If you have a car, you’ve noticed the savings at the pump over the past few months. Low gas prices are a welcome gift to consumers — though the effect on oil industry workers has been negative, causing a slight shift in the overall unemployment rate. But many consumers are not aware of the influence cheap oil is has on mortgage interest rates.

The Federal Reserve (the Fed) is arguably the number one influencer of mortgage interest rates. Due to a strengthening national economy, the Fed increased the short-term borrowing rate in December 2015. The ripple effect is that interest rates on other loan products will also increase.

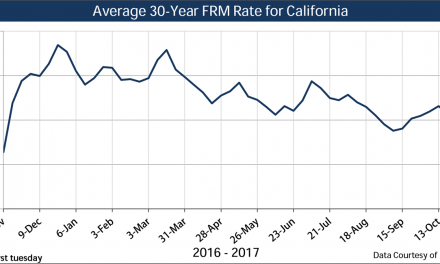

The Fed knows this, and uses the short-term rate as a tool to slow inflation — or in this case, anticipated inflation. However, fixed rate mortgage (FRM) rates have actually decreased since the end of 2015, from 3.9% at the end of December to 3.7% in March 2016.

Why have mortgage rates decreased despite the increase in the short-term rate?

The answer leads back to declining oil prices and ultimately the 10-year Treasury note, which, while influenced by the Fed’s movement of the short-term rate, is guided by investor demand. Investors, discouraged away from the oil market and in search of a safe long-term investment, buy Treasuries. High demand for the 10-year Treasury note drives the rate down, which helps keep FRM rates low. That’s because investors are willing to accept a lower rate of return on the 10-year T-note in exchange for the safety of their investment.

Thus, when the global economy is in turmoil, as is the case in 2016, the 10-year T-note gets cheaper. In turn, FRM rates are held down.

The future of mortgage rates

Expect mortgage interest rates to remain low as long as oil prices suffer. How long will this last?

The U.S. Energy Information Administration (EIA) projects oil prices to increase just slightly in 2016 and 2017. Prices will find support as producers pull back on oil production, but even then prices are not expected to return to mid-2015 levels in the next two years.

To translate to the broader global economy: things probably won’t get worse, but they’re not getting much better anytime soon. Therefore, mortgage rates will likely remain low through most of 2016, until investors become more confident in other investments. first tuesday expects mortgage rates to experience a sustained increase at the end of 2016, at the earliest, though low rates may possibly extend into 2017.

In the meantime, homebuyers and sellers will continue to benefit from the boost in buyer purchasing power due to low mortgage rates. California’s buyer purchasing power index is up compared to mid-2015, with the average homebuyer saving tens of thousands of dollars due to today’s lower rates. Positive buyer purchasing power will also keep home prices on their upward incline, for now.

Once mortgage rates finally increase, expect home sales volume to trend down, followed by prices within a year. Watch the pump closely for indicators on where mortgage rates are headed.

{kind=link}

I am confused. Why does high demand for 10 year treasuries drive their price DOWN? Doesn’t high demand drive prices UP?

Are you intending to say, in paragraph 5 above, that High demand for treasuries drives oil prices down? That also seems odd.

Any clarification would be welcome

Dear Nancy,

Thank you for your question! The relationship between demand and the 10-year Treasury Note is actually the opposite of what you might expect from other economic situations (i.e. when demand for goods is high, the price is often driven up).

However, when demand for the 10-year Treasury Note is high, interest rates are brought down. This is because when a lack of other safe investments exists (as in today’s turbulent global economy), investors are willing to pay a higher price for the 10-year Treasury Note, which lowers the Note’s yield (interest rate). In short, they are willing to accept a lower rate on the 10-year to guarantee the safety of their investment. Therefore, the interest rate moves in the opposite direction of the Note’s price.

For more information, useconomy.about.com/od/economicindicators/p/Treasuries.htm has an article on the subject.

On your second question, which was “High demand for treasuries drives oil prices down?” the answer is actually the opposite. When investors are uncertain about aspects of the economy, like when the supply of oil outstrips demand, causing prices to fall, they turn to safer investments like U.S. Treasuries. Therefore, it’s falling oil prices that cause the increased demand in treasuries (which in turn affects other interest rates like mortgage rates).

Regards,

ft Editorial