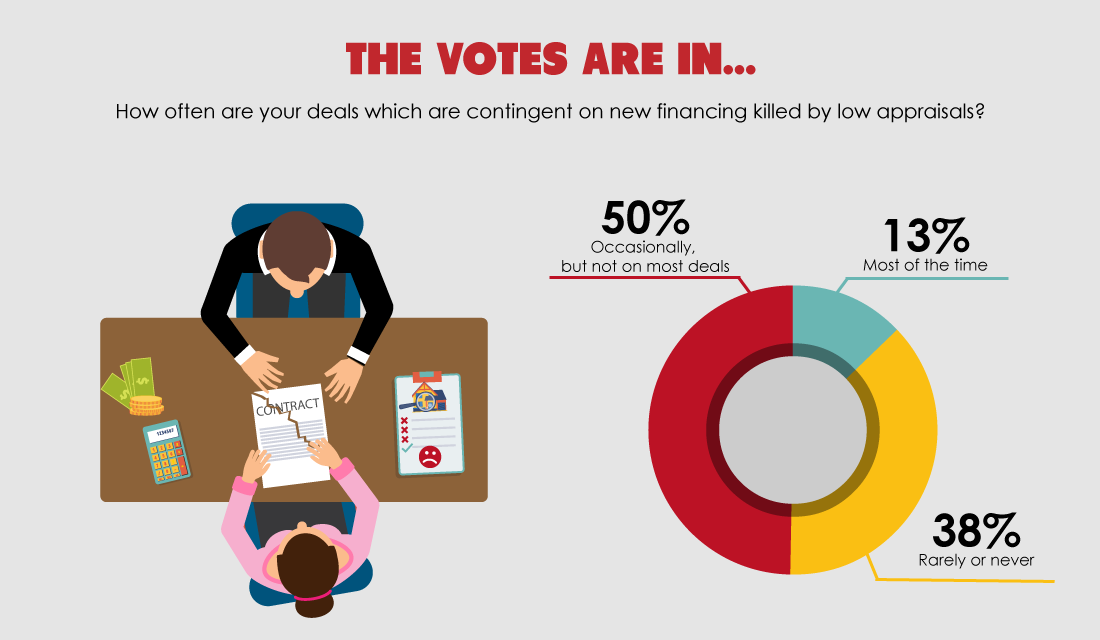

Do low appraisals still interfere with your closings? In response to a recent poll, 50% of our readers said low appraisals occasionally kill their deals contingent on new financing, while 13% said low appraisals interfere most of the time. Only 38% said low appraisals never or rarely prevent a closing.

These results are similar to poll results from a year prior when 56% of readers voted low appraisals occasionally kill their deals, 10% said low appraisals interfere most of the time and 35% said rarely or never.

Our poll results indicate the majority of real estate agents still experience issues closing sales due to low appraisals that interfere with their buyer’s financing.

AMCs and the bad appraisal

The appraisal is integral to the price agreed to between the seller and buyer, which means it has the potential to make or break a deal.

At the center of the low appraisal dilemma is the appraiser who determines a property’s value. Property appraisers were once considered specialists in a local market with expert knowledge of comparable properties and trends. However, today’s lending industry uses the anonymous appraisal management companies (AMCs) by federal directive in an attempt to improve appraisal quality and ensure appraisers have no affiliation with the lender.

Yet, often the appraiser employed from an AMC for a property lacks the specialized knowledge of the area to provide a more accurate appraisal, compromising the quality of the appraisal. When lenders require more appraisals be handled by an AMC, the risk of a failed closing increases due to a knee-jerk appraisal coming in lower than the contracted price.

Further, though California has mandated additional requirements for AMCs to ensure proper appraisal methods, the issue of low appraisals by unreliable appraisers remains.

Rebutting a low appraisal

As deals continue to die after bad appraisals, some real estate agents are getting aggressive with their recourse. Proactive agents send a rebuttal letter to the lender arguing for a second appraisal from a more qualified local appraiser — i.e., one familiar with the nuances of the local market.

A successful rebuttal letter:

- is written by the buyer with the help of an experienced agent;

- focuses on hard facts rather than emotions;

- includes professional opinions and recent comps to rebut the previous appraisal; and

- is professionally bound and sent to all participants in the transaction.

Drafting a rebuttal letter is a sound practice when an experienced agent deems it necessary. However, talk of rebutting low appraisals during a momentum market is worrisome.

Any competent agent will know the fair market value (FMV) of a listing in their community. When the appraisal comes in low after an offer has been accepted, the experienced agent will know to ask first whether the price is fair.

As markets heat up, buyers often use their emotions when making an offer. Here, a savvy buyer’s agent will know when to apply the brakes and avoid allowing their buyer to make a high offer on an overpriced property.

Alternatively, in the case of a low appraisal, a buyer’s agent may advise their buyer to pay cash for the difference in appraised value and the price set in the purchase agreement. This is a favorable option for a buyer in a rising market when property values are expected to increase and, thus, welcomed advice from the agent.

{kind=link}