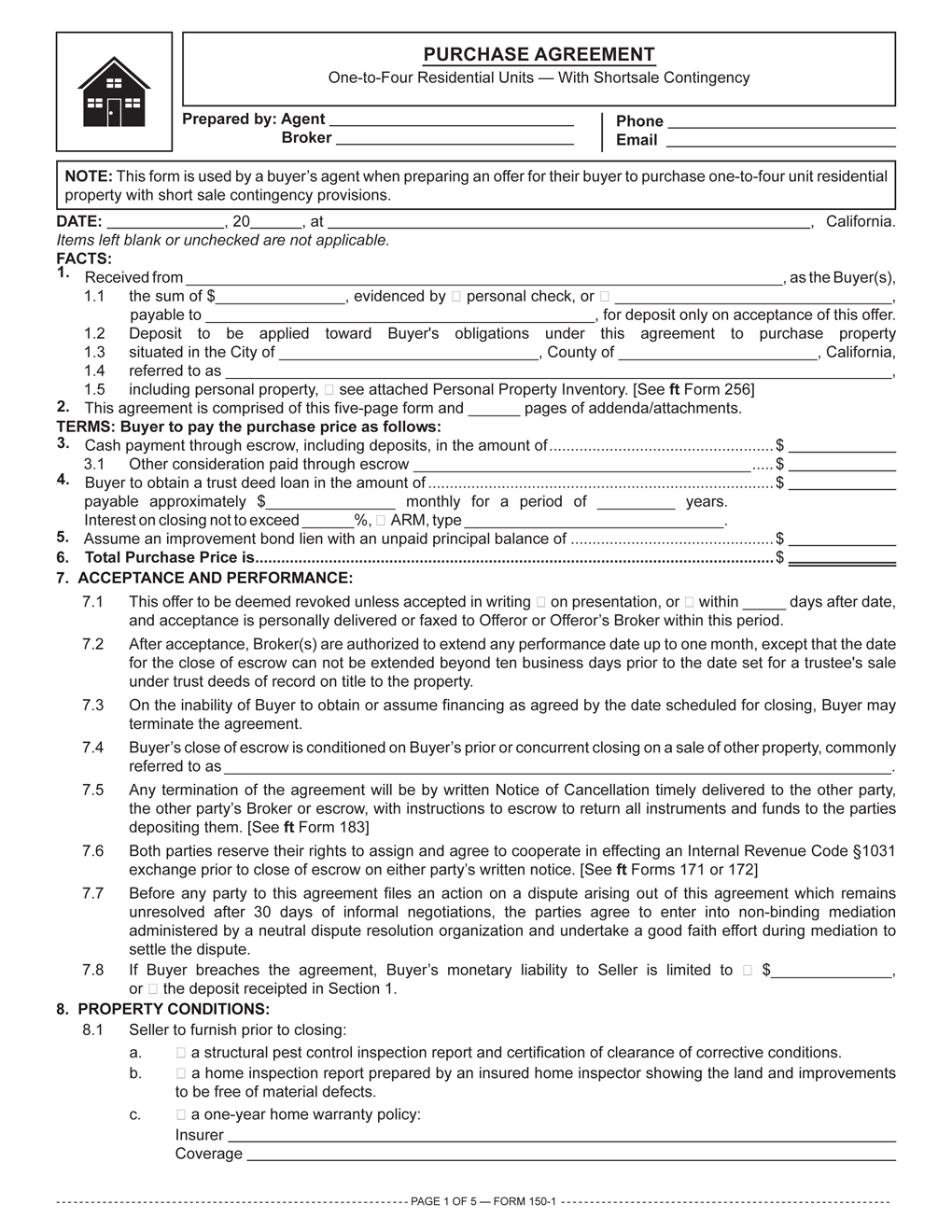

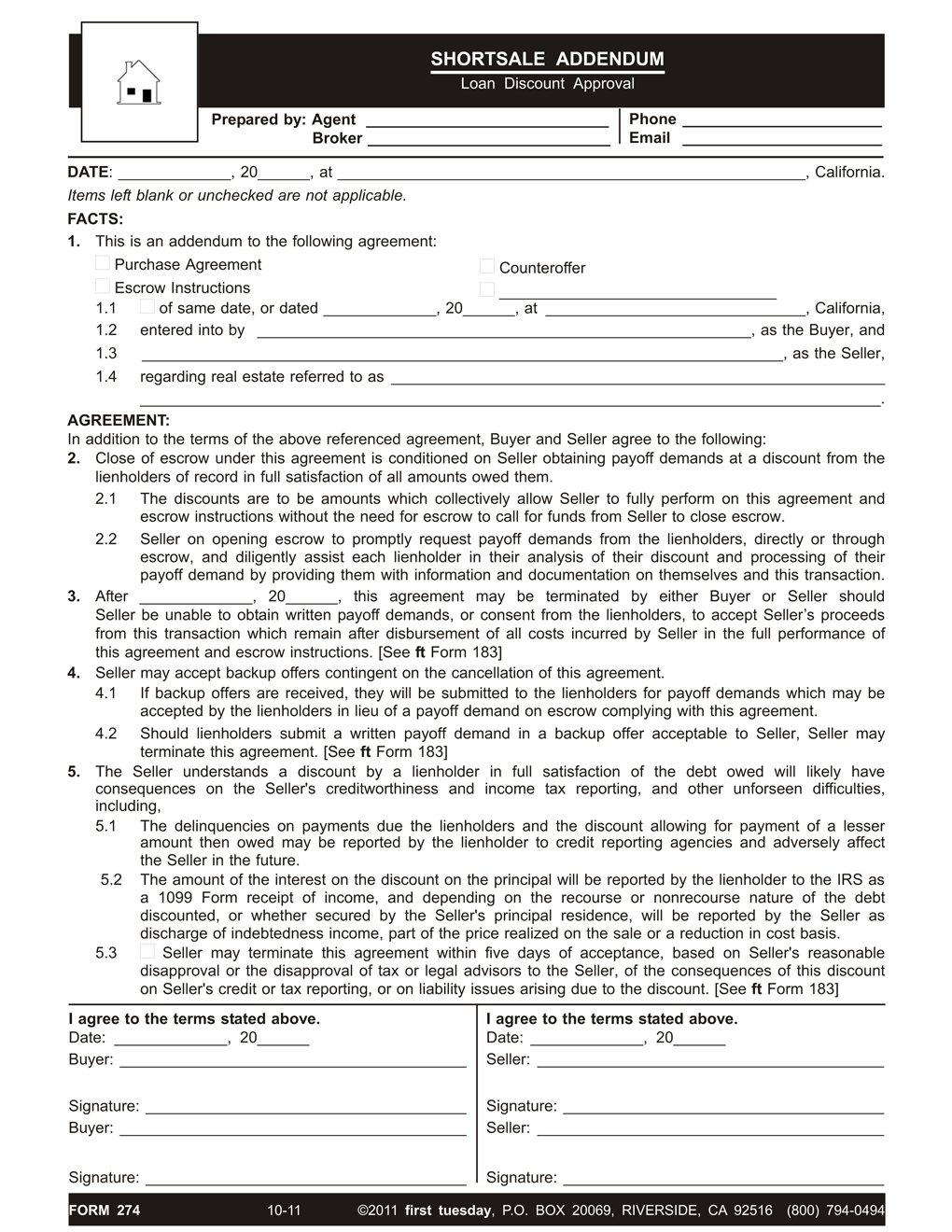

Form-of-the-week: Purchase Agreement with Short Sale Contingency – Form 150-1 and 274

Selecting the right purchase agreement

For a real estate transaction conveying fee ownership of a property, the primary document a buyer’s agent uses to negotiate their buyer’s acquisition of property is a purchase agreement. [See RPI Form 150-159]

The use of different varieties of purchase agreements is required for different types of properties, buyers and financing arrangements. The various purchase agreements contain provisions necessary for the buyer’s agent to readily negotiate the purchase of a particular property with a particular seller.

Three basic categories of purchase agreements exist to formalize real estate transactions. The categories are influenced primarily by legislation and court decisions addressing the handling by the seller’s agent of the disclosures and due diligence investigations required of them to properly market properties.

The three categories of purchase agreements are for the acquisition of:

- one-to-four unit residential property [See RPI Form 150 – 153 and 155 – 157];

- property other than one-to-four residential units, such as for income-producing properties and owner-occupied business/farming properties [See RPI Form 154, 158-1 and 159]; and

- land and unimproved parcels. [See RPI Form 158]

Within each category of purchase agreements, several variations exist. The variations cater to:

- the use of a property;

- the diverse arrangements for payment of the price;

- property conditions which affect value; and

- loan discount approvals on a short sale within the one-to-four unit residential property.

{kind=link}

With the recent protection offered by CCP 580e, short sales short sales are a good option for many underwater borrowers, especially given this year’s Supreme Court decision that eliminates the “stripping” of 2d’s. However, borrowers need to remember that although their liability to the lender[s] is eliminated, they remain fully liable to the buyers for any disclosure violations; so over-disclose. Real estate agents handling short sales will do their sellers and themselves a big favor by making sure that short sellers receive legal counseling on the liability and tax issues.

I’m in a deal now and it surprises me how no one reads the documents. So much is over looked. They all operate as if th contract does not apply. I’m constantly pointing out facts and they always reply, this is how we always do it. Serious issues overlooked.