services. They are incurred to assure buyers the seller’s property is what it is. Thus, the costs are properly the obligation of the seller and are not to be advanced by the seller broker or their agent.

Further, the reports on property conditions sought to assist in the marketing are generally the same reports the seller needs to provide when a buyer is located. However, the agent needs the reports when they post the availability of the property for sale. [Jue, supra]

Related video:

Read more about the marketing package cost sheet.

The influence of business cycles on timing

Business cycles in real estate sales also influence a broker’s need for authorization to obtain property reports for a marketing package. During periods of rising prices, disclosures tend to occur less frequently and are deliberately delayed by “lazy” seller agents despite best brokerage practices and rules to the contrary.

In boom or bubble times, sellers become impatient, driven by pricing to sell, while buyers are fear of missing out (FOMO) anxious to buy and permissive of failed disclosures — but that is not justification for a broker’s failure to timely disclose. Both sellers and buyers drop their guard in a deliberate effort to meet their short-term objectives. Brokers are often caught off guard in the frenzy.

Conversely, during periods of decreased sales volume, buyers are more selective and buyer brokers more protective of their clients. In a weak market, sellers need to step forward to fund the cost of reports simply to “sell” the property. The seller broker with comprehensive property disclosure reports has an equal or better marketing package than other properties to facilitate their connection with a buyer.

Related article:

Using the yield spread to forecast recession and recovery conditions

When to pay

A seller may choose when and how to pay for the cost of the reports when filling out the advance cost sheet. The seller may opt to pay the charges directly to the third-party provider once billed. Here, the broker coordinates the arrangements for payment with the provider. The seller’s check is thus payable to and delivered directly to the provider, not to the broker.

When a check is handed to the seller broker for delivery to the provider, the check constitutes trust funds. As trust funds, the broker or their agent makes an entry in the trust fund ledger maintained by the broker. [See RPI Form 107 §4.1]

Alternatively, the seller may deposit the estimated cost of the reports with the broker by making the check payable directly to the broker, called advance costs. The broker then pays the charges for reports from the deposit when billed by the provider. [See RPI Form 107 §3.4]

Related article:

Advance costs as trust funds

Funds advanced by a client payable directly to a broker belong to the client. As money held for a client, the broker places all advance cost deposits the broker or their agent receives in a trust account in the broker’s name as trustee. [Calif. Business and Professions Code §10146]

The advance cost sheet authorizes the broker to disburse the client’s funds from the trust account only as costs are incurred. When the representation period terminates, the broker returns all remaining trust funds to the client. The broker is prohibited from using trust funds to offset any fees the client may owe them.

The broker is also required to give the client a statement of accounting at least every calendar quarter for all funds held in the trust account. However, increasing the frequency by mailing a copy of the client’s trust account ledger each month creates a better business relationship.

A final accounting is delivered when the representation agreement expires. Again, when any funds remain in trust, the broker return them to the client with an accounting. [Bus & P C §10146]

Related video:

Statement of account

The statement of account for the trust funds includes the following information:

- the amount of the deposit toward advance costs;

- the amount of each disbursement of funds from the trust account;

- an itemized description of the cost obligation paid on each disbursement;

- the current remaining balance of the advance cost deposit; and

- an attached copy of any advertisements paid for from the advance cost deposit.

Lastly, the broker keeps all accounting records for at least three years and makes them available to the Department of Real Estate (DRE) on request. [Bus & P C §10148]

A broker who fails to promptly place advance deposits payable to the broker in their trust account, or who later fails to deliver proper trust account statements to the client, is presumed to be guilty of embezzlement. [Burch v. Argus Properties, Inc. (1979) 92 CA3d 128; Bus & P C §10146]

Related article:

{kind=link}