Both rental and homeowner vacancies held steady in 2025 as the California population ominously slipped and jobs flattened heralding recession conditions.

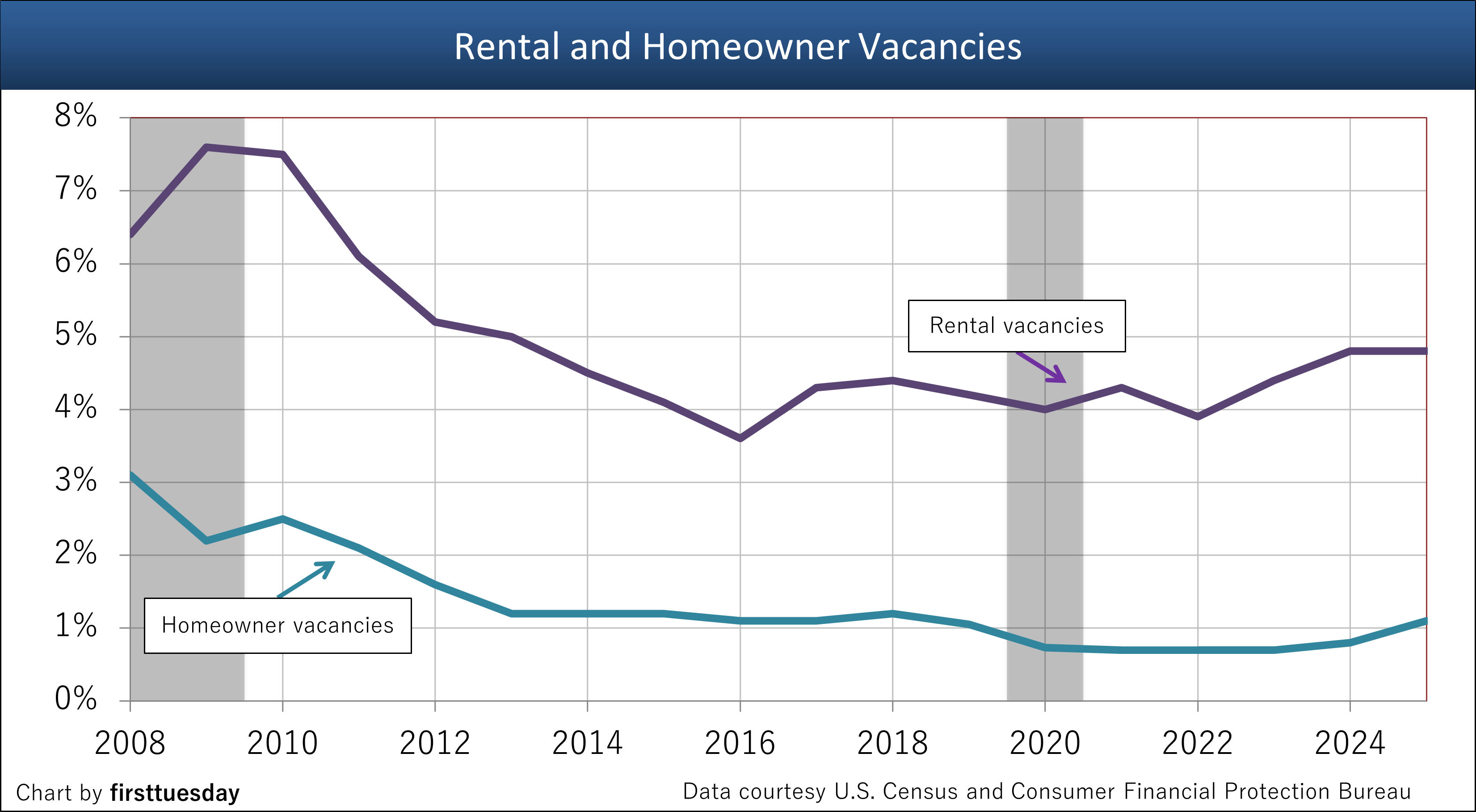

California’s average rental vacancy rate stayed at 4.8% in 2025, less than the historical mean line of 5.5%. It was lowest in 2016 when it was just 3.6%.

In contrast, the homeowner vacancy rate remained tight at 1.1% in 2025, after remaining below 1% throughout the 2020s, it is now at its highest since 2018 at 1.2%.

Vacancies are influenced by a number of factors, particularly California’s job market and construction starts, both of which stalled but did not decrease in 2025. Mortgage rate movement shift vacancy rates between tenant- and owner-occupied residential properties. For example, as FRM rates increase, vacancies in rental units decrease while owner-occupied homes experience an increase in vacancies.

Post updated April 28, 2026.

| 2025 | 2024 | 2023 | |

| Homeowner Vacancy Rate | 1.1% | 0.8% | 0.7% |

| Rental Vacancy Rate | 4.8% | 4.8% | 4.4% |

Trends in residential vacancies

California residential vacancies are broken down into two categories by the U.S. Census Bureau:

- homeowner vacancies; and

- rental property vacancies.

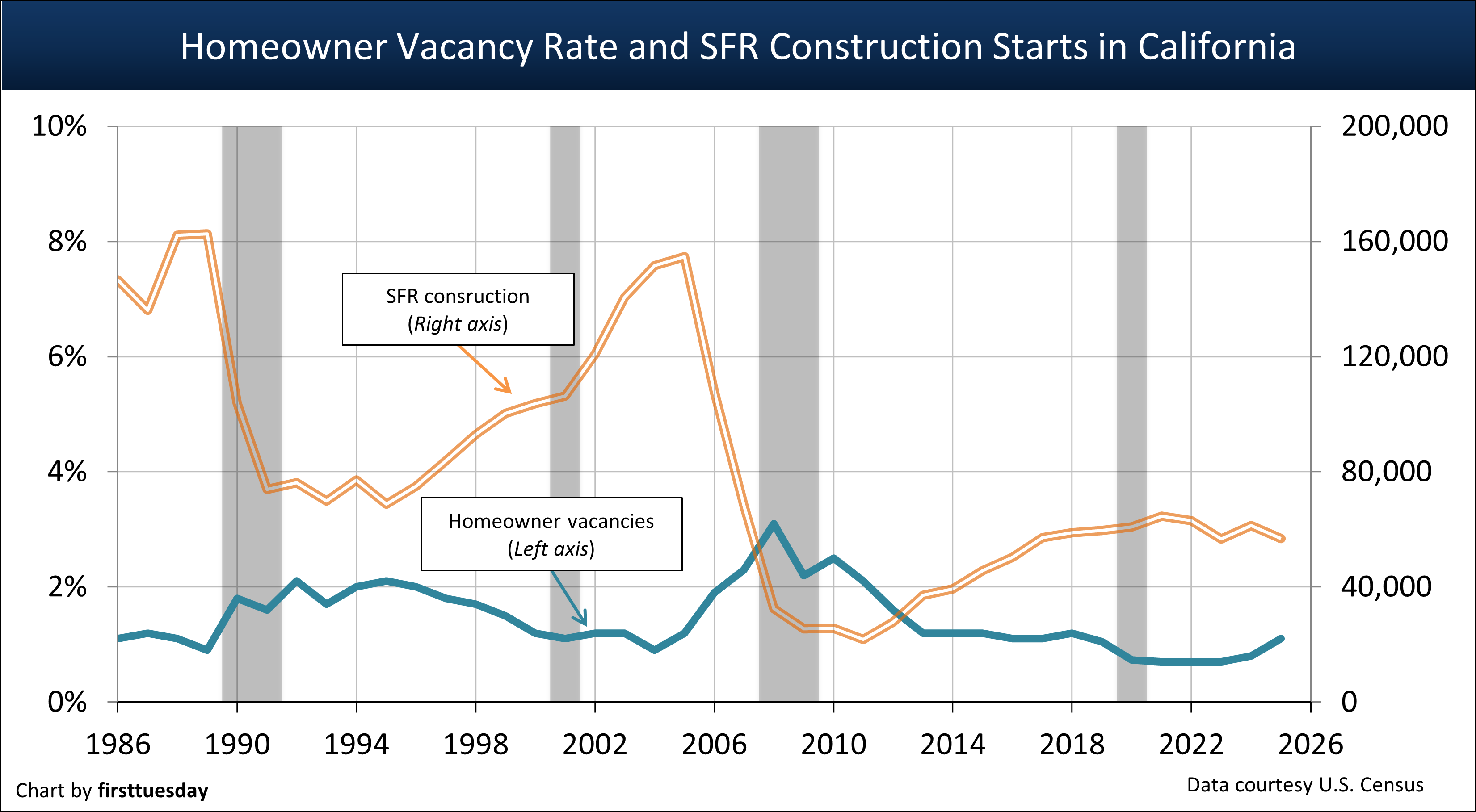

Homeowner vacancies represent the number of vacant units present in California residential housing stock occupied by the owner. In 2024, California had just under 7,567,600 owner-occupied housing units. Owner-occupied housing units consist of residential properties which are:

- owner-occupied;

- sold to a homebuyer and awaiting occupancy from inventories available for sale by both builders and resale owners; or

- unsold and vacant housing inventory not available for lease.

The annual vacancy rate in California for owner-occupied housing consistently returns to roughly 1.2%. As the economy strengthens and weakens in business cycles as population growth, jobs and housing starts fluctuate, actual vacancies run below the equilibrium (as in 2005) and above it (as in 2010). Presently, homeownership vacancies — comprising primarily homes for sale — are returning to the mean vacancy rate.

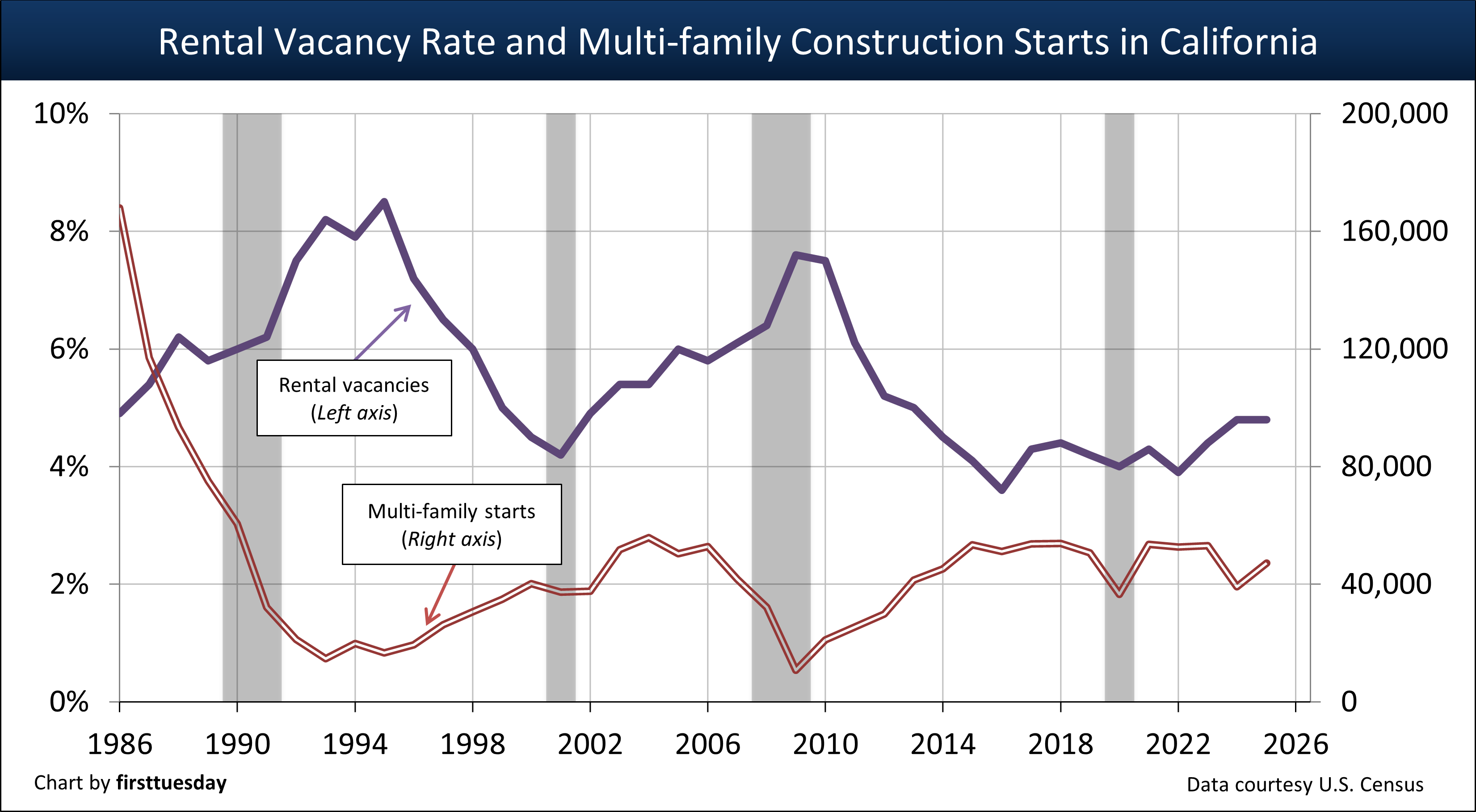

Likewise, rental property vacancies represent the number of vacant units in California’s rental housing stock. Rental housing consists of residential units which are:

- renter-occupied;

- rented and awaiting occupancy; or

- unrented and vacant and held out for sale-or-lease, or only for lease.

The vacancy rate California residential rental properties return to is roughly 5.5%, a pivotal figure for an analysis by property managers and investors (in 2020, it averaged 4.1% and grew to 4.8% by 2025). Homeowners are less likely or simply unable to sell, pack up and move in recessions as they are tethered to their homes by negative net equity and an unwillingness of buyer-occupants to make offers.

Like owner-occupant residential vacancies, the rental vacancy rate varies above and below this pivotal mean figure as economic conditions vary throughout a business cycle from a recession trough to a recovery peak and crash.

Presently, the rental vacancy rate is slightly below normal. During the past decade, the low rental vacancy rate has been partly attributed to the slowly recovering construction industry due to the inability to obtain permits needed to keep up with rising rental demand. Restrictive local zoning ordinances in coastal urban areas were able to limit new multi-family housing.

The competition between vacant owner-occupant residential units and vacant residential rental units is a zero-sum game. First, when prices for homeownership are high it makes financial sense to rent. Thus, as vacancies in rental housing decline, vacancies in owner-occupant housing units go up. The population simply exercises its housing discretion to move about when financially expedient.

Other factors influence this equation, like the massive foreclosure and short sale crisis that ruled the housing market for five years following the December 2007 commencement of the Great Recession. One factor, mortgage rates, bottomed in January 2013 followed by sufficient willing buyers coming in to drive home prices up 33% in 2013. Over time, the dominance of one type of housing (homeowner vs. rental) is equalized by a shift in favor of the other type of housing.

For instance, as more and more individuals continue to favor rental housing, the demand for rental housing causes landlords to increase rents to maximize profits as they can to meet demand. This, in time, translates into better financial results by owning and occupying a home, as well as profit opportunities for construction of new homes as home prices rise.

Additionally, as economic conditions weaken, households consolidate to save money by sharing monthly housing costs with roommates, be they family or others. Consolidation leaves residential units vacant without the vacating occupant transitioning to homeownership or another rental unit but moving in with others. Thus, fewer residential units of all types are occupied.

Easy lending fuels a building rampage

Chart update 4/28/26

| 2025 | 2024 | 2023 | |

| Homeowner Vacancy Rate | 1.1% | 0.8% | 0.7% |

| SFR Construction Starts | 56,800 | 61,200 | 56,700 |

Chart update 4/28/26

Chart update 4/28/26

| 2025 | 2024 | 2023 | |

| Rental Vacancy Rate | 4.81% | 4.82% | 4.44% |

| Multi-family Construction Starts | 47,200 | 39,200 | 53,100 |

The introduction of new housing units into the homeowner/rental vacancy equilibrium is not in and of itself a disruptive event. This is simply because the California population consistently grew around 1% annually since 2001, though the trend stopped with the Covid pandemic.

Related article:

Today, NODs and foreclosures are rising again. Q1 2026 began with a foreclosure sale in 0.08% of properties in California. This represents a 15% increase from the same time last year.

While foreclosure rates bottomed in 2020 due to pandemic-era housing protections, 2026 isn’t close to the intimidating rates of 2009-2011. Current experience is around one-eighth of the foreclosure sales compared to the height of the foreclosure crisis.

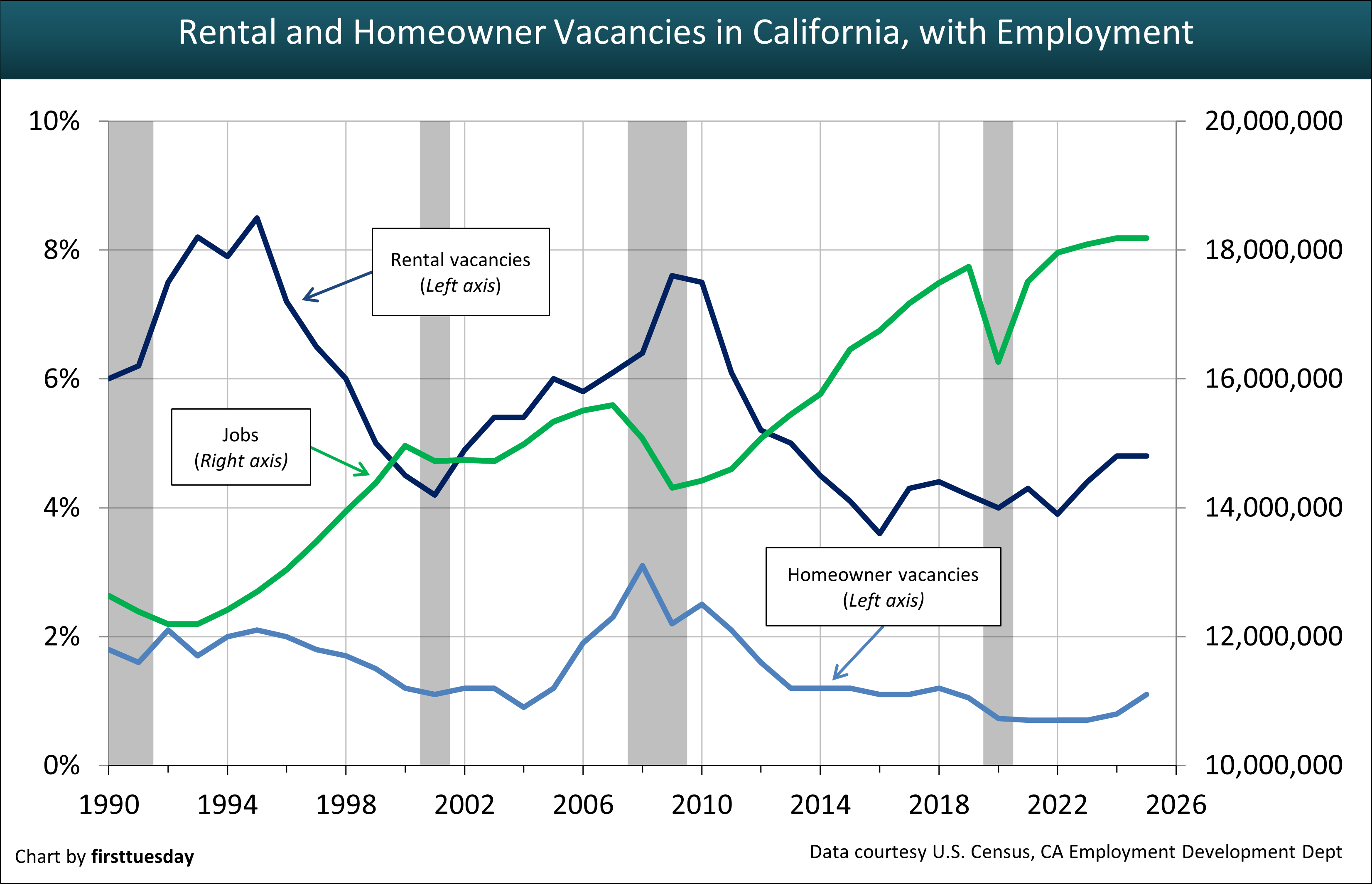

Jobs move real estate

Chart update 4/28/26

Jobs surpassed 2007 pre-recession levels by late-2014. However, California didn’t regain enough jobs to keep up with the population increase of 1.7 million individuals that occurred during the in-between years through 2019. Unfortunately, the population catch up took place just in time for the 2020 recession to hit, causing a loss of 2.7 million jobs.

California reached its pre-pandemic 2019 peak of 17.6 million total non-farm jobs in October 2022. The job growth continues, though at half the pace, ending 2025 at nearly 18.2 million jobs six years on from 2019. After two decades of national economic growth, cheaper homes and about the same pay for jobs in other states distract those considering a move to California.

Without confidence in the California job market, changes to households slow. Younger generations dealing with more debt obligations are either priced out of homeownership or wait to leave home rather than rent.

They are shadow households — the users of real estate in need of financial stability through jobs and an acceptable price of ownership and tenancy before they set up a household. When they start setting up households, vacancies in all types of residential vacancies will decline. Construction will follow.

When they do succeed in finding jobs that will support households in California, most of them will initially rent until they become comfortable with their jobs and community.

Agents and brokers look forward

Today, we see the abrupt rise in vacant units in the residential ownership and rental markets as housing occupants react to the past ten years of annual price and rent increases far exceeding wage increases. The two sets of vacancy rates will further rise until property prices and rent respond to what is shaping up as significant long-term changes to the California economic landscape.

Brokers and agents with an eye on vacancy rates notice that different niches of the housing market have different needs for their services. City centers comprise culture, commerce, finance and government, and an environment which more quickly works through their inventory for sale or for lease than their suburban bedroom community counterparts.

Suburban areas primarily provide homeowner occupancy which has a very low rate of turnover compared to urban areas with predominantly tenant occupied residential units. Expect rental inventory for lease in urban markets to dry up first. The trend brings on construction jobs and investment in rental unit construction and brokered transactions as the pace of turnover picks up.

{kind=link}

Amazing, and love to read. Thanks for sharing!

What are the factors & aims, objectives on residential property. Its my project topic. Thank you.

Very nice post, I am also associated with real estate, foreclosure Los Angeles County, California taxes and properties. I enjoy reading new stuff on this subject, and I hope you will be adding new and fantastic posts on property services. Thanks for writing such a wonderful post.

Orange County actually has more people in their 40’s than their 20’s, so gen y is smaller there since a lot of babyboomers left the OC in the early 1990’s- and whites left big in the early 1990’s. Now, Mission Viejo has a lot of teengers, so past 2020 the y will help.

I simply don’t think that Gen. Y, the echo boomers, will come around and save the day. We, that majored from Uni., mostly majored in soft majors that are not applicable in the American job market of today or tomorrow. The uni.’s should have capped, and should cap, the number of people graduating with “communication studies” and “art history” majors and so on. That won’t happen. So people graduating from uni. today are already finding themselves irrelevant in the job market. Most 19 year olds are unaware of this though. The educated members of Gen. Y will be like the young, but not so young, Japanese of 10 years ago and today, unwilling or unable to leave home, get married, or make babies. Come around to the time when Gen. Y finally decides to grow up and they will be inheriting homes from their dead parents i.e. not buying homes. What does all this mean with the glut in the housing market?-There won’t be a recovery in housing markets unless we let a ton more immigrants in to do the buying for us. Turnaround in 2013? Laughable. What prospects are there on the horizon? Even if there are some cutting edge new industries of the future that America can take part in, kids are still getting their degrees in unrelated fields.

Don’t forget about all the school loans Gen Y has which they will also need to pay off before buying a house. Household formation will be delayed even further.

Great article with loads of useful information – all something we surely felt as we are still trying to get back on our feet here in the “Golden” state.

How it all comes together: property ownership, rentals, vacancies, and construction. This is the big picture. Thanks for a great article and illustrative graph.