Adjustable rate mortgages (ARMs) made up roughly 11% of all mortgages recorded in California in January 2015. Today’s use of risky ARM purchase-assist funding has declined slightly in recent months, the result of decreasing fixed rate mortgage (FRM) rates during Q4 2014. ARM use remains below the average ARM-to-loan ratio seen over the last 30 years and well below the 77% extreme experienced during the Millennium Boom.

ARM use normally tracks with FRM rate movement, which affects buyer purchasing power. Buyers turn to ARMs to extend their buying reach when FRM rates rise. In turn, when FRM rates decrease, buyer need for ARMs is reduced.

Expect FRM rates to remain low during 2015, not to increase until the Fed takes action to raise the short-term rate. This is expected in the early part of 2016, perhaps sooner. At that time, ARM use will rise once again, and buyers will unwittingly take on risks homeowners other than the very wealthy cannot absorb. Here, protection of the consumer is left to the buyer’s agent as their duty owed to the buyer client.

Chart 1

Chart 2

Chart update 03/05/15

| Jan 2015 | Dec 2014 | Jan 2014 | |

| ARM-to-loan ratio | 11.3% | 12.3% | 13.5% |

*Note: From August 2010 on, all ARM-to-loan ratios are first tuesday estimates based on the ratio of ARMs to all mortgage loans originated in the Southern California region, as reported by DataQuick. All prior numbers are based on recorded statewide ARM use.

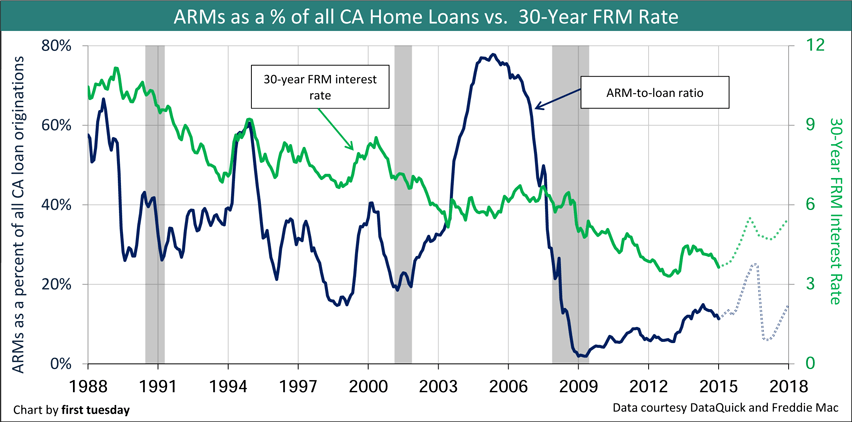

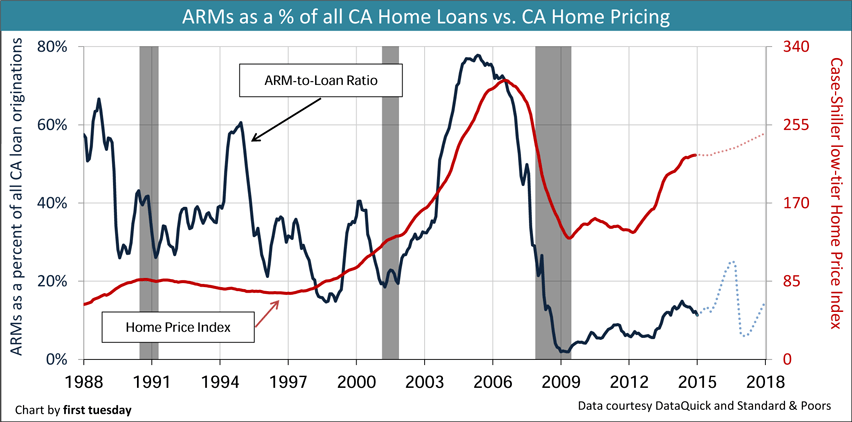

The charts above present two market perspectives on adjustable rate mortgage (ARM) used to purchase homes in California. Both charts track ARM loans as a percentage of all mortgages recorded in California, called the ARM-to-loan ratio.

The first chart juxtaposes California’s ARM-to-loan ratio with the 30-year fixed rate mortgage (FRM) rate for the Western Census Region. The second chart couples the ARM-to-loan ratio with the monthly average of low-tier home pricing in San Diego, Los Angeles and San Francisco.

The ARM-to-loan ratio itself is a measure of the relationship between ARMs and FRMs. It can be used to determine probable future sales volume and price movements for 12 and 24 months, respectively.

ARMs volume depends on FRM rate movement

The single most powerful engine driving home price movement is the availability of purchase-assist mortgage money. Evidence of this is the boom in sales volume and pricing brought on by unwarranted mortgage funding in the mid-2000s.

Related article:

Brokers who observe the relationship between the FRM rate and the ARM-to-loan ratio will notice they are able to predict California’s future home sales volume and price movement. Sales volume and pricing are heavily influenced by financing trends set in motion by the bond market and federal monetary policies.

The FRM and ARM-to-loan connection

30-year FRMs are the basic and essential form of financing for homebuyers. If FRMs are available at reasonable interest rates, the well informed homebuyer will choose the FRM over the much riskier ARM loan.

In a mortgage market functioning normally, the ARM-to-loan ratio moves parallel to FRM interest rates. Any deviation from parallel movement is a clear warning of an impending distortion in real estate sales volume and pricing.

As shown in Chart 1, ARM use increases as FRM interest rates increase which in turn drives real estate prices down.

When FRM rates first increase, sellers are unwilling to lower prices in response to increased FRM rates. This is the sticky price phenomenon, ever present when mortgage rates rise faster than personal income. For their part, homebuyers don’t readily lower their standard of living aspirations. They either pay too much at the sticky prices, or wait out the market.

Thus, sticky prices compel impatient homebuyer-occupants to borrow larger sums than available with an FRM by resorting to ARMs. Lured by their temporary lower rates, these buyers pay too high a price at the time.

For instance, ARM use jumped dramatically when FRM rates were raised in 1988, 1994 and 1999. Supported by homebuyers’ use of ARMs, high prices persisted for a while after they were programmed to drop. ARMs deliver more money than homebuyers otherwise qualify to borrow on an FRM. In these cases, the homebuyer and their access to funding from ARMS contrived artificially to keep prices up.

ARMs span the gap

Generally, lenders do not qualify homebuyers for mortgage amounts with monthly payments exceeding 31% of their monthly income. Thus, any increase in FRM rates immediately reduces buyer purchasing power, offsetting mortgage principal amounts. With their lower interest rates, ARMs bridge the gap in available purchase money created by FRM interest rate increases.

Related article:

When FRM rates rise, buyers’ ARM use keeps prices from falling and quickly adjusting to market conditions. On the other hand, when FRM rates are flat to down, excessive ARM originations directly cause property prices to climb significantly. This condition last occurred in the mid- 2000s.

The increased availability and use of ARM purchase funds stabilizes sales volume for a period, keeping it from immediately dropping in times of increasing FRM rates or prices. This arrangement financially favors sellers.

Homebuyers, on the other hand, pay too much for their property and imperil their continued homeownership. Meanwhile, mortgage lenders take in greater earnings in a shift of wealth from sellers to lenders when mortgage rates rise.

Likewise, when FRM rates are dropping, a rising proportion of ARMs is a distortion which leads directly to a bubble in home sales volume and pricing. Once the ARM-to-loan ratio has run contrary to FRM rate movement for several months, prices fall back toward mean price levels.

This distortion is seen in Chart 1 in 1993, and again in 2002. In the current recovery period, the ARM-to-loan ratio has remained parallel with FRM rates — both climbing upward.

The ARM borrower at risk of loss

A rising ARM-to-loan ratio is a clear sign of instability in the real estate sales and mortgage markets. Instability forebodes weaker sales volume, which eventually lowers home prices. Ultimately, if the trend of a rising ARM-to-loan ratio persists for more than six months, foreclosures will increase within a couple of years.

Today, monthly payments on an FRM used to acquire a low-tier single-family residence (SFR) exceed the rent these SFRs command.

Thus, the tire-kicking aspect of home sales: in an effort to induce tenants to buy and become homeowners, sales agents need to show a financial advantage in terms of monthly outlay. But increased prices and mortgage rates have joined to drive the monthly cost of ownership considerably beyond rents in the low-tier resale market.

The tenant is induced to buy, won over by the ARM’s initial monthly payments if they are equal to or lower than the the rental rate for the SFR. Sales volume is maintained and ownership seems the financially wise thing to do. Correct?

Yes — until you consider the risk of losing your home as the ARM rate resets and your mortgage payments increase faster than your personal income. Over the next 30 years interest rates will have the opposite influence on pricing as the declining rates of the past three decades.

Forecasting the future

To forecast home sales volume and pricing, examine the correlation between FRM rates and the ARM-to-loan ratio on Chart 1.

Ordinarily, the ARM-to-loan ratio rises, falls or holds steady in tandem with the movement in FRM rates. It is this parallel relationship that softens changes in sales volume and prices going forward.

However, stable sales and pricing conditions end when external factors cause the ARM-to-loan ratio to break away from the FRM rate trend.

External factors driving this destabilization include:

- increases in jumbo loan demand in the high-tier housing category;

- rapid shifts due to changes in demographic demands within an area to buy or sell;

- too much or too little construction activity to meet the growth or relocation of the population; and

- changes in government regulation of mortgage financing or taxation of homeownership.

To forecast home sales volume 12 months forward, and price movement 24 months forward, observe and follow any divergence from FRM rates in the ARM-to-loan ratio movement. The longer the distortion runs the greater the future adverse disruption in sales volume and pricing 12 and 24 months out, respectively.

Home sales volume tends to rise and fall in a cyclical fashion. These cycles correspond to economic recessions (represented by gray vertical bars on the charts) and booms. Expect these cycles to be shorter and more frequent in the coming decades than during the period from 1980 to 2012. An example: the brief pricing boom experienced in 2013-2014, induced by speculator over-activity.

Editor’s note: There is no such thing as a 5-year, 7-year or 10-year cycle – it is a business cycle controlled by interest rates via the Federal Reserve.

Home prices fluctuate primarily due to trend changes in sales volume 9-12 months prior. Again, sales volume changes in response to interest rate movement 12 months prior to that.

Related articles:

For instance, the pricing momentum generated by rising sales volume tends to peak some 8 to 12 months after home sales volume reaches its apex. This delay is due in part to ARM use enabling seller’s sticky pricing.

However, a speculator invasion of the SFR resale market elbows out buyer-occupants and, in time, artificially drives up prices. That occurred the entire year of 2013, with stragglers wandering into the market in 2014 to buy and flip in (false) expectation of a quick profit.

Looking forward, neither a continued boom in pricing nor a recession will take place in 2015. As long as mortgage rates remain low, pricing will continue to bump along at a modest pace of increase. However, when rates rise–likely in early 2016–pricing will feel downward pressure.

Historical examples

Let’s look at some historical instances of the relationship between FRM rates and the ARM-to-loan ratio:

1. In 1996-2002 the ARM-to-loan ratio moved parallel with FRM rates. This displayed ideal lending conditions for a stable housing market. Real estate prices rose at a sustainable rate for the duration of this period.

2. Beginning in 2002, FRM rates dropped continuously for two years. In the meantime, the ARM-to-loan ratio began to rise. This inverse movement was brought on by reduction in government oversight of mortgage lenders, called deregulation.

Without consumer protection, providers of mortgage money at large Wall Street banks were at liberty to push (and tease) for increased ARM use to continue bundling mortgages and selling mortgage-backed bonds.

The unanchored rise in the ARM-to-loan ratio that followed led directly to hugely excessive home price increases, which continued for nearly three years. The ARM-to-loan ratio peaked in early 2005, and sales volume turned down in mid-2005. Home pricing reached its apex one year later in early 2006; sales volume tanked in 2007.

3. Between 2005 and 2009, FRM rates remained flat while the ARM-to-loan ratio reversed course and dropped significantly. The declining ratio in ARMs to all loans alongside a flat FRM rate, an abnormal sequence, presaged a further decline in home prices.

In short, decreased ARM use (without an accompanying drop in FRM rates) was both a symptom and a cause of the catastrophic Great Recession. Rates on FRMs dropped in early 2009 and the ARM-to-loan ratio responded by dropping to almost zero. The demand for mortgage dollars was insufficient to keep ARM use high.

The current market

ARMs made up 11% of mortgage originations in California during January 2015. This is extremely low compared to a 77% ARM-to-loan ratio at the height of the Millennium Boom. Still, the current ARM-to-loan ratio is trending much higher than the bottom of 2% in May 2009.

Editor’s note — For comparison, the peak national ARM-to-loan ratio was only 36% during the boom.

The ARM-to-loan and FRM relationship has remained relatively stable since 2010.

Interference by speculator acquisition and resale activity – the flip situations – brings about two-year bumps and distortions in pricing, which in turn reduces sales volume during that episode.

However, in the new lending regime emerging from the present zero lower-bound interest rate environment, stability in and beyond this recovery is not absolute. ARMs have only been observed at work over the past 30 years during which we experienced a consistent decline in interest rates. All that thinking now needs to be reconsidered.

The next two or three decades will be marked by constantly rising interest rates. As interest rates steadily increase, ARM use will likewise rise as homebuyers – in need of more money as slipping personal income limits borrowing capacity — are attracted to initially lower rates. Nevertheless, it is unlikely ARM use will rise again to the heights seen during the Millennium Boom.

{kind=link}

This article suffers from a fundamental misunderstanding that renders its primary conclusion false. The article concludes that homeowners tend to to take ARMs in a rising market in order to qualify for the higher loans amounts. However, the current underwriting environment is qualifying most ARM borrowers at rates HIGHER than fixed rates. So ARM borrowers actually qualify for less home than with fixed rates.

The problem is that the article uses data from the pre-crisis period, when ARM borrowers indeed qualified at much lower rates. [Hey, with SISA, NINA, etc. loans, they did not even need qualification!] So the ARM-fixed ratios are now meaningless due to the major change in how ARM loans are underwritten.

While Mr. Carrico offers some valuable comments, he fails to catch the point being made by the article. That point being: We have been, for a long time now, in a declining interest rate environment, but according to the author of the article, that is about to change.

The lenders in collusion with the FED are once again setting us up. Millions of buyers will be enticed with low ARM rates, only to see their home prices drop precipitously in the next few years, thus wiping out any equity they may have built up and negating any benefit from using an ARM.

This is the age old game the “controllers” (the banking powers in collusion with government) use to transfer wealth (in this case in the form of property) FROM the common people TO themselves.

You saw that happen from 2006 to now. You will see it happen again, unless the entire control system is derailed and an equitable system replaces it.

As prices are hugely bloated at the current time in many markets, the buyer (now more family end-users) will be enticed to buy and forced, due to insufficient income, to use an ARM to make the purchase. When enough millions are thus drawn into the trap, the gate will be slammed shut by the “controllers” (interest rate increase), the ARM monthly payments will shoot up, and the slaughter will begin anew, with millions more foreclosures, just as we saw in recent years.

Who are the sellers listing so many properties today at such bloated prices? In many cases it is the speculators who bought in low from 2009-11, have fattened the calf, and are now about to lead the unwary family end-use buyers to the slaughter (and ARMS will help them do that).

The “controllers” are exactly that. Nothing in financial markets happens by chance, except perhaps if a major Black Swan even occurs (but, then to the “knowing,” even most of those are orchestrated by the “controllers”). Otherwise, the controllers manipulate financial and real estate markets solely for their own benefit.

Open your eyes and witness the decline of the middle class, the impoverishment of millions of American families, and the 50 million Americans now on government assistance, and the quickly developing plans to raid pension funds and 401-Ks.

None of that was a coincidence, but was carefully orchestrated by the FED and the banking families that control it and you. Unless our people remove the central bankers from their positions of control, and restore the American Republic, we are lost as a nation, and the collapse of our currency immanent.

Look what you are paying for food and the essentials of life currently. That is nothing compared to what is soon to come.

Is this a dark prognostication? No, not at all. It is a wake up call. Remove the oppressive central bank powers or suffer the consequences. Thomas Jefferson, Andrew Jackson, and a whole host of Great American patriots agree with us. Do you?

LIBOR ,ENRON,PRESIDENT’S WORKING GROUP ,FINANCIAL MARKETS,H.R 5660 ,2000 COMIDITIES,FINANCIAL MARKETS MODERNIZATION ACT,HYBIRD BANKING PRODUCTS,SUB PRIME LOANS , PRADATORY LOANS OTC DERIVATIVES ,CDSWAPS, CD OBLIGATIONS WILL CONTINUE TO CONTROL THE MOST VALUABLE REAL ESTATE IN THE WORLD FOR THE NEXT 30 TO 40 YEARS .

HALF OF THE NOTES DEEDS OF TRUST HAVE A LIBOR INTEREST RATE .DASISATER IS ON .ENRON LEGAL TEAM CALLED THEM SELVES THE SMARTEST GROUP OF PEOPLE IN THE ROOM THE GOAL OF THE GEORGE BUSH ADMINSTRATION ATTACKED CALIFORNIA JAN ,2001 THEY HAVE CRIPPLE CALIFORNIA DAMAGED TH EFUTURE OF EVERY CALIFORNIAN

CALIFORNIA POLTICIIANS WILL NOT PROTECT CALIFORNIA HOME OWNERS MAYBE FIRST TUESDAY WILL BY ASKING THE STATE FOR HELP FOR CALIFORNIA HOME OWNERS IN REMOVING EVERY FINANCIAL INSTRUMENT WHICH HAS A LIBOR INTEREST RATE . . I HOPE IT IS NOT TOO LATE GOOD LUCK WITH THISS ONE

Hi,

I get the impression that you are completely condemning ARMs as a financing tool, in which case I strongly disagree.

There are different types of ARM loans. This essay, as with several other discussions of ARMs I have read in recent years, seems to imply that all ARMs start off with an artificially low interest rate that inevitably has to increase dramatically at some point in the future. To me, this type of loan is just one subcategory of ARMs, with variations such as a structured graduated payment loan or a loan with an extended ‘teaser’ rate which is what you appear to be talking about in this article.

A ‘traditional’ ARM might start off with a slightly reduced teaser rate for the 1st six months or so, and then change to what I call the ‘real rate’ (the index plus the margin) for the remainder of the loan term. The teaser period ‘savings’ can be easily evaluated by applying the short term savings during the teaser period to the total up-front cost of acquiring the loan (points, appraisal, misc. loan fees, etc.) when comparing one loan product to another when determining which type of loan is best suited for a borrower at that time.

A traditional ARM should always be considered during periods of the interest rate cycle when interest rates on fixed rate mortgages are relatively high. The financial decision in choosing a fixed or an ARM in that environment comes down to making an educated guess as to which loan will have the lowest AVERAGE interest rate over the term of the loan. The ARM interest rate will go up at times, but they also go down at times, often by a lot.

Borrowers who chose competitively priced ARMs during high interest cycles since the mid 1980s have averaged much lower interest rates than if they had chosen the fixed rate loan available at that time. At the same time, I believe that when fixed rate loans are available at interest rates that are relatively low by historical comparison, a borrower should always get the fixed rate loan.

Choosing an ARM under the conditions I mentioned always assumes that the borrower is financially and psychologically able to handle the rate increases during the up cycles. I have found, however, that once someone has experienced the joys of having one’s interest rate and monthly payment go down substantially for an extended period, the increase periods are much more acceptable.

As an apartment investor, I have had many ARM loans on investment properties over the past 30 years. A far bigger and more frustrating problem with these loans has been hitting the minimum floor interest rates rather than the periods of higher rates. I have never had an ARM get anywhere near the cap rate.

Thanks,

Tim Carrico