This article explores the relationship between the disappearing middle class and mid-tier home sales.

Home prices rise

Let us tell you a story about home prices.

This story starts in the year 2000. Y2K is recently behind us and the dot-com bubble will soon burst. The majority of Americans are middle class. Most Baby Boomers are homeowners, and many are looking to trade up. The suburbs are “in” and Britney Spears has just released “Oops, I did it again.” (You get the picture.)

Meanwhile, home prices are riding up the rails into the Millennium Boom, the biggest roller coaster home price rise in history:

The chart above reflects 2016, which has mid-tier home prices between $501,800 and $764,700. But in 2000, mid-tier homes were hundreds of thousands of dollars lower.

Editor’s note — Price tiers are determined by the original sale price of a property. For instance, a property which sold for $300,000 was considered mid-tier in the year 2000. This same property sells for $600,000 today, and it is still considered mid-tier. Weighting is used for individual homes that may have undergone renovations which may account for part of the change in price.

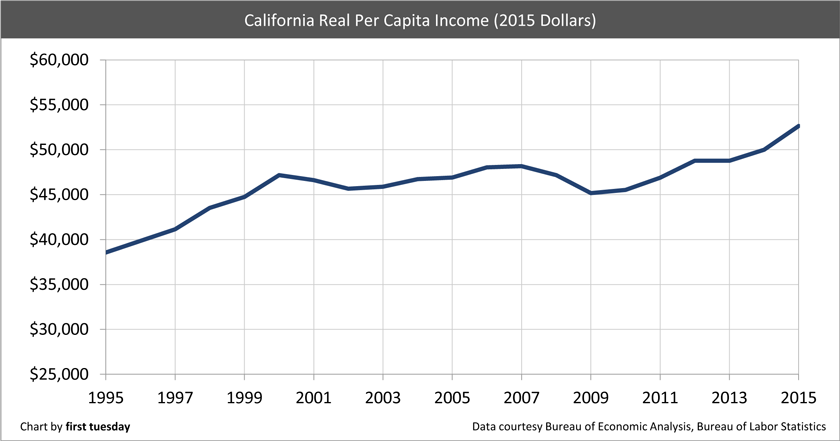

Here’s the rub: while mid-tier home prices have increased dramatically since 2000, incomes have increased much less:

So how have prices been able to increase so quickly? Either:

- middle income households are pouring more resources into buying; or

- middle income households are now only able to buy in the low-tier, if at all.

Editor’s note — Middle class is defined as having a household income 66% to 200% the median income, adjusted for household size and changes in the cost of living.

The amazing disappearing middle class

61% of households were middle class in 1971. In 2000, 55% of households were middle class. In 2014, 51% of households were middle class. The data paints an even more quickly degenerating middle class in California.

A Californian family of four needs a pre-tax income between $54,000 and $161,000 to be considered middle class, according to the Pew Research Center. In contrast, nationally, a middle class family of four needs only $48,000 to $144,000. This difference is due to California’s higher than average cost of living.

In 2014 (the latest data available), income classes are split nationwide, with:

- 19% considered upper class;

- 51% considered middle class; and

- 29% considered lower class.

In California, the middle class is smaller than average, with:

- 20% considered upper class:

- 48% considered middle class; and

33% considered lower class.

Source: Pew Research Center

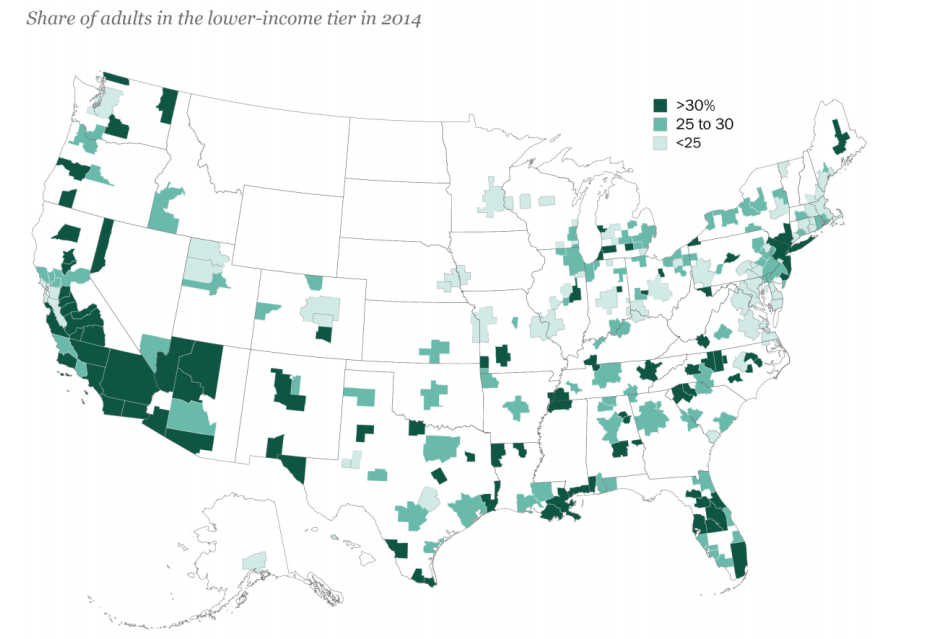

California has more households living on the extremes, according to the Pew Research Center. In fact, metropolitan areas with some of the biggest shares of upper class in the nation — but also the biggest shares of lower class — are found in California, with:

- 31% of San Jose-Sunnyville-Santa Clara residents in the upper class (compared to the 19% national average); and

- 28% of San Francisco-Oakland-Hayward residents in the upper class (compared to the 19% national average); alongside

- 46% of Visalia-Porterville residents in the lower class (compared to the 29% national average); and

- 43% of Fresno and Merced residents in the lower class (compared to the 29% national average).

The widening gulf between members of the Golden State’s upper and lower classes illustrates worsening income inequality.

Further, the median income within these income groups has fallen 6% since 2000 in California. Broken up by income group:

- lower class incomes are 10% lower today;

- middle class incomes are 6% lower today; and

- upper class incomes are 8% lower today.

The problem for housing

As more households find themselves unable to keep up with a higher cost of living, many are unsure where to turn for housing.

In fact, the National Low Income Housing Coalition estimates California has a low-income housing shortage of over one million units.

The situation for renters is extreme. California has the second-highest housing wage in the nation, after Hawaii. In order to qualify at 30% of their income for a two-bedroom rental, a full-time worker needs to earn $28.59 an hour in California, according to the National Low Income Housing Coalition. However, the average renter’s wage, at $19.22 per hour, is much less than what is needed.

Even a one-bedroom apartment is out of reach for many, as the average minimum wage worker needs to work 89 hours a week to qualify for a one-bedroom in California. Therefore, living with roommates and parents is becoming more necessary and more commonplace.

For those seeking to become homebuyers, the situation is also dire.

Potential first-time homebuyers literally have the hardest time finding starter homes to purchase in California compared to other states. That’s because there are so few homes on the market for sale within reach of first-time homebuyer incomes. This problem is compounded by high levels of student debt, which weigh down incomes already stretched thin.

The solution for many unable to keep up with rapidly increasing costs of living is simply to delay major life events, including:

- getting married;

- starting a family;

- leaving the nest; and

- buying their first house.

Still, low-tier home sales don’t appear to be suffering in 2016. In fact, low-tier homes are increasing in price more quickly than any other tier.

But this isn’t because there are plenty of low and middle class homebuyers eager to buy — it’s really due to the fact that middle class buyers are being pushed out of the mid-tier home sale market. In other words, they aren’t able to qualify for the same houses they were able to in years past. So they are now competing for low-tier homes, which pushes up the price of these homes more quickly than high-tier home sales, and especially higher than mid-tier sales.

The middle class is quietly declining. Unless the middle class makes a comeback, this will only worsen. Homebuyers will over-reach and resort to dangerous adjustable rate mortgages (ARMs) to extend their purchasing power. Prices will rise more and more quickly and speculators will intervene in increasing numbers. If this sounds familiar, you were around during the Millennium Boom (and bust).

{kind=link}